G10 FX talking: Tightening cycles coming to a close

Some early action from policymakers on both sides of the Atlantic has seen risk assets recover some ground and the dollar weaken. A further dollar decline looks likely this year, although we suspect this is more a story for the second half when the Fed can declare that the inflation battle is won. Expect steady outperformance of the yen through the year.

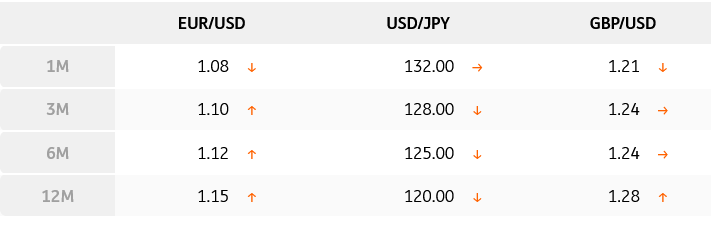

Main ING G10 FX forecasts

↑ / → / ↓ indicates our forecast for the currency pair is above/in line with/below the corresponding market forward or NDF outright

Source (all charts and tables): Refinitiv, ING forecast

EUR/USD: A case of when, not if the dollar declines

-

The collapse of two regional banks in the US has seen the Fed take action to address financial stability, while at the same time tightening rates to address monetary stability. We expect these two positions to collide in the second half of this year, where tighter credit conditions and greater evidence of a hard landing could see the Fed cut rates 100bp in 4Q23. It is a question of when, not if the dollar declines.

-

Timing that sell-off is difficult. It is hard to rule out more stress emerging this quarter – especially if the Fed delivers one more 25bp rate hike. Thus, we favour a 1.05-1.10 range over coming months.

-

But the European financial sector looks better positioned than the US. Higher for longer European Central Bank rates target EUR/USD at 1.15 by year-end.

USD/JPY: The Bank of Japan can add to the yen’s appeal

-

A lower USD/JPY is becoming the market’s conviction call. It covers both the potential for a sharp Fed easing cycle and frailty in the US financial system. Also, there is the wild card risk event of a change in BoJ policy. At the 16 June meeting, we think the BoJ could shorten its yield curve target to 5-year from 10-year JGB yields. 10-year JGB yields would rise sharply, and the yen would rally. That’s why we target 128 for USD/JPY at end-June.

-

Expect much focus on new BoJ governor, Kazuo Ueda, over coming months and what he has to say about recent wage trends and whether dovish policy has out-served its time.

-

One risk we see to the bearish USD/JPY call is energy prices. Our team is calling Brent to $110/bbl by year-end – a yen negative.

GBP/USD: Surprising sterling strength

-

We have been surprised by sterling strength in March. Given the UK’s large current account deficit and its large financial sector, we'd have thought it would have underperformed during the recent financial turmoil. We suspect that positioning may have played a role in sterling’s rally in March – where asset managers wrong-footed in bond markets also had to cover short sterling positions.

-

What now? Based on our EUR/USD view for the second quarter, we suspect GBP/USD may bounce around in a 1.20-1.25 range. Events in the US, however, give us greater conviction that it trades at 1.28/1.30 later in the year as the Fed pushes through with easing.

-

An early pause from the BoE in May could also support the view that GBP/USD will struggle to sustain a move above 1.25 in the second quarter.

EUR/JPY: Downside looks more inviting

-

EUR/JPY briefly traded below 139 at the height of the US banking crisis only to trade to 145 as conditions settled. We suspect the risk environment remains fragile – the KBW US Regional Banking index continues to drop – and that EUR/JPY can turn lower again.

-

From the eurozone side, growth is weak and stressed markets could make the case that the ECB does not need to tighten much more. We look for 25bp hikes from the ECB in May and June, but no cuts until the third quarter of next year. The BoJ is at the other end of the spectrum, turning less dovish and possibly even hiking rates early in 2024.

-

EUR/JPY is normally a good barometer for global growth and the forthcoming downturn favours a multi-quarter drop to 135.

EUR/GBP: Non-consensus BoE view leaves GBP vulnerable

-

Our macro team thinks the Bank of England may have completed its tightening cycle with a 25bp hike to 4.25% in April. This is at odds with the market pricing a further 35bp of tightening over the next couple of months. A BoE pause should be a slight sterling negative. And assuming the ECB takes its own deposit rate (floor on overnight rates) to 4.00% in June, EUR/GBP should gravitate back to the 0.89 area.

-

As we mentioned last month, we doubt the improvement in UK-EU relations delivers material improvement to sterling yet and the sterling rally in March had more to do with positioning.

-

As an aside, local UK elections in May might provide some insights into how well the Labour Party is really doing.

EUR/CHF: Swiss National Bank to remain in control

-

Despite the Credit Suisse debacle, EUR/CHF has traded in a reasonably narrow range of 0.9850-1.000 over recent weeks. Probably limiting the topside at 1.00 has been the Swiss National Bank. Here, the SNB increasingly tells us it has been selling FX reserves to keep CHF stable – largely in line with monetary rather financial stability priorities. The SNB sold

-

CHF27bn of FX in the fourth quarter of 2022.

-

Last year we had felt that the SNB would want a lower EUR/CHF to help fight inflation. It is still threatening another hike – we look for a final move in the policy rate to 1.75% in June.

-

But the financial stress and weaker economic outlook probably means the SNB prefers a 0.98-1.00 range near term.

EUR/NOK: Let the rollercoaster continue

-

Krone volatility remains very elevated, and despite the hawkish turn by Norges Bank likely aimed at offering support to the currency, intermittent selloffs have remained the norm.

-

We doubt this will change soon, even if fundamentals point at NOK appreciation, especially after the OPEC+ cuts enhanced the oil price outlook and Norges Bank turned more hawkish. Liquidity conditions in the FX market need to improve and volatility needs to abate before NOK can enjoy a sustained recovery.

-

Our view is that 11.00 can be touched in EUR/NOK by the end of this quarter on the back of easing appreciating pressure on the euro side and improving sentiment. But it won’t be a smooth ride.

EUR/SEK: Riksbank walking a narrow path to save the krona

-

The Riksbank has stuck to its hawkish, SEK-supporting tone, as inflation rose in February. Wage negotiations yielded a 7.4% increase for the next two years, which may ease fears of a wage-price spiral. Still, a 50bp April hike looks likely given SEK weakness.

-

Meanwhile, the economic backdrop in Sweden remains concerning. The house price slump accelerated in March (-0.8% MoM) and retail sales fell 9.4% in February. March’s activity surveys were slightly more encouraging.

-

Perceived FX intervention risk may be on the rise, but we think the RB won’t go beyond mere threats. Short-term upside risks for EUR/SEK remain material. While the path for a SEK recovery is quite narrow, we expect EUR/SEK to move below 11.00 in the second half of 2023 thanks to improved risk sentiment and Riksbank tightening.

EUR/DKK: DN should replicate ECB rate hikes

-

Danmarks Nationalbank refrained from intervening in the currency market for a second consecutive month. This was justified by EUR/DKK rising to the 7.4500 area.

-

Moving ahead, we expect two more 25bp rate hikes by DN this year, in line with our ECB call. At this stage, there is no clear need to widen the rate gap with the ECB given the higher EUR/DKK.

-

Incidentally, inflation in Denmark proved rather sticky in February, which underpins tightening beyond the mere FX sphere. With FX intervention and smaller rate hikes compared to the ECB ready to be deployed if needed, EUR/DKK should stay around 7.45 and rise to 7.46 around the turn of the year.

USD/CAD: Loonie still lacking the hawkish factor

-

The US banking troubles initially weighed on CAD, but now, with financial risks having abated and oil prices shifting higher on OPEC+ supply crunch, CAD’s attractiveness has improved.

-

However, the Bank of Canada remains a dovish standout. While the door will remain open to more tightening if needed, it’s looking increasingly likely the next move will be a cut. Core inflation measures have declined below 5.0%, and despite better-than-expected growth, the BoC Business Outlook Survey showed worsening sentiment as a result of monetary tightening.

-

Investors may still favour pro-cyclical currencies backed by hawkish central banks than by a commodity push, and the USD/CAD decline may remain primarily a USD decline story.

AUD/USD: Dealing with the Reserve Bank of Australia pause

-

The Aussie dollar was the worst-performing currency in March when CPI data (for February) showed a surprise decline below 7.0% and fuelled dovish speculation on the RBA.

-

Those expectations were matched by a pause at the April meeting. Despite efforts by Governor Philip Lowe to suggest more hikes are possible, markets aren’t pricing any more tightening. We think another 25bp is possible, but that would mark the peak.

-

With the RBA no longer offering AUD a hawkish undercurrent, further gains in the currency would need to be mainly driven by a benign USD decline, positive spill-over from China’s growth story and supportive risk environment. We have trimmed our AUD/USD profile but remain moderately bullish in the medium term.

NZD/USD: RBNZ went big, but may have to cut big

-

The Reserve Bank of New Zealand surprised with a 50bp rate hike in April, but NZD failed to find support after an initial jump. The OIS curve embeds another 25bp hike, in line with the Bank’s projections.

-

Most importantly, there are quite contained market expectations about rate cuts later in the year. Inflation may well fall faster than the RBNZ expects and with the housing market slump weighing on the already fragile economy, markets may soon price in rate cuts in the second half of 2023, in line with the Fed.

-

Accordingly, we are reluctant to jump into RBNZ-led New Zealand dollar rallies in the crosses. Still, NZD/USD can rise on a weak USD and improved risk sentiment, as well as a supportive China narrative.

Read the original analysis: G10 FX talking: Tightening cycles coming to a close

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.