If You Build It, Will They Come?

In the movie “Field of Dreams,” a mysterious voice urges Kevin Costner to unearth part of his cornfield and replace it with a baseball diamond. “If you build it, he will come,” the voice says. It takes Costner immense perseverance to fulfill his mission, but in the end, the field is completed and serves its purpose.

Today, it seems as if there is a mysterious voice speaking to politicians all over the world, urging them to build. Infrastructure has become the siren’s song that governments are tempted to follow as they search for strategies to boost economic growth. But the mission of designing an effective infrastructure program has proven frustrating for many who have attempted it. What seems like a panacea can be problematic.

Broadly stated, infrastructure includes anything that creates economic capacity, including physical and intellectual capital. This essay will focus on the former; we’ll discuss investments in education at a later date.

Physical infrastructure encompasses systems and facilities that are essential to economic functioning. Projects follow a hierarchy of needs: at the bottom are public works that support basic subsistence (water treatment, electricity) and at the top are endeavors that expand horizons (broadband). The McKinsey Institute estimates that global spending on physical infrastructure amounts to $2.5 trillion each year.

Investing in infrastructure generates several types of benefits:

Today, it seems as if there is a mysterious voice speaking to politicians all over the world, urging them to build. Infrastructure has become the siren’s song that governments are tempted to follow as they search for strategies to boost economic growth. But the mission of designing an effective infrastructure program has proven frustrating for many who have attempted it. What seems like a panacea can be problematic.

Broadly stated, infrastructure includes anything that creates economic capacity, including physical and intellectual capital. This essay will focus on the former; we’ll discuss investments in education at a later date.

Physical infrastructure encompasses systems and facilities that are essential to economic functioning. Projects follow a hierarchy of needs: at the bottom are public works that support basic subsistence (water treatment, electricity) and at the top are endeavors that expand horizons (broadband). The McKinsey Institute estimates that global spending on physical infrastructure amounts to $2.5 trillion each year.

Investing in infrastructure generates several types of benefits:

- Maintenance of existing infrastructure reduces the risk of unfortunate occurrences. Aging architecture near geological faults, decaying power grids and poorly maintained levees in flood plains can introduce terrible human costs when they fail.

- Spending on infrastructure accrues directly to economic growth. Sales of essential materials increases, and those involved in construction and maintenance see their incomes enhanced. When these earnings are spent, economic activity is boosted.

- Progressive infrastructure can boost productivity. When people, products and ideas move more fluidly, the potential for creating output is higher. At a time when advances in productivity growth have been tepid, infrastructure is seen as an avenue to better outcomes.

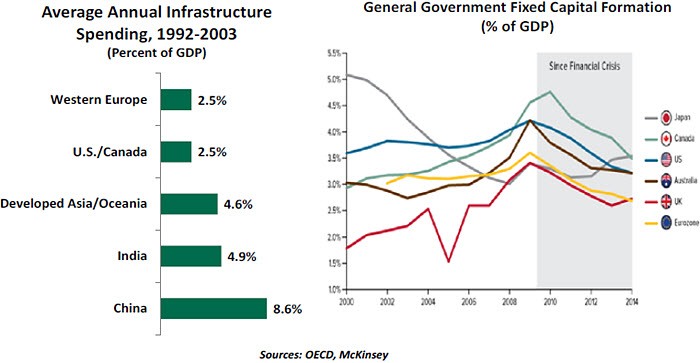

Despite these apparent benefits, infrastructure investment has flagged in the developed world since the 2008 financial crisis. The modest interest rates of the past eight years should have made projects more attractive, but a series of hindrances have limited progress.

The vast majority of infrastructure spending around the world is performed by governments. This makes a certain amount of sense: infrastructure is a public good that matches best with public financing. Central coordination of investment can overcome suboptimal regional incentives. Infrastructure often involves networks (transportation, electric, communications) whose local weaknesses can hamper the broader system.

The vast majority of infrastructure spending around the world is performed by governments. This makes a certain amount of sense: infrastructure is a public good that matches best with public financing. Central coordination of investment can overcome suboptimal regional incentives. Infrastructure often involves networks (transportation, electric, communications) whose local weaknesses can hamper the broader system.

Unfortunately, budgetary pressure has led national governments to austerity. Line items on the ledger are viewed as costs that should be controlled, even though infrastructure is more like an investment. If the investments aren’t made, the returns will not be realized.

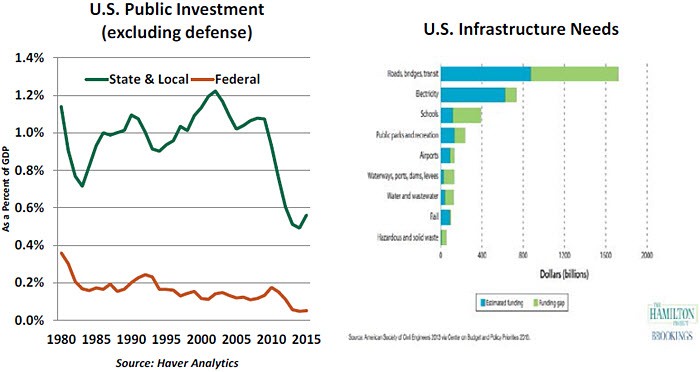

In some countries such as the U.S., the infrastructure effort is deeply fragmented. State and local governments bear much of the responsibility for public works in these places, and their efforts are often poorly coordinated. Local state and county budgets are often more stressed as they struggle with underfunded pensions and medical liabilities. This situation has led to deferred maintenance and a substantial infrastructure gap.

The American Society of Civil Engineers has estimated that an investment of $3.1 trillion would be required to bring U.S. infrastructure back to “good repair.” Globally, McKinsey estimates that an annual gap of $800 billion exists between what is spent and what is needed. And those figures only include maintenance, not expansion.

Studies also suggest that the monies being spent are not always used wisely. Patronage comes into play in the awarding of contracts; scope creep and cost overruns are common. In some jurisdictions, the permitting process is byzantine, costing time and money. As bad outcomes accumulate, the willingness of taxpayers to support projects diminishes.

Further, the failure to optimize plans across broad geographies invites inefficiency. As each district thinks only of its own needs, project designs fail to consider important interconnections. McKinsey estimates that a more efficient approach could save $1 trillion annually across the globe.

This mismatch between economic ideals and political realities exists in many arenas. But in the case of infrastructure, misaligned incentives and short-termism are especially pernicious. The current funding model seems in serious need of re-evaluation. Some new ideas have been advanced: the United Kingdom has asked its public pension systems to increase its investments in infrastructure, while the U.S. is contemplating an investment requirement as part of any tax strategy to repatriate corporate profits currently stranded overseas. But something more comprehensive is called for.

Pushing Partnership

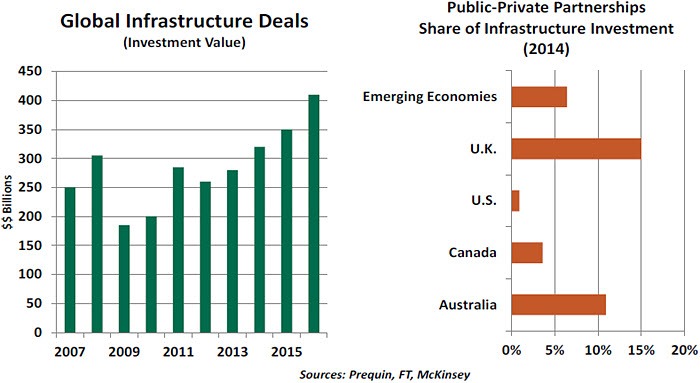

To break through current frictions, public-private partnerships (PPPs) are gaining currency. In some sense, all infrastructure projects are partnerships between government and industry; contracts are let out for bid, and providers carry out the work. But modern-day PPPs take that concept further. Investment groups contract with the government to build and manage public works, offering capital up front for a share of the revenue generated by the project.

To break through current frictions, public-private partnerships (PPPs) are gaining currency. In some sense, all infrastructure projects are partnerships between government and industry; contracts are let out for bid, and providers carry out the work. But modern-day PPPs take that concept further. Investment groups contract with the government to build and manage public works, offering capital up front for a share of the revenue generated by the project.

A simple example of a PPP is a toll road. Private capital pays for construction and is rewarded with toll collections. Fees are paid directly by those who use the facilities, often in a painless way (in this case, through windshield transponders). Ports are another common expression of PPPs: funds raised from investors can be used to dredge deeper channels and develop intermodal logistics. Returns can be generated from docking fees.

PPPs have the favorable financial optics of keeping project costs off the public budget. Investors receive regular and attractive returns. (Infrastructure investments have produced annual returns of nearly 9% since 2003, with a variance lower than that of equities.)

But PPPs can be controversial. Terms intended to protect residents from increases in fees diminish the attraction to investors. When stress occurs, Main Street is pitted against Wall Street. This was illustrated in a recent example involving new water infrastructure in New Jersey; residents have trouble comprehending the costs involved and resent paying the fees necessary to bring facilities up to date.

The responsibility for this stress rests primarily with politicians, whose failure to appropriate funds for routine maintenance has created the context for even bigger costs down the road. (And a tax-adverse public has not been anxious to press them on this point.) Yet public servants find it convenient to deflect the blame to investors, so as to maintain good electoral standing.

PPPs may not lend themselves well to projects that might be badly needed but which are not easily monetized. The acts of repairing roads, modernizing air traffic control systems or building schools don’t spin off the kinds of cash flows that attract investment. Further, some are concerned that public officials will be outmatched in negotiations and will end up giving away the store (or the highways).

Some countries have turned to national infrastructure boards, whose members are charged with thinking beyond the political cycle. But for larger economies, entrenched interests and bureaucracies present difficulties in transitioning to that kind of model.

Infrastructure and Influence

While most countries have trouble investing sufficiently in domestic infrastructure, China has recognized that offering funds to other countries for infrastructure serves multiple purposes. It increases demand for the raw materials (like cement) that it has in surplus, keeping plants running and employment up. It opens up channels for the sale of additional Chinese products. And it is an investment in diplomacy, currying strategic favor with recipients.

China took a substantial step a few years ago when it championed the formation of the Asian Infrastructure Investment Bank (AIIB). The Bank, which began operation last year, aims to finance projects across a wide range of countries. China is also investing directly, under its “One Belt, One Road” program. $40 billion has been committed to the effort, which will be directed to rails, roads, ports and pipelines. The hope is not just for investment returns and expanded commerce, but global influence.

China took a substantial step a few years ago when it championed the formation of the Asian Infrastructure Investment Bank (AIIB). The Bank, which began operation last year, aims to finance projects across a wide range of countries. China is also investing directly, under its “One Belt, One Road” program. $40 billion has been committed to the effort, which will be directed to rails, roads, ports and pipelines. The hope is not just for investment returns and expanded commerce, but global influence.

Suspicious of China’s motivations, the U.S., the U.K. and Japan declined to participate in the AIIB. But 56 other countries did. The West may have played its hand badly, and is now seen as less supportive of the region. (The recent decision of the U.S. to withdraw from the Trans-Pacific Partnership only cements that reputation.) Geopolitical rivalries are of limited interest to populations without running water.

But budget realities may limit these lofty ambitions. There are questions about whether China can follow through on the commitment it has made to infrastructure development. The country’s reserves are dwindling, and financial excesses may force credit conservatism. A new cast of Chinese financial leaders was announced this week; they may be tasked with cooling overheated markets.

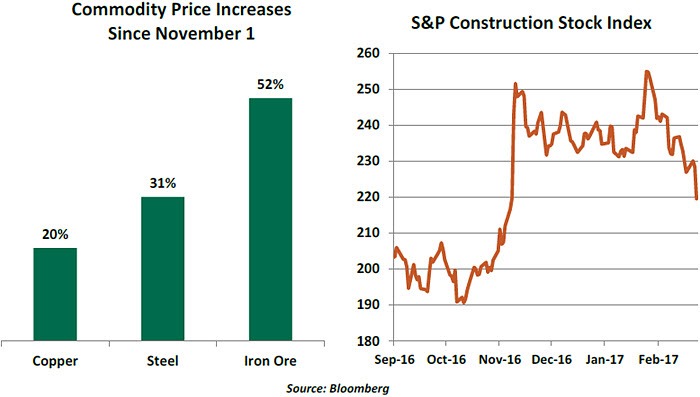

The post-election period in the U.S. generated considerable excitement in the infrastructure arena. President Trump has proposed a $1 trillion program, which would be the largest in the nation’s history. The effort seems to be among the few things that could attract bipartisan support, given critical needs in this area. Commodity prices and shares of construction firms have consequently soared since Election Day.

However, fiscal conservatives will certainly insist on new revenues or cost cuts to pay for new programs. There is little fat to cut on the spending side, especially if the Congress follows through with plans to expand defense outlays. The only new tax being contemplated is a border tax, which could produce a series of unpleasant side effects (discussed here). Opposition to this tactic may limit aspirations to expand public investment.

Infrastructure is at once essential and impossible, local and global, strategic and tactical. Those contradictions make it difficult to design and execute programs that deliver on the great promise that infrastructure offers. Infrastructure done well would be hugely beneficial to the global economy; done poorly, it could make matters considerably worse.

Infrastructure is at once essential and impossible, local and global, strategic and tactical. Those contradictions make it difficult to design and execute programs that deliver on the great promise that infrastructure offers. Infrastructure done well would be hugely beneficial to the global economy; done poorly, it could make matters considerably worse.

It will take significant powers of vision and persuasion to advance the cause. And maybe some inspiration from above.

Unfortunately, budgetary pressure has led national governments to austerity. Line items on the ledger are viewed as costs that should be controlled, even though infrastructure is more like an investment. If the investments aren’t made, the returns will not be realized.

In some countries such as the U.S., the infrastructure effort is deeply fragmented. State and local governments bear much of the responsibility for public works in these places, and their efforts are often poorly coordinated. Local state and county budgets are often more stressed as they struggle with underfunded pensions and medical liabilities. This situation has led to deferred maintenance and a substantial infrastructure gap.

The American Society of Civil Engineers has estimated that an investment of $3.1 trillion would be required to bring U.S. infrastructure back to “good repair.” Globally, McKinsey estimates that an annual gap of $800 billion exists between what is spent and what is needed. And those figures only include maintenance, not expansion.

Studies also suggest that the monies being spent are not always used wisely. Patronage comes into play in the awarding of contracts; scope creep and cost overruns are common. In some jurisdictions, the permitting process is byzantine, costing time and money. As bad outcomes accumulate, the willingness of taxpayers to support projects diminishes.

Further, the failure to optimize plans across broad geographies invites inefficiency. As each district thinks only of its own needs, project designs fail to consider important interconnections. McKinsey estimates that a more efficient approach could save $1 trillion annually across the globe.

This mismatch between economic ideals and political realities exists in many arenas. But in the case of infrastructure, misaligned incentives and short-termism are especially pernicious. The current funding model seems in serious need of re-evaluation. Some new ideas have been advanced: the United Kingdom has asked its public pension systems to increase its investments in infrastructure, while the U.S. is contemplating an investment requirement as part of any tax strategy to repatriate corporate profits currently stranded overseas. But something more comprehensive is called for.

Pushing Partnership

A simple example of a PPP is a toll road. Private capital pays for construction and is rewarded with toll collections. Fees are paid directly by those who use the facilities, often in a painless way (in this case, through windshield transponders). Ports are another common expression of PPPs: funds raised from investors can be used to dredge deeper channels and develop intermodal logistics. Returns can be generated from docking fees.

PPPs have the favorable financial optics of keeping project costs off the public budget. Investors receive regular and attractive returns. (Infrastructure investments have produced annual returns of nearly 9% since 2003, with a variance lower than that of equities.)

But PPPs can be controversial. Terms intended to protect residents from increases in fees diminish the attraction to investors. When stress occurs, Main Street is pitted against Wall Street. This was illustrated in a recent example involving new water infrastructure in New Jersey; residents have trouble comprehending the costs involved and resent paying the fees necessary to bring facilities up to date.

The responsibility for this stress rests primarily with politicians, whose failure to appropriate funds for routine maintenance has created the context for even bigger costs down the road. (And a tax-adverse public has not been anxious to press them on this point.) Yet public servants find it convenient to deflect the blame to investors, so as to maintain good electoral standing.

PPPs may not lend themselves well to projects that might be badly needed but which are not easily monetized. The acts of repairing roads, modernizing air traffic control systems or building schools don’t spin off the kinds of cash flows that attract investment. Further, some are concerned that public officials will be outmatched in negotiations and will end up giving away the store (or the highways).

Some countries have turned to national infrastructure boards, whose members are charged with thinking beyond the political cycle. But for larger economies, entrenched interests and bureaucracies present difficulties in transitioning to that kind of model.

Infrastructure and Influence

While most countries have trouble investing sufficiently in domestic infrastructure, China has recognized that offering funds to other countries for infrastructure serves multiple purposes. It increases demand for the raw materials (like cement) that it has in surplus, keeping plants running and employment up. It opens up channels for the sale of additional Chinese products. And it is an investment in diplomacy, currying strategic favor with recipients.

Suspicious of China’s motivations, the U.S., the U.K. and Japan declined to participate in the AIIB. But 56 other countries did. The West may have played its hand badly, and is now seen as less supportive of the region. (The recent decision of the U.S. to withdraw from the Trans-Pacific Partnership only cements that reputation.) Geopolitical rivalries are of limited interest to populations without running water.

But budget realities may limit these lofty ambitions. There are questions about whether China can follow through on the commitment it has made to infrastructure development. The country’s reserves are dwindling, and financial excesses may force credit conservatism. A new cast of Chinese financial leaders was announced this week; they may be tasked with cooling overheated markets.

The post-election period in the U.S. generated considerable excitement in the infrastructure arena. President Trump has proposed a $1 trillion program, which would be the largest in the nation’s history. The effort seems to be among the few things that could attract bipartisan support, given critical needs in this area. Commodity prices and shares of construction firms have consequently soared since Election Day.

However, fiscal conservatives will certainly insist on new revenues or cost cuts to pay for new programs. There is little fat to cut on the spending side, especially if the Congress follows through with plans to expand defense outlays. The only new tax being contemplated is a border tax, which could produce a series of unpleasant side effects (discussed here). Opposition to this tactic may limit aspirations to expand public investment.

It will take significant powers of vision and persuasion to advance the cause. And maybe some inspiration from above.

Author

Northern Trust Economic Research Department

Northern Trust

More from Northern Trust Economic Research Department