Powell’s Jackson Hole Symposium Preview: Inflation’s virtual reality

- Chairman Powell’s speech expected to recast the effort to raise inflation.

- Remarks to outline the result of the Fed’s “Monetary Policy Framework Review”.

- Inflation averaging would permit periods of faster price gains.

- Unclear how the new terminology would differ in practice differ from ‘symmetric inflation’.

- Central bank’s monetary tools have been increasingly ineffective in spurring inflation.

- Unless the Fed introduces new policy tools, markets likely to be unimpressed.

The Federal Reserve is the world’s most successful central bank. It has shepherded the US economy through the worst financial crisis since the Depression and the first pandemic in a century. But until a decade ago its most lasting achievement was the reduction of inflation to a footnote in the US economy.

Jerome Powell the Federal Reserve Chairman and the governors are worried that the bank has done its work too well. Since the financial crisis the Fed has been unable to push inflation back to its 2% target.

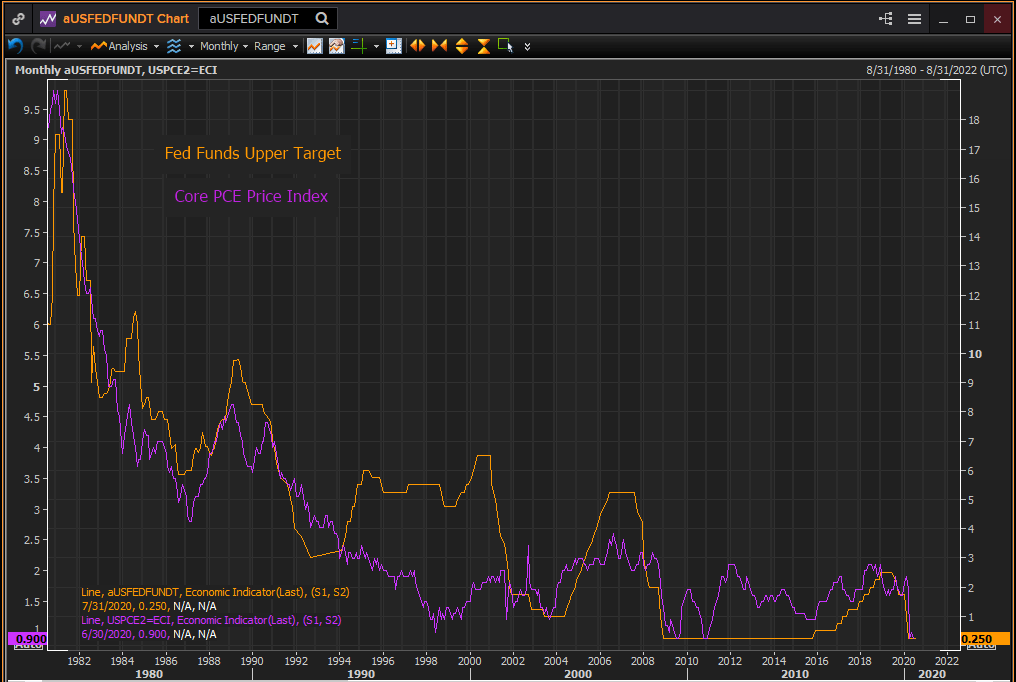

The quadrupling of the Fed balance sheet from 2008 to 2014 resulted in just one year, 2018, with an average core PCE rate of 1.96%, that was close to the bank's 2% target.

Since that was almost five years after the Fed stopped expanding its balance sheet, it is most probable that it was the excellent economy of 2017 and 2018 and the cumulative gains in the labor market that had enabled higher prices rather than any QE addition to the money supply. The price pressure did not last and by the middle of 2019 core PCE prices were back to 1.5%.

Core PCE price index

Why a 2% target?

For consumers inflation means an added burden on family budgets and low or even falling prices would seem a benefit.

In the macroeconomic world of most economists weak inflation accompanies a slow growing economy with stagnant standards of living. Low inflation also means equally spare interest rates which give central banks little room to cut when they need to spur growth. A permanent low inflation environment is far less susceptible to the bankers’ main economic tool, interest rate adjustment.

There is a further reason for central banks to promote inflation—government debt. A 2% inflation rate devalues debt 20% a decade. With US national debt over $26 trillion and total domestic non-financial debt at $56 trillion debt, inflation helps keep the service payments from crowding out investment.

Monetary Policy Framework

The Fed’s year-long review involving bank officials and the public is expected to produce an outline of future policy. As inflation has been the bank’s most consistent failure, that is where the focus is expected.

One possibility is that the bank will target “average inflation.” Simply put, that means inflation would be permitted to run above target for a certain amount of time to bring the overall rate up to its goal.

It is not clear how this would differ from the current charge of “symmetric inflation,” which anticipates prices to be balanced above and below the target, which after all, is what symmetric means.

Inflation targets, practice and globalization

The Fed’s inability to raise inflation has not been because it is undecided about its goal, or that it doesn’t understand that if inflation has run at 1.5% for six months, a 2.5% rate is needed in the next six to produce an overall rate of 2%.

Inflation has have been declining for a generation. It is no coincidence that the last thirty years have seen the advent of the global consumer economy. Goods are produced, marketed and sold around the world. The ability of manufacturers and retailers to raise prices in a national market, especially in the US that is relatively open to imports, is severely limited by global production and competition.

As has become increasingly evident in the last decade, global price pressure is a powerful countervailing force to money supply expansion.

When the Fed began its QE experiment in 2008, there was much speculation as to when prices would begin to rise from the vast addition to the money supply. That they would increase was accepted knowledge. The answer turned out to be never.

Against the diminished consumer demand from jobs losses after the financial crash and the array of imported products, the QE flood had almost no impact.

Conclusion

The Fed’s inflation problem is, to use the currently popular world “systemic.”

Central banks were conceived in a world of national economies. Manufacturing, consumption and finance are now global enterprises. No economy is isolated and traditional interest rate policies are far less effective than they were when the majority of consumer demand was satisfied domestically.

The reasons the Fed has been unable to achieve its inflation target are found in Hunan factories and Brazilian soy fields not Walmarts in Des Moines and Albuquerque.

Unless the Fed has created innovative tools to accompany its revamped terminology, the new inflation policy will be just a virtual image of the old.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.