Forex majors settle down ahead of Non-farm Payrolls

Market Overview

The dollar has just dropped away a touch in the wake of the announcement of both the Republican tax reform bill but also Donald Trump’s pick of Powell for the next Fed chair. Tax reform is likely to be a long hard slog and the market is right to look at its progress with slight caution, whilst Powell is a continuity choice for Fed chair who in isolation will do little to shift the path of rate normalisation. That now means today that markets are settling down for the announcement of Non-farm Payrolls. Subsequently there is little decisive move across Treasury yields or major forex pairs. Part of the reason could be the fact that the market faces the prospect of another very mixed, hurricane impacted payrolls report. Having seen surprise job losses last month, the needle is set to swing the other way with massive job gains. In addition to likely revisions, this could be a report that sees algo-driven volatility on the announcement but once the dust settles, the market pays little real regard to.

Wall Street closed at all-time highs again yesterday on both the Dow (+0.3%) and S&P 500 (+0.02% at 2580). However the mixed moves on the session suggest uncertainty. This mixed mood continued in Asian trading (Nikkei +0.5%) whilst European markets are slightly positive in early moves, however with the prospect of payrolls ahead, these moves could be limited. In forex, the G4 currencies are showing very slight dollar positive bias as the European session takes over, whilst the Kiwi continues its near term recovery, although the Aussie has been hit by weaker than expected Australian retail sales. The consolidating dollar means that in commodities we see gold and silver hovering around the flat line, whilst oil has edged slightly higher.

Given the hurricane disruption, this will be another very difficult Employment Situation report to decipher. The data is released at 1230GMT and the headline Non-farm Payrolls are expected to show a rise of +310,000. Coming after a huge miss last month down to -33,000 this is a wild swing back higher in job creation. Expect significant revisions to prior months, but also reading into the implications of the headline numbers will be a tricky task. Focus could therefore come on the Average Hourly Earnings which are especially in vogue at the moment, with the with Phillips Curve gaining so much attention. Wages are expected to have risen by +0.2% for the month (down from +0.5% last month) and +2.7% for the year (down from +2.9%). Also look at the unemployment rate which is expected to stick at 4.2%, but also the U6 underemployment which fell from 8.6% to 8.3% last month. Also the laborforce participation rate is key having increased sharply last month to 63.1% which was the highest since May 2014.

Non-farm Payrolls will be key for traders today, however there is also the important services PMIs to take into consideration too. The UK kicks off the releases with UK Services PMI at 0930GMT which is expected to slip slightly to 53.3 (from 53.6). This would be the sixth month that the services PMI has hovered between 53.2/53.8 and again will be keenly watched by sterling traders with the services sector accounting for around 80% of the UK economy. The ISM Non-Manufacturing data is at 1400GMT and is expected to drop back to 58.5 from a two year high of 59.8 last month. Factory orders are also at 1400GMT and are expected to have increased by +1.3% in September (+1.2% last month).

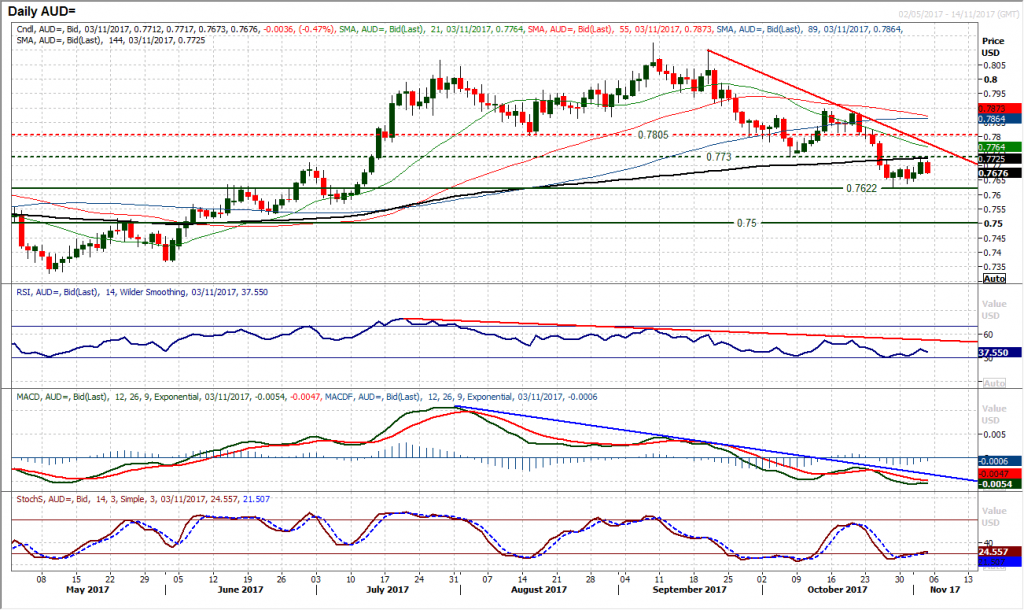

Chart of the Day – AUD/USD

After a bit of a torrid time recently, the commodity currencies have just show signs of recovery, with the Kiwi having rallied but also the Aussie too. The question is whether this is a sustainable turnaround. The strong bull candle from yesterday took the price to a one week high to suggest that the old key long term pivot (and key October low) at $0.7730 could now be tested. However already we are finding the rebound tested as the Aussie has dropped back on weaker Australian retail sales. The market is already questioning the rebound. Looking at the momentum indicators, this becomes more clear, with the recent rally looking to be an unwind within the medium term bear market, with downtrends on both RSI and MACD lines suggesting rallies remain a chance to sell. Subsequently, I expect the rally to struggle and another lower high to form possibly in the “sell zone” between $0.7730/$0.7805. There is also a downtrend linking recent highs that comes in around $0.7780 today and this may come into play too, however rallies are a chance to sell. The hourly chart shows the near term improvement in outlook is already being tested. Initial support is at $0.7660 but on a medium term basis a retest of the $0.7622/$0.7637 lows is likely in due course.

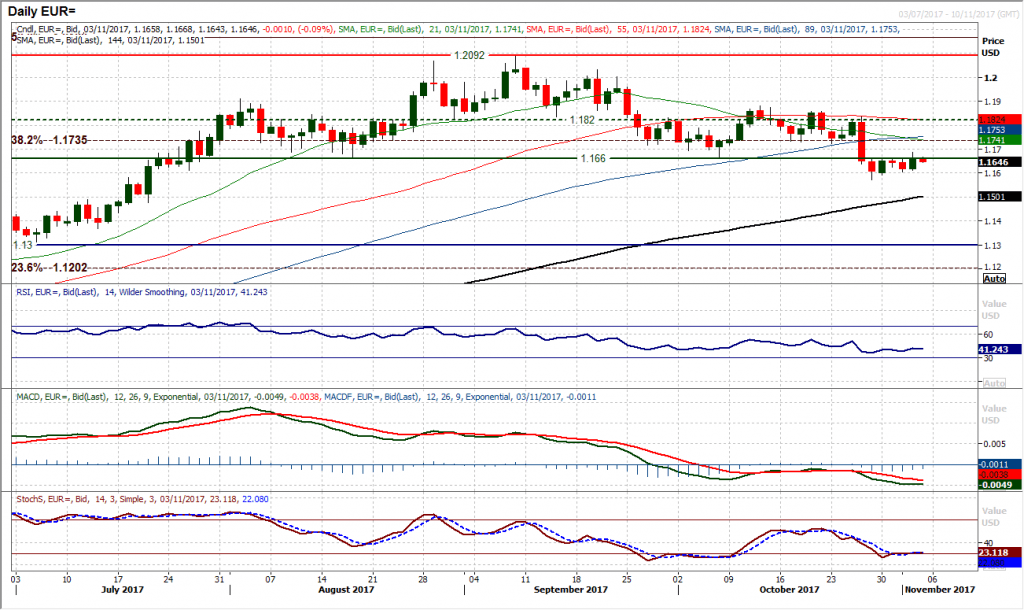

EUR/USD

On a medium term basis, rallies on EUR/USD are a chance to sell. In the wake of the announcement of the US tax reform bill and Powell as the next Fed chair, the dollar has weakened a touch, but the significant overriding technical factor on EUR/USD remains the big head and shoulders top. Yesterday the market was again struggling around the neckline of $1.1660 and this remains a source of overhead supply, with a resistance band $1.1660/$1.1730. The early move today is once more around the neckline, but any rebound will ultimately prove to be a chance to sell. The near term technical outlook has improved a touch over the past day or so, with the uptick on the hourly momentum. However the recovery is likely to be short lived. Non-farm Payrolls is likely to produce some sizeable volatility today and any spike higher should be a chance (in the absence of a catastrophic report). Initial support at $1.1625 and then $1.1600 before the recent low of $1.1575. Resistance is initially $1.1687 and then $1.1730.

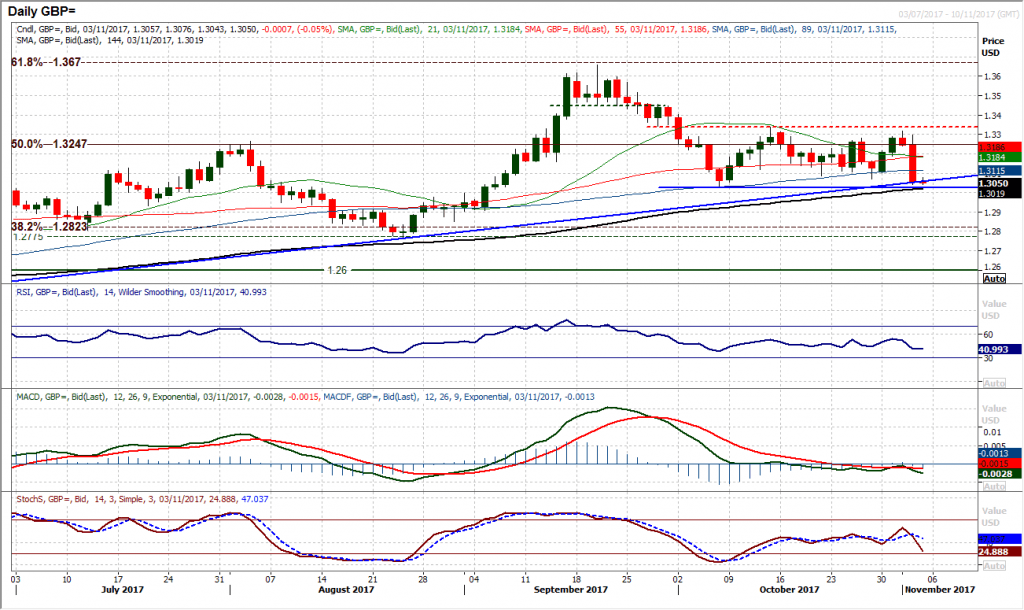

GBP/USD

A huge bear candle (that lost almost 190 pips on the day) on a “dovish hike” from the Bank of England has seen the long term uptrend come under threat. This means that Cable is now testing a confluence of key technical support and makes the coming sessions important. The uptrend of the past twelve months, is broadly around $1.3060 today, whilst the one month range low is at $1.3025 and the 144 day moving average (a long term trend indicator which has been supportive on the major corrections comes in around $1.3020 today. Momentum indicators have ticked lower in the wake of the strong bear move yesterday but nothing yet that would suggest a decisive downside break. That is why the bulls are key today as the market now knows the Bank of England’s policy stance whilst tax reform and a Fed chair Powell have also failed the break the long term trend. If the bulls come back in to support now this would be a strong signal of support above the $1.3000 psychological level. The market has begun to settle overnight and clearly Non-farm Payrolls could be an issue for volatility this afternoon. If the support can survive the payrolls report then bull confidence will be bolstered. A closing breach of $1.3000 opens $1.2800/$1.2900. There is minor resistance around $1.3120/$1.3150.

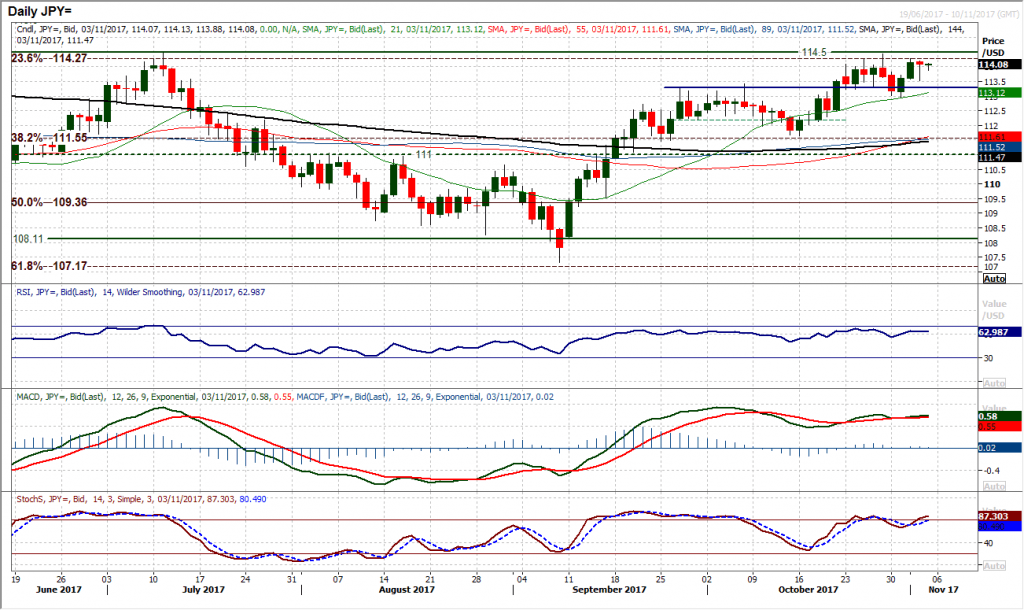

USD/JPY

The move to test 114.50 may have just been put on pause briefly however the bulls still have the key July resistance in sight. Yesterday’s candle is difficult to decipher as a long intraday downside shadow with a small negative real body can be taken two ways. Either the sellers are testing the water and this is a concern, or the bulls have fought back strongly to position well for another go at the resistance. Today’s session could be key to the answer and payrolls will play an important role in today’s move. The importance of yesterday’s low at 113.50 is elevated and a breach would begin to suggest the bulls have lost momentum for now. The support at 112.95 is key near term. With the positive configuration on the momentum indicators the suggestion is that the market should be pushing for a test of 114.50 and is my preferred positioning. However the volatility of what could be an extremely difficult payrolls to read into could mean a wild reaction.

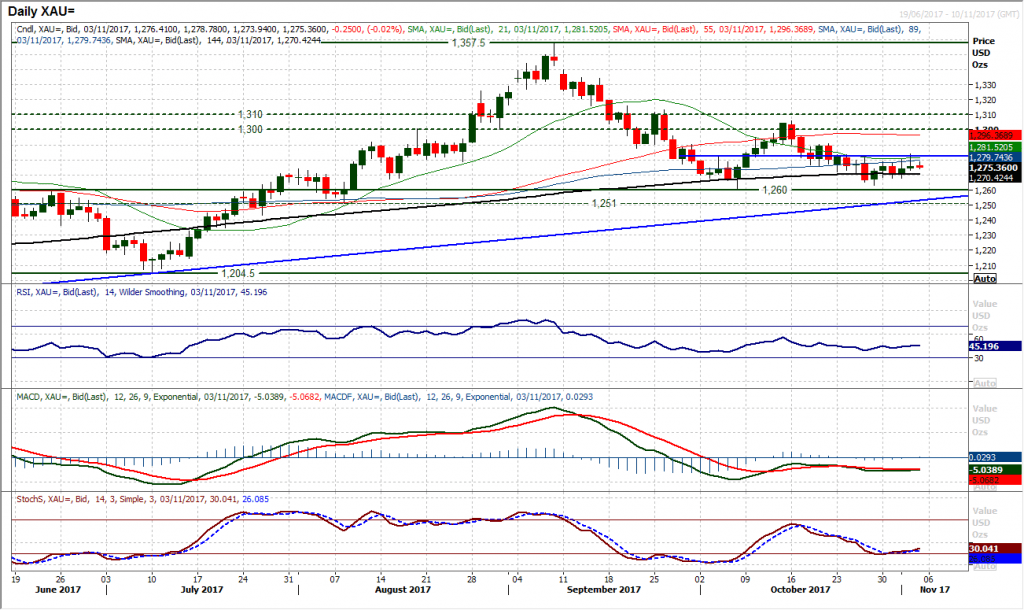

Gold

The chart analysis of gold is extraordinary at the moment. There seems to be an appetite for a rebound, however the bulls just cannot grasp their opportunity. Long upper tails and small candlestick bodies reflect a market testing the water only to be too timid the make the move. Uncertainty subsequently prevails and consolidation continues. There is the slightest of positive biases forming in the past couple of days on gold with the hourly chart showing the upside pressure on the resistance band $1282/$1284, however every time the market gets near this near term band of resistance there is a failure. Non-farm Payrolls will add to the mix of uncertainty today with a likely spike in volatility, however we will likely know a lot more about the near to medium term outlook as a result. Above $1284 opens $1291, whilst support comes initially around $1272 and then $1267 with $1263.30 being key.

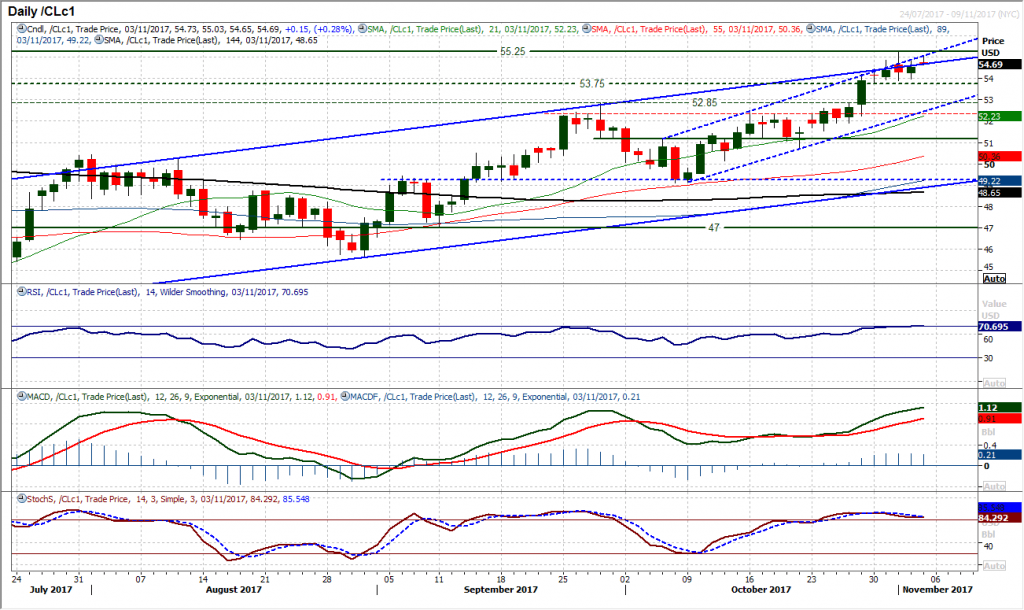

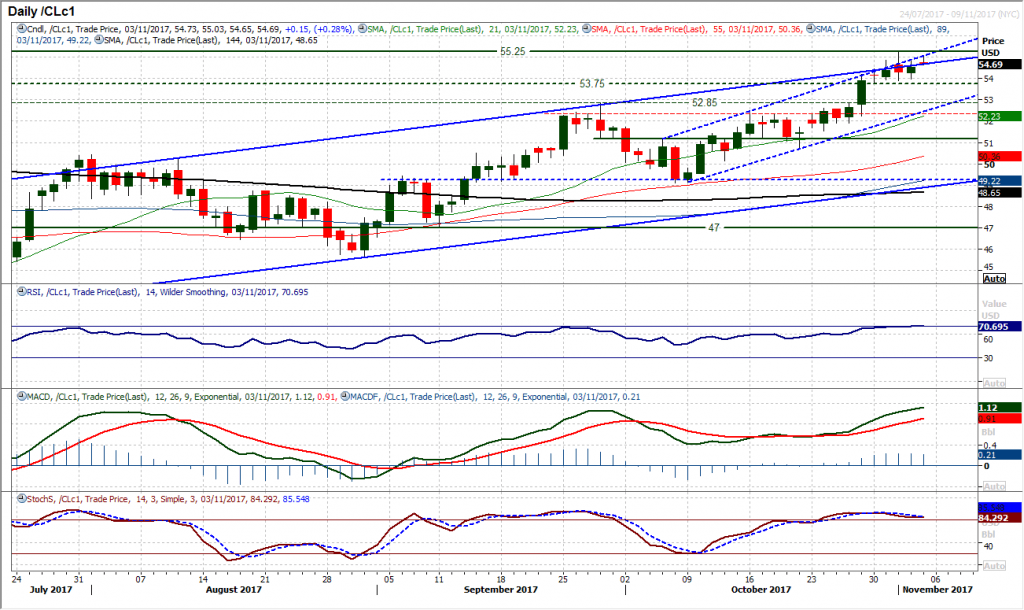

WTI Oil

The recent consolidation above the breakout of $53.75 continues. For now, whilst this support remains intact then the bulls remain in near term control, whilst yesterday’s mildly positive candle and today’s early gains continue this outlook. However the momentum indicators are beginning to look a little tired with the RSI stuttering around 70 and the Stochastics having crossed lower (although not yet confirmed as a corrective signal). A positive candle posted yesterday helps to settle the nerves following Tuesday’s negative candle but the potential for a correction remains. This is reflected in the hourly chart which shows a near term possible top, whilst the hourly MACD lines are suggesting the strength of the immediate bull control is a touch nervy. A move below $53.75 would open a correction of around $1.50 which would still be considered a chance to buy. Resistance at the 2017 high of $55.25 remains strong.

Dow Jones Industrial Average

The seven week uptrend continues to pull higher and the market remains supported. However the run of uncertain candles continues. For more than a week now the market has posted either negative candles or small bodied positive candles. This does not suggest there is much conviction with the run higher. This is reflected in the momentum indicators which are drifting a touch and do not have the impetus of earlier in the rally. “The trend is your friend until it ends” remains key however, and this means that optimism is still needed with the outlook, even if it needs to be cautious optimism. Yesterday’s all-time high of 23,531 is the initial resistance with yesterday’s traded low of 23,351 now a minor higher low above 23,328 and the key support 23,251. The hints of bearish divergence on the hourly momentum indicators have not been entirely dispelled with yesterday’s move higher, but as yet the bulls are still able to pull the market higher.

Author

Richard Perry

Independent Analyst