Nonfarm Payrolls January Preview: Waiting for the dollar bid

- Payrolls expected to return to positive at 50,000 after -140,000.

- Initial Jobless Claims continued December's rise into January.

- Purchasing Managers' Indexes in services and manufacturing maintain expansion outlook.

- Business spending has remained steady despite pandemic increases.

- Dollar, improved in January, will swing with payroll performance.

The US labor market recovery was interrupted in December by the return of the pandemic and the reaction of a few states, particularly California with the largest economy, sent payrolls into a tailspin.

The shutdown of the Golden State and revived restrictions in a few others drove initial jobless filings up almost 100,000 a week from November to December, an increase that has continued into January.

Nonfarm payrolls dropped from 336,000 in November to -140,000 in December, the first job losses since the March and April calamity.

Has the notable decline in case loads and hospitalizations in January and the ending of California's shutdown been enough to encourage employers to begin hiring again?

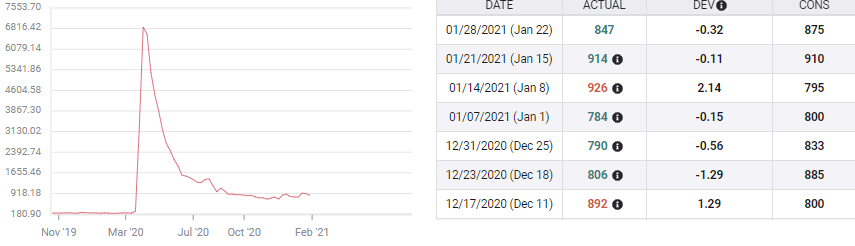

Initial Jobless claims

Claims have been the telltale for the pandemic economy. They heralded the collapse in payrolls in March and April and again in December.

From November to December the monthly average of unemployment filings jumped from 740,500 to 837,500. Nonfarm Payrolls, as above, contracted for the first time since April.

Initial Jobless Claims

Initial filings have continued to rise in January. The average of the first four weeks is 867,750. If the 830,000 forecast for the final statistic is correct the average drops to 860,200.

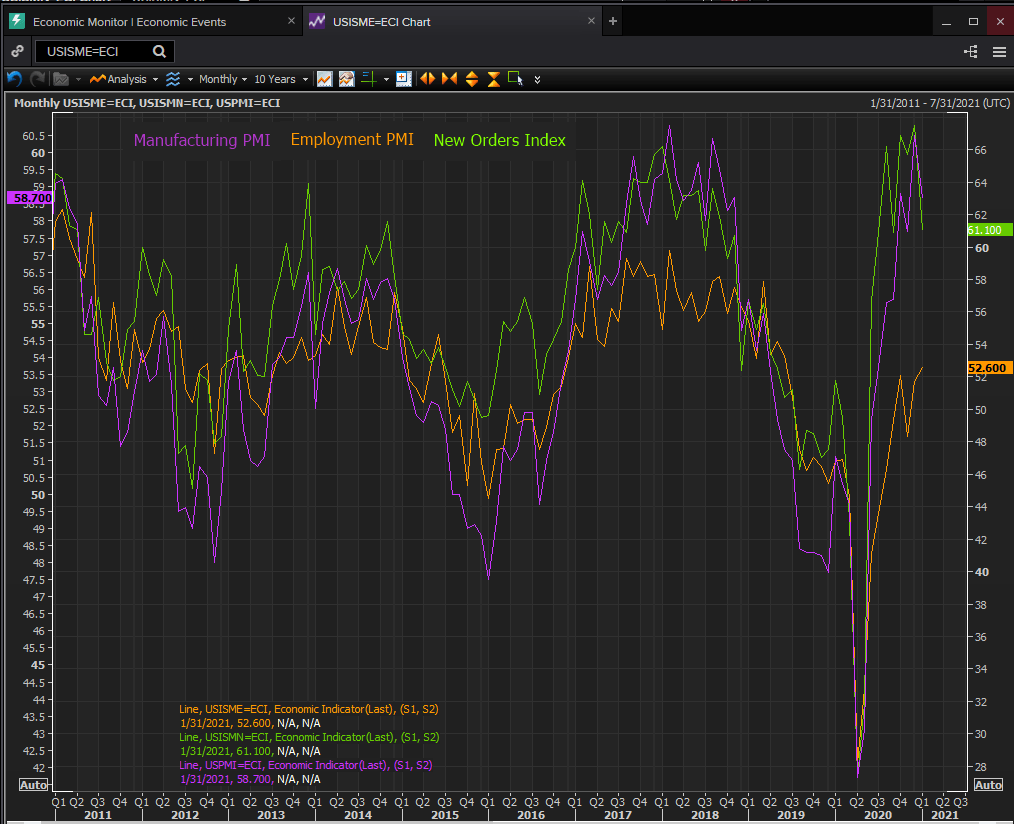

Purchasing Managers Indexes

Manufacturing PMI from the Institute for Supply Management (ISM) has been substantially better than forecasts since June, beating estimates in five of those eight months and averaging a healthy 56.6.

For January the overall index at 58.7 missed its 60 estimate but the three-month moving average of 58.96 is the best since October 2018.

The Employment Index rose to 52.6 in January, the highest score since June 2019. It has been positive for three of the last four months after 14 below the 50 division between expansion and contraction.

The New Orders Index slipped to 61.1 in January from 67.5, but December's three-month moving average of 66.7 was, but for December 2003 and January and February 2004, the highest in twenty-five years. The Manufacturing Employment Index increased in January to 52.6, its best level since June 2019, from 51.7.

Reuters

Optimism also pervades the far larger services sector. The Services Employment Index came in at 55.2 for January, its highest level since February 2020 and a unexpected jump from its 49.7 forecast and December's revised 48.7 (initially 48.2).

The overall Services Index climbed to 58.7 in January its highest score since November 2018. New Orders rose to 61.8 from 58.6, also its eighth month of robust expansion.

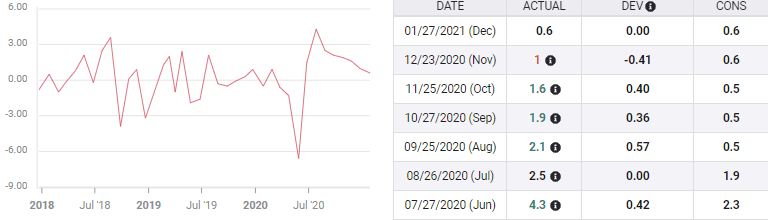

Business investment

Executives have been anticipating a full-blown recovery for six months. Attitudes have remained positive through the fall and winter surge of COVID-19, now in sharp retreat. Business have spent in accordance with their view of a pending economic expansion.

Nondefense Capital Goods ex-aircraft, the business investment proxy category of Durable Goods, averaged a 1.62% monthly increase from July through December. Spending in October, November and December was lower at 1.07%, even as viral counts were spiraling across the country.

Nondefense Capital Goods

Conclusion

Initial Jobless Claims, being weekly, are the most up-to-date US labor statistic but for once they may be behind the curve in the fast-moving events of the pandemic. Since early January US positive tests are down 35%, hospitalizations 28% and ICU occupied beds 20%.

Except for the rise in case numbers and California's attendant closure at year end, the labor market would have continued to improve in December. Initial claims are the consequence of that action not a precursor of greater layoffs.

In that environment it is possible that businesses may have resumed their planning for recovery, extending it this time to their employees.

The dollar has had a modestly successful New Year, gaining 1.6% against the euro 1.8% versus the yen and 0.6% from the Canadian dollar. Gradually rising Treasury interest rates and the prospective US recovery have been the twin propellers. If the potential recovery moves closer to reality with strong January payroll the dollar will receive another bid.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.