US Retail Sales Preview: Holidays are unpredictable

- Retail sales predicted to be flat in December, the ex-autos component weaker

- The retail sales control group estimated to halve its November gain

- The holiday season’s sales report was delayed month by the partial government shutdown which ended on January 25th

Forecast

Retails sales are expected to rise 0.2% in December as they did the prior month. Sales excluding automobiles should fall to 0.1% after November's 0.2% increase. The 'control group’, which leaves out building materials, motor vehicles, gasoline purchases and food service is predicted to rise 0.4% in December following November’s 0.9% climb. This figure is used as the personal consumption component of GDP by the Bureau of Economic Analysis to calculate gross domestic product. Fourth quarter annualized GDP will be issued on March 28th.

Coincident economic factors for retail sales

Although Decembers’ retail sales fit unremarkably into the overall pattern of American consumer spending they have a disproportionate impact on many firms bottom-line often determining profitability for the year.

Black Friday is a colloquial term referring to the Friday after the Thanksgiving as the start of the Christmas and holiday shopping season. Since 2005 it has been the busiest shopping day of the year with many stores opening early in the morning and offering steep discounts.

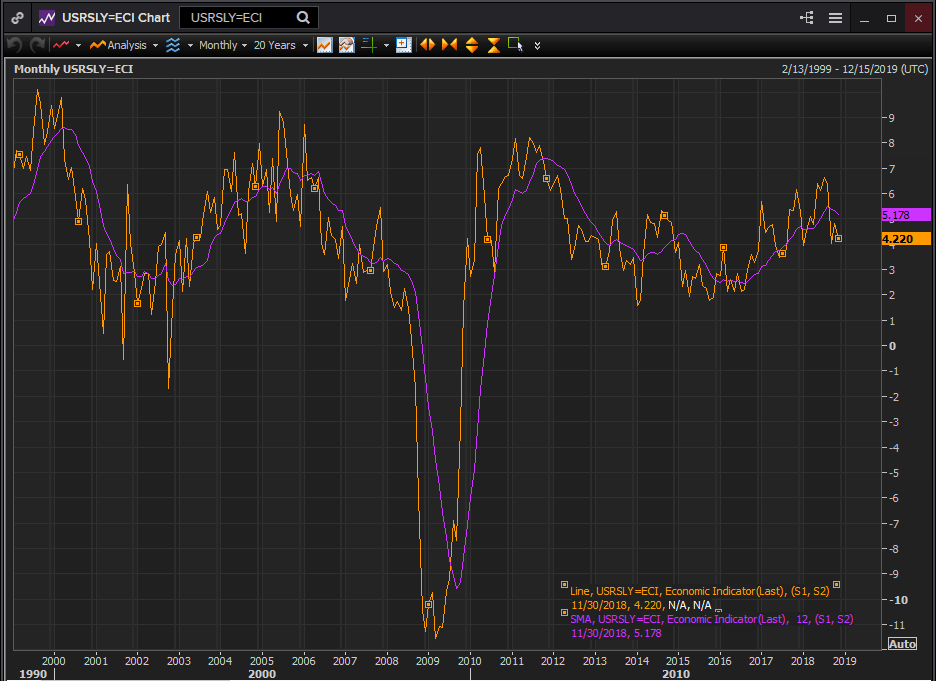

Annual retail sales have been rising at an increasing clip since the summer of 2016. In August of that year sales were 2.2% higher than the year before. By the election in November they were rising at a 3.27% pace. The 12-month moving average went from 2.52% in September 2016 to 4.20% a year later. It continued up to 5.49% this past August dropping to 5.18% in November.

Annual Retail Sales

Reuters

The quickening pace of annual sales has had little impact on the month to month sales figures which remain volatile.

Retail sales in November have been a poor predictor for December or January activity in the past five years.

In 2017 sales rose 0.8% in November followed by a flat December and a 0.1 decline in January. In 2016 it was almost the opposite, a flat November followed by 0.8% in December and 1.2% in January. In 2015 it was 0.3% in November, 0.4% in December and -0.7% in January. In 2014 0.2% in November then -0.6% in December and January. In 2013 0.3% in November was trailed by 0.5% in December and -1.0% in January.

Nor has the labor market been a reliable indicator. The 222,800 average for 2018 is the best yearly since 2015. In the five years prior to last year the economy produced a steady supply of jobs, averaging 182,000 per month in 2017, 195,000 in 2016, 226,000 in 2015, 250,000 in 2014, and 191,000 in 2013.

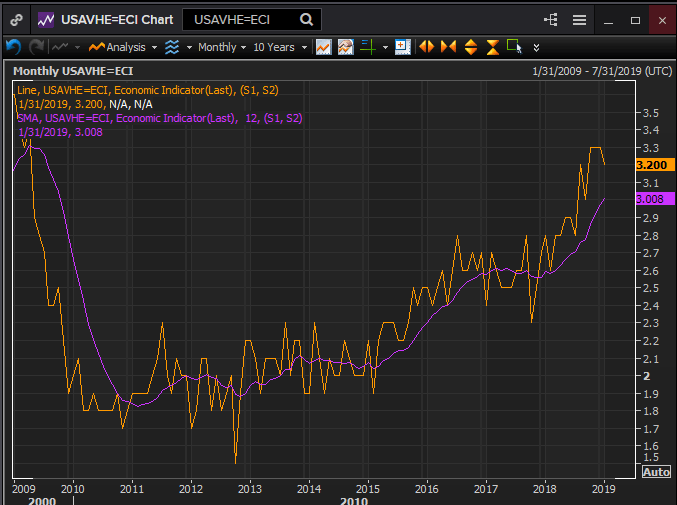

Annual wages gains have been on a steady increase in the last six years. Average annual hourly earlings averaged 2.98% last year, in 2017 they were 2.56%, in 2016 2.58%, in 2015 2.28%, 2014 2.05% and in 2013 2.09%.

Annual Average Hourly Earnings

Reuters

Unemployment has declined steadily from 8% in the beginning of 2013 to its current 4.0%. The 0.3% increase since October is a labor market success largely due to substantial numbers of people joining the work force not all of who immediately find work.

This increasing tempo of job creation, wage growth and improvement in unemployment in the last three years has not brought about reliably higher holiday sales in November, December and January though it has stoked a steady increase in annual retail sales.

Market Impact

With the Fed’s pullback on rate increases for 2019 there is concern that the global slowdown cited by the Chairman Powell could affect growth in the United States. Such possibility was one of the triggers behind the December equity meltdown. A healthy December sales number will help to aleviate that worry.

The United States economy expanded at a 3.27% annual rate in the first three quarters. The most recent Atlanta Fed GDPNow estimate for the fourth quarter is 2.7%. That would give the States a 12 month expansion of 3.125% and the best yearly growth since 2006. These retail sales figures for December are one of the last necessary components for the growth picture for 2018.

Holiday sales whether robust, mediocre or abysmal will not change the Fed’s mind on policy though strong spending will offer the dollar mild support. Any return to rate normalization would be unlikely to occur until the third quarter at the earliest and strong consumption growth in the interim would be only one of several economic trends that would be needed before the Fed will risk further hikes.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.