Will the RBA need to be more aggressive now?

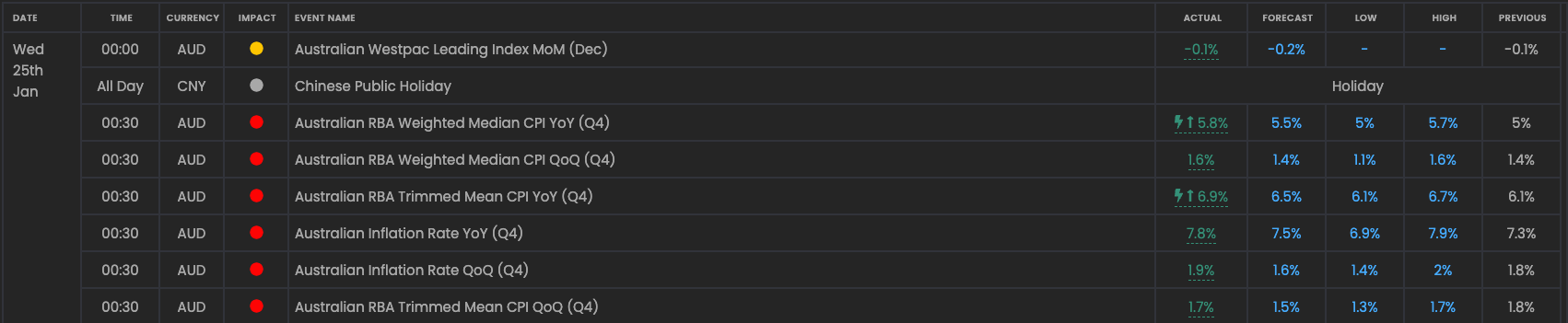

It was Australia’s inflation data this week that raised expectations for a more aggressive RBA. All the inflation metrics beat across the board and both, the trimmed mean and weighted median, printed above the market’s maximum expectations. See here for the prints from Financial Source’s calendar:

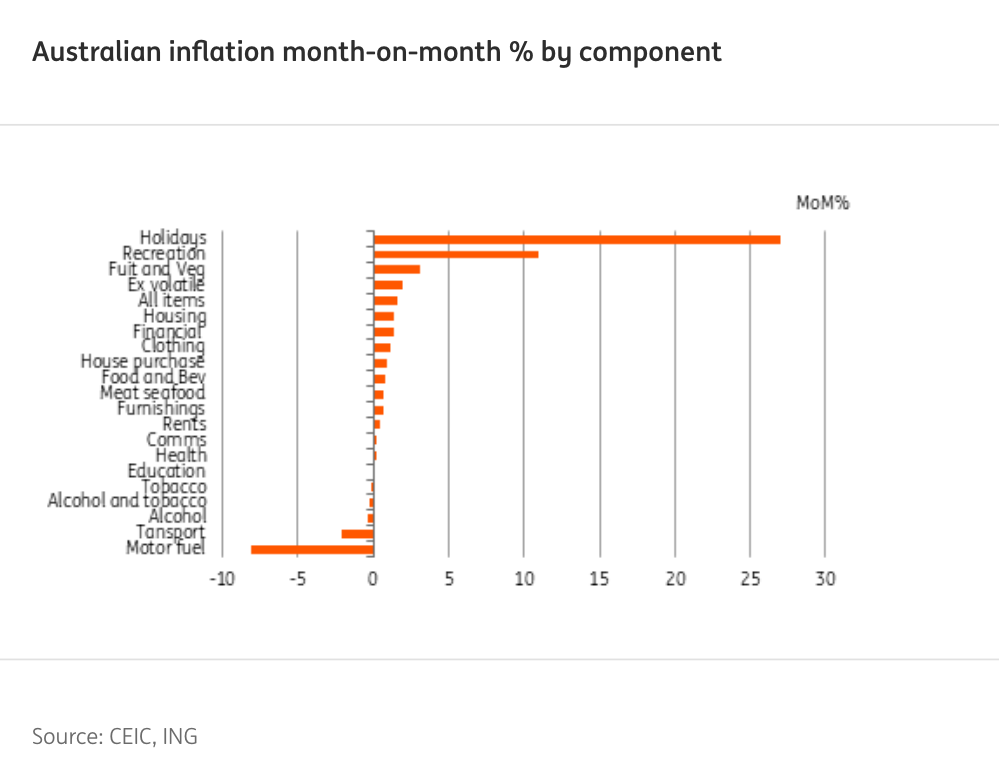

The headline figure for Q4 2022 rose to 7.8% from 7.3% in Q3 2022 and this shows a marked increase in inflationary pressures. However, the majority of that pressure came from one source – holidays. There were people taking holidays after long Covid waits that boosted demand. All in all the sector rose over 25% on a month-over-month basis. That’s a big move. So, the only good news is that the pressure should be a one-off. However, recreation and fruit and veg were the next big gainers for inflation on an m/m basis.

What this means for the RBA?

In a word, higher rates. Inflation is the number one target for central banks and that means expectations are now soaring for higher rates out of the RBA in its February meeting. Current expectations will now rise for a more aggressive RBA and a terminal rate that could rise higher than 3.5%. On balance, this should keep the AUD supported against the NZD. However, the real event to look out for is a big divergence between the RBA and the RBNZ.

-638103216379422085.png)

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.