Week ahead: BoE and UK GDP in the spotlight

Following Friday’s huge miss in US jobs data – which triggered dollar selling, a bid in equities and bonds, and a sizeable dovish repricing in rates (markets are now implying 53bps of easing this year for the Fed funds target rate, with September fully priced in for a 25bp cut as opposed to November’s meeting prior to the release of the data) – the first full week of May is now upon us.

The calendar is lighter stateside this week, but we still have enough market-moving event risk to get our teeth into. The update from the Bank of England (BoE) and the UK GDP growth release will be the key macro highlights of the week, closely shadowed by US consumer sentiment numbers (preliminary release produced by the University of Michigan) and a look at the Canadian jobs market.

BoE rate change unlikely

The majority of the market and economists do not expect the BoE to budge on rates this week, scheduled to take the stage on Thursday at 11:00 am GMT. You may recall that from the March meeting, the MPC voted by a majority 8-1 to keep rates unchanged, observing two members (Jonathan Haskel and Catherine Mann) downshift their votes to hike the Bank Rate in favour of a hold and Swati Dhingra continued to vote for a 25bp cut. It was noted at the time of the release that this is a central bank manoeuvring towards policy easing and could prove a notable headwind for sterling (GBP).

Heading into this week’s meeting, it is obviously no secret we still have divided ranks among policymakers at the BoE. However, recent comments from BoE Governor Andrew Bailey and Deputy Governor David Ramsden aired a dovish vibe, expressing confidence in the disinflation process and that inflation risks remain ‘skewed to the downside’. So, with a potential change in votes in the not-so-distant future from these two key players and MPC member Dhingra likely to continue to vote for a cut, the gap between holding policy at current rates and a majority vote to cut is closing in. The March UK CPI revealed a slower-than-expected pace of disinflation across all four key metrics, though year-on-year measures continued to exhibit a disinflationary trajectory. This followed mixed labour data; the unemployment rate jumped to 4.2% in the three months to February from the upwardly revised 4.0% in the three months to January 2024, and wage growth was stronger than expected. The above, coupled with economic growth remaining weak, may pave the way for the central bank to begin pencilling in a timeline for easing.

Although a rate cut is pretty much off the table this week, traders will look to (and respond to) the rate statement, the updated economic forecasts, and the press conference for insight into when easing could commence, along with the BoE’s outlook on inflation and whether the central bank is waiting for the Fed to make its move before committing.

UK to exit technical recession?

Friday welcomes UK growth data ahead of the European cash open on Friday at 6:00 am GMT; market consensus heading into the data expects we’ll see another expansion in March. This follows economic expansion in January and February’s reports: +0.3% and +0.1%, respectively. This optimistic start to the year has also likely pulled the UK economy out of what was a mild ‘technical recession’ that kicked off in the second half of last year.

According to Bloomberg’s estimates, the median forecast indicates a +0.1% expansion in March (estimate range between +0.2% and -0.2%), with the QoQ release forecast to print +0.4% for Q1 (estimate range between +0.4% and +0.1%).

While an upside print (particularly one that is within close proximity of upper estimates) might drive GBP demand, and vice versa for a downside release, we have to consider that the BoE’s focus is on price pressures: inflation and wage numbers.

Additional data:

The Reserve Bank of Australia (RBA) is up on Tuesday at 4:30 am GMT. Market pricing suggests another no-change for the central bank this week, with only a 3.0% chance of a rate cut priced in.

Canadian jobs data will hit the wires on Friday at 12:30 pm GMT.

Preliminary University of Michigan (UoM) consumer sentiment survey data will be released on Friday at 2:00 pm GMT.

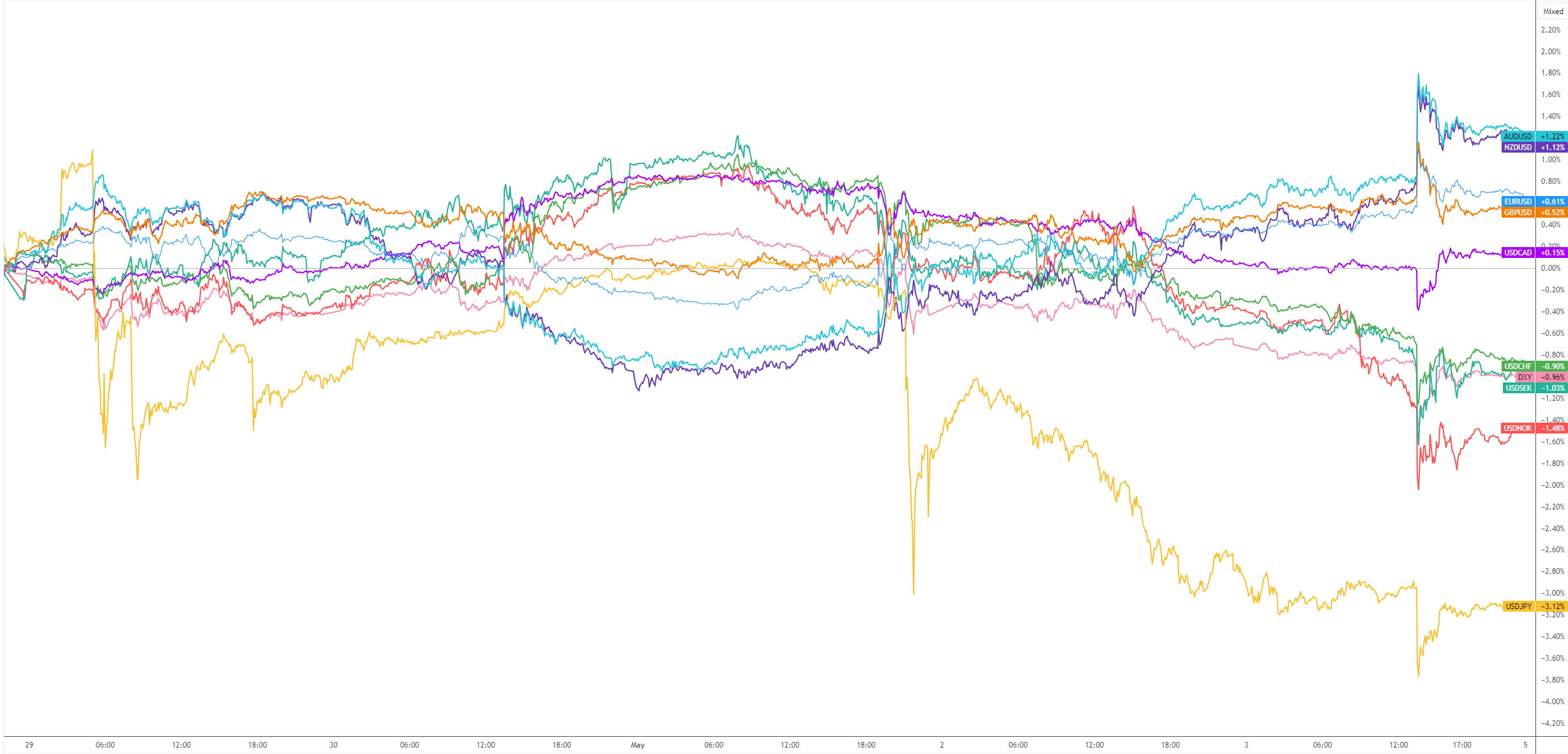

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,