We had dinner reservations not long ago, and I confidently led my family on a walk to the restaurant. But as the journey dragged on with the destination nowhere in sight, my family began to question my navigation. Well, that only served to increase my frustration and decrease my openness to feedback. Smart phone maps were proffered, but I stubbornly insisted on following the GPS in my head. Ultimately, we reached the restaurant a half hour late, and our table had been cedfed to others.

After taking time to calm down and reflect, I realized (once again) that you can never be totally certain about direction. You may think you see the path ahead clearly, but the journey can take unexpected turns that require re-orientation.

A couple of months ago, several things in the global economic landscape seemed nearly certain. The U.S. was going to outperform the eurozone, oil prices were going to remain depressed, the dollar was going to get stronger, and the world was likely to remain mired in a disinflationary spiral from which there seemed little hope of escape. All of that, plus the aggressive quantitative easing (QE) program from the European Central Bank (ECB), promised to place sustained downward pressure on long-term interest rates in developed markets.

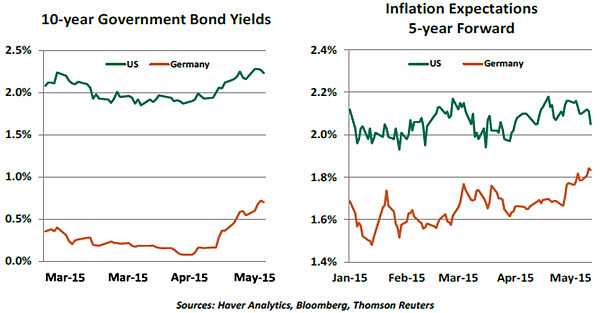

Well a funny thing happened on the way to lower yields: bond markets have been selling off almost persistently since the second quarter began. And most surprisingly, the yield on 10-year German government bonds has risen from nearly zero to almost 70 basis points since mid-April.

Many factors bear on long-term interest rates. But it seems that two main elements are primarily at play.

The first is a significant re-evaluation of inflation prospects. As shown in the chart above, implied inflation expectations have been rising. This is, in part, a reflection of the two-month rally in oil prices, which have risen from about $43 per barrel in March (for West Texas Intermediate crude) to the current level of nearly $60. Inflation expectations tend to follow energy prices quite closely, and the actual price level will surely follow upward in the months ahead.

The recovery in oil prices is as mysterious as the decline that preceded it, so it is hard to know what might be ahead. As James Pressler describes in a companion piece later in this commentary, the world’s leading producers are locked into an intricate contest for market share.  Another contributor to the re-evaluation of inflation seems to be a belief that the world’s central banks are going to be successful in their war against disinflation. The ECB’s purchases of debt may have the direct impact of pushing yields down, but recent news of improving economic performance had the opposite effect.

Another contributor to the re-evaluation of inflation seems to be a belief that the world’s central banks are going to be successful in their war against disinflation. The ECB’s purchases of debt may have the direct impact of pushing yields down, but recent news of improving economic performance had the opposite effect.

More upbeat readings from the eurozone have led some to wonder whether the ECB will end QE before its stated target of September 2016. But this is highly unlikely. As we discussed in our April 24 commentary, the unevenness of European performance and the absence of structural reform in key countries will probably continue to limit economic achievement on the Continent for some time to come. And the ECB risks losing some credibility and its hold on market expectations if it reverses such strong forward guidance so soon after establishing it.

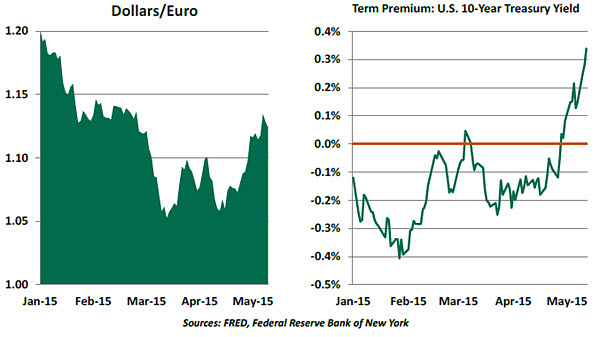

Still, first quarter growth in the eurozone was much better than it was in the United States. This reversal of fortunes halted the dollar’s march to parity against the euro and may have eased fears that America would import lower inflation.

The dollar may yet find the strength predicted for it. But the rude interruption of what seemed like a reliable trend clearly caught currency markets off-guard. The consequent reversal of trading positions, amid markets with fewer active broker/dealers present, has added a technical element to the correction in global interest rates.

The other element pushing yields upward is the “term premium.” A lot can happen during the course of a 10-year investment, and so bondholders typically like to be compensated for the uncertainty. The size of this compensation depends on the degree of perceived volatility in the outlook.  It is arguably this aspect that is most at play in the United States, where 10-year yields have risen 40 basis points in less than a month. Market expectations for Federal Reserve action have vacillated quite a bit over the past few weeks; a prospective interest rate increase was pushed into 2016 when disappointing results for the first quarter were released, but the strong employment report seems to have brought that possibility forward again. With no calendar-based guidance in the Fed’s most recent statements, market participants are guessing more than ever on how the central bank will weigh incoming data; that will tend to drive term premiums higher.

It is arguably this aspect that is most at play in the United States, where 10-year yields have risen 40 basis points in less than a month. Market expectations for Federal Reserve action have vacillated quite a bit over the past few weeks; a prospective interest rate increase was pushed into 2016 when disappointing results for the first quarter were released, but the strong employment report seems to have brought that possibility forward again. With no calendar-based guidance in the Fed’s most recent statements, market participants are guessing more than ever on how the central bank will weigh incoming data; that will tend to drive term premiums higher.

Global growth remains somewhat tepid, and there is “event risk” surrounding Greece and other hot spots. So safe assets will continue to attract a lot of interest, and sovereign yields are likely to remain quite low by historical standards.

But the route from the present position to the ultimate destination is rarely a straight line. That is the learning I arrived at while eating a cold takeout meal that fateful evening, amid a very cold attitude from my family.

The Pendulum at the Pump

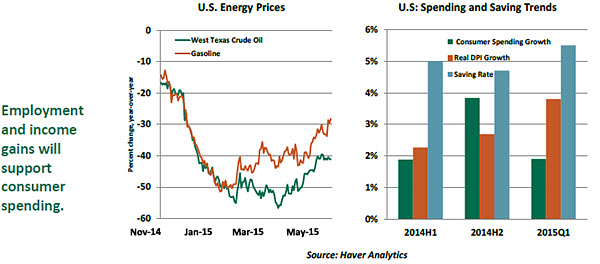

Energy prices have moved up in the past four months, with gasoline prices posting a larger increase than crude oil prices in the United States. The two have decoupled somewhat after declining in synch during the latter portion of last year.

Many are wondering how these movements in gasoline prices will affect U.S. consumer spending. Three questions need to be answered to assess the likely impact:

- Why are gasoline prices rising faster than crude oil prices in the United States?

- Did consumers use or save the extra dollars from lower gasoline prices in the second half of 2014?

- What other factors are influencing spending patterns?

Starting with the first question, gasoline prices have moved up 61% since the January low, whereas crude oil prices have increased 36%. Refinery capacity was reduced in the United States due to scheduled and unscheduled maintenance caused by bad weather. These refinery issues curtailed gasoline availability and exacerbated the increase in crude oil prices.

Refinery issues are a thing of the past now, but gasoline prices are still increasing in anticipation of higher demand during the summer driving months. Yet there are ample inventories of crude oil and gasoline. Analysts expect production of crude oil to increase in the United States with the price trading upwards of $60. Oil rigs that shut down at lower prices are likely to resume operations and lift supply. If crude oil continues to trade at current or higher levels, previous projections of output and prices will have to be revised.

Moving on to the second question, U.S. consumer spending rose at a higher pace in the second half of last year than the first half of last year. Real disposable personal income (DPI) also advanced in the second half of 2014 but at a slower pace compared with consumer spending, which leads us to conclude that a part of the increase in consumer spending stemmed from an energy price “dividend.” Nonetheless, all evidence suggests that a big portion of the energy price benefit has been used to pay down debt and increase saving.

There is speculation that the higher saving trajectory reflects consumers considering the windfall from falling energy prices to be temporary. There is probably some truth in this hypothesis, and this year’s partial reversion in gasoline prices may confirm this expectation. But on close inspection, real disposable income also advanced in the first quarter of this year and yet consumer spending still grew slowly. This gives weight to the notion that weather most likely held back consumer spending in the early months of the year.

Finally, the last question: will the recent jump in gasoline prices will hold back consumer spending? According to the Automobile Association of America, gasoline prices are still about $1 a gallon below a year ago. Current gasoline prices are the lowest at this time of the year since 2010. In other words, gasoline is not oppressively expensive and unlikely to require a reallocation of household budgets around current prices.

Looking ahead, the following observations help put things in perspective. The inventory situation of crude oil and gasoline suggests there are no worrisome price pressures from lean inventories. Global growth is projected to be modest, implying that demand pressures should be contained. These factors suggest that a large hike of gasoline prices has a low probability, barring adverse geopolitical developments.

The fluctuations seen in gasoline prices over the past nine months have been difficult for both consumers and economists to interpret. But energy is still considerably less expensive than it has been for quite a while, and other household fundamentals are strengthening. This augurs very well for U.S. consumption during the balance of 2015.

The Oil Game Theory

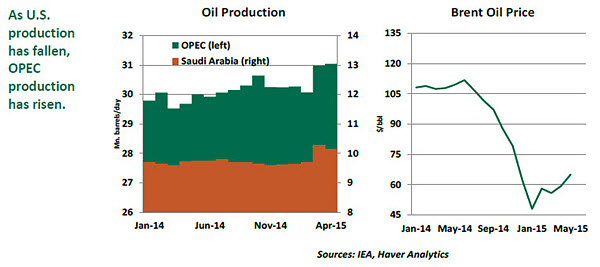

As crude oil prices rise, analysts have struggled to reconcile this with continuing increases in production from the Organization of Petroleum Exporting Countries (OPEC). April figures reported cartel countries producing more than 31 million barrels per day, including Saudi Arabia raising its own output to record highs. Yet with all this extra supply, markets are still firming.

Instincts suggest a supply question has a demand answer, but a rise in global oil consumption is not evident. The U.S. economy may be moving along just fine, but struggles in the eurozone, China and emerging markets suggest global oil consumption is soft at best.

The most likely reason for higher oil prices is reduced production in high-cost non-OPEC countries, with the U.S. standing out. The recent oil boom throughout the Midwest was extraordinarily profitable when oil exceeded $100/barrel, but the dramatic fall in prices has forced some operations to shut the valves and reconsider expansion of marginally profitable wells.

If so, it would be a win for OPEC’s mission to reclaim market share by forcing high-cost producers to shutter operations, but this will only be temporary. When price declines force production levels past an inflection point, oil prices recover; however, this restores profitability in some closed operations. Furthermore, producer cost-cutting lowers the per-barrel breakeven point, allowing more wells to restart. Renewed production then puts more supply on the market, prices fall, and the ball goes back into OPEC’s court.

The back-and-forth of the pricing cycle is a difficult race to handicap, leaving the markets to search for some sign of direction. Next month’s OPEC summit, on June 4, will likely reaffirm that the organization is committed to its ongoing strategy, and that it will produce as much oil as necessary to reclaim market share. And the next step will be up to the rest of the market.

Recommended Content

Editors’ Picks

AUD/USD: Gains appear capped near 0.6580

AUD/USD made a sharp U-turn on Tuesday, reversing six consecutive sessions of gains and tumbling to multi-day lows near 0.6480 on the back of the robust bounce in the Greenback.

EUR/USD looks depressed ahead of FOMC

EUR/USD followed the sour mood prevailing in the broader risk complex and plummeted to multi-session lows in the vicinity of 1.0670 in response to the data-driven rebound in the US Dollar prior to the Fed’s interest rate decision.

Gold stable below $2,300 despite mounting fears

Gold stays under selling pressure and confronts the $2,300 region on Tuesday against the backdrop of the resumption of the bullish trend in the Greenback and the decent bounce in US yields prior to the interest rate decision by the Fed on Wednesday.

Bitcoin price tests $60K range as Coinbase advances toward instant, low-cost BTC transfers

BTC bulls need to hold here on the daily time frame, lest we see $52K range tested. Bitcoin (BTC) price slid lower on Tuesday during the opening hours of the New York session, dipping its toes into a crucial chart area.

Federal Reserve meeting preview: The stock market expects the worst

US stocks are a sea of red on Tuesday as a mixture of fundamental data and jitters ahead of the Fed meeting knock risk sentiment. The economic backdrop to this meeting is not ideal for stock market bulls.