Oil turns bullish after OPEC output hike deal confuses markets

The Organization of the Petroleum Exporting Countries (OPEC) and a group of 11 non-OPEC countries struck a deal on Friday to raise oil production from July, marking the first increase since the alliance began capping output in January 2017. Crude oil prices surged immediately after the announcement as an agreement was not certain due to strong objections from Iran. However, the lack of clarity on how the production increases will be achieved and how much of a supply boost can be realized from the deal has generated more uncertainty about the outlook for the oil market than remove them.

With the announcement being short on detail, it was left up to market participants to interpret the deal based on differing estimates provided by the various countries’ energy ministers. Saudi Arabia says the agreement paves the way for a nominal increase in output of 1 million barrels per day (bpd). Iran puts the figure at half that level at 500,000 bpd. But the actual increase is likely to be something closer to 600,000 bpd as many countries in the pact have limited capacity to raise output. While the big producers Saudi Arabia and Russia have plenty of spare capacity to meet higher targets, the increase would need to be shared among all participating nations, meaning a modest hike of around 600,000 bpd in real terms is the likely outcome.

Some analysts have described the deal as a “fudge”, as the compromise reached between Saudi Arabia and Iran involves no new increases in production but simply requests that bloc members return to 100% compliance of the original output targets after months of underproducing. Overcompliance, particularly among OPEC countries, had started to become a problem since late 2017, fuelling the recovery in oil prices. Compliance by OPEC has been running above 150% since February, meaning producers have been cutting output by more than required. In contrast, compliance among non-OPEC countries has been on the decline since January.

Russia, a non-OPEC country, is likely to be the most disappointed from the deal as it had been pushing for a rise in supply of up to 1.5 million bpd. However, the vagueness of the agreement allows the OPEC-led pact to claim success, keeping Iran satisfied in that the real increase is far less than what had been anticipated, whilst Saudi Arabia can boast of a 1 million bpd boost to supply, pleasing its close ally, the United States. The US President, Donald Trump, had publicly been pushing for higher output to reduce oil prices ahead of the mid-term elections in November.

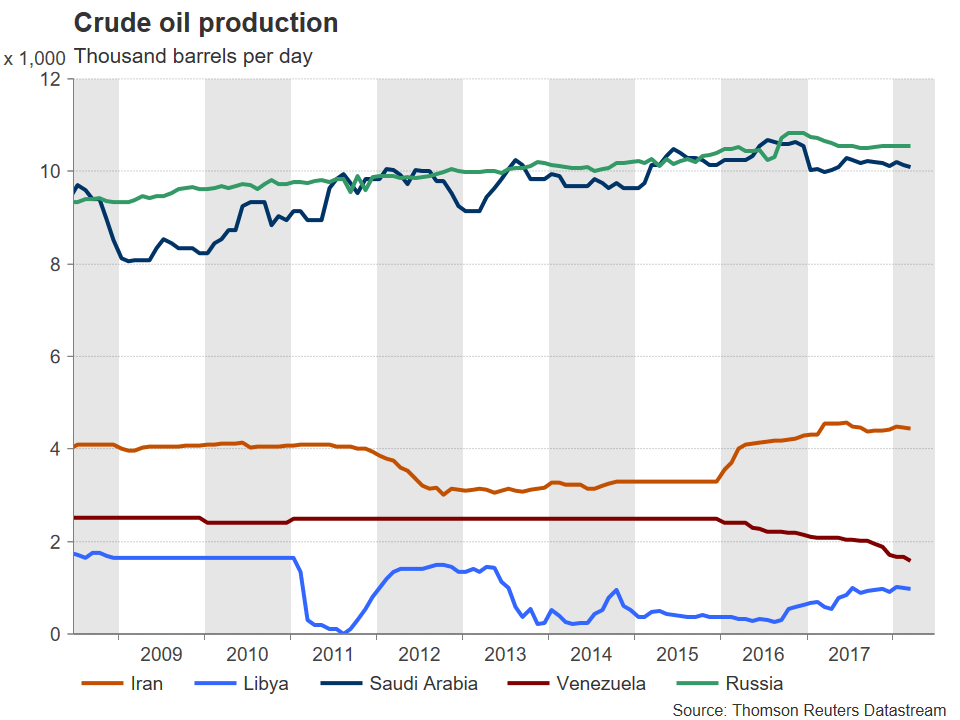

However, the President may not get his wish of cheaper gasoline prices for American voters as oil prices rallied after Friday’s deal as investors are unsure how successful OPEC and non-OPEC will be in raising output. The main problem lies with difficulties among some OPEC members in lifting production, namely, Venezuela, Libya and Iran. Venezuela is facing tough international sanctions which have crippled its economy. Years of underinvestment and mismanagement have led to a collapse in the country’s oil industry. Production stood at just 1.5 million bpd in April, about a third below its OPEC-set target.

Libya’s production meanwhile has been unstable due to fighting between government forces and various rebel factions that has afflicted the country’s oil facilities. And although Libya is exempt from OPEC’s cuts, the widespread violence and lawlessness is causing severe supply disruptions and hampering the country’s efforts to raise production to 2 million bpd by 2022.

Iran on the other hand has been hit by fresh sanctions from the United States and its exports are braced for a major tumble in the coming months. The Trump administration this week increased pressure on other countries to stop importing oil from Iran. The US State Department has given buyers of Iranian oil exports until November to completely halt their purchases.

Oil prices jumped higher after the news as it further raises the prospect that disruptions to supply will greatly outstrip any increases in output following the deal. Another potential future boost to prices is world demand rising more strongly than expected in 2018, assuming of course that growing trade tensions don’t upset the global growth story.

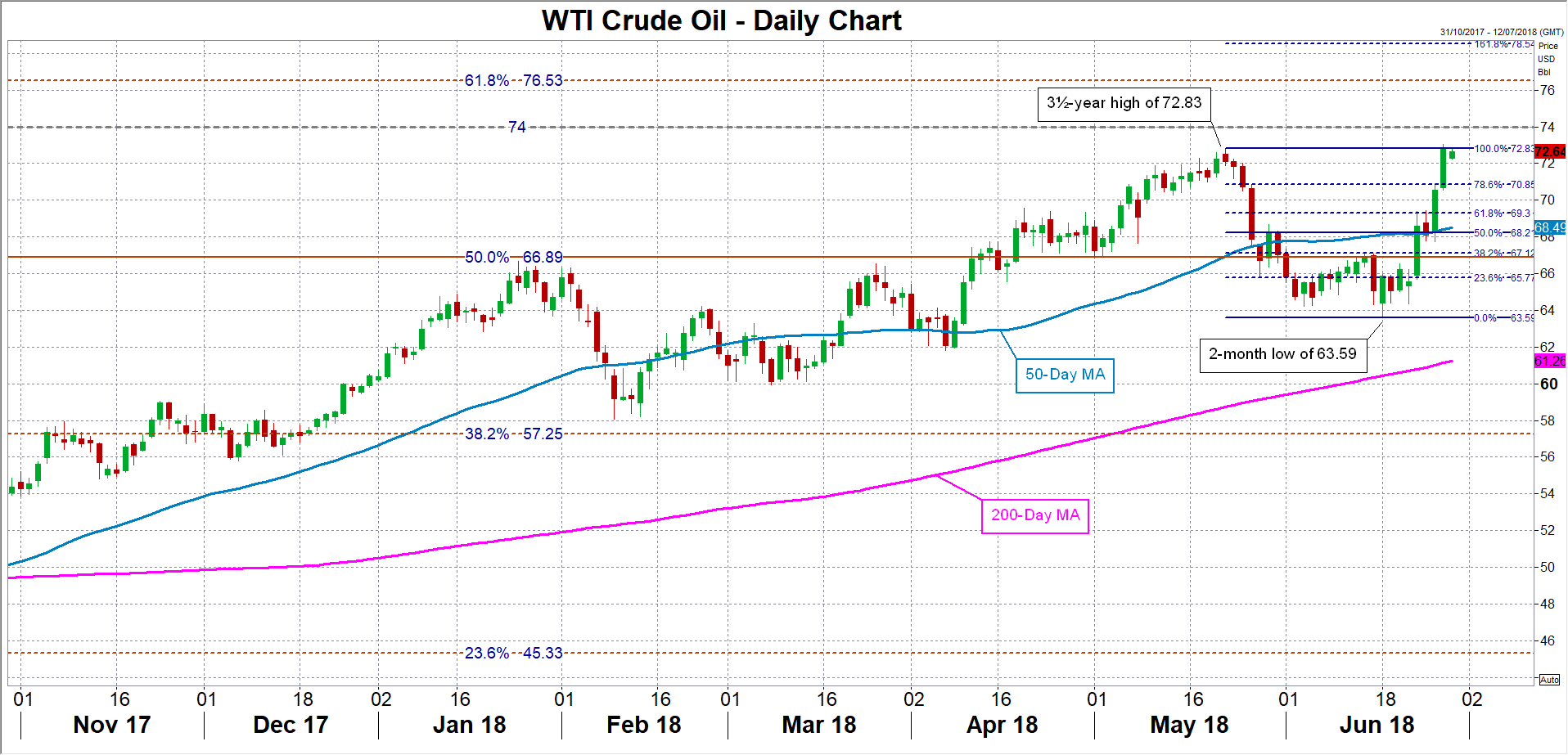

If oil prices continue to evolve in a bullish structure, it won’t be long till WTI reaches the $74 level. WTI prices have already broken above the 3½-year high of $72.83 a barrel achieved in May, reinforcing the medium-term positive outlook. Steeper gains would likely meet resistance around $76.50 (the 61.8% Fibonacci retracement of the June 2014 – February 2016 downtrend) and then near $78.55 (the 161.8% Fibonacci extension of the May-June downleg).

Downside risks remain though, and many traders will probably want to wait until OPEC publishes production levels for July to get an indication as to how much member countries have boosted supply following the June deal. Another risk is a worsening of the trade row between the US and its major trading partners. A deepening trade conflict could derail the global economic recovery and this in turn would dampen demand for oil.

Should oil come under renewed selling pressure, WTI will likely seek support from the 61.8% Fibonacci of the May-June slide around $69.30, followed by the 50% Fibonacci around $68.20. A drop below the 50% Fibonacci could accelerate the declines, drawing attention to June’s 2-month low of $63.59.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.