US Non-Farm Payrolls Preview: The trend remains the same

- October payrolls are expected to fall on General Motors strike.

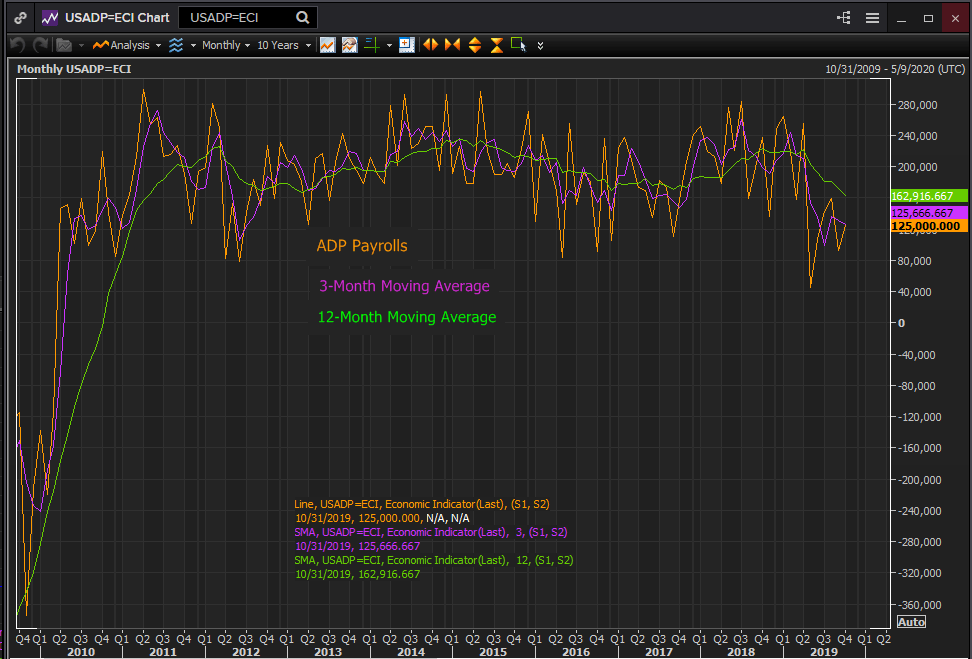

- ADP jobs of 125,000 in October were at the three month trend.

- Consumer economy and sentiment remain strong backed by labor market.

The Bureau of Labor Statistics (BLS) a division of the US Department of Labor will issue its Employment Situation Report for October on Friday November 1st at 12:30 GMT, 8:30 EDT.

Forecast

Non-farm payrolls are projected to add 85,000 in October after September’s 136,000 gain. The unemployment rate is expected to rise 0.1% to 3.6%. Average hourly earnings will climb 0.3% on the month and 3.0% on the year after no monthly gain in September and a 2.9% annual increase. The labor force participation rate will remain at 63.2%. Average weekly hours will be unchanged at 34.4%.

The Employment Situation Report

The US Labor Department’s Employment Situation Report is the most comprehensive assessment of the American labor market produced by the federal government. Commonly referred to as just payrolls or non-farm payrolls for its central jobs figure, it is the most widely followed and important US economic statistic.

The report consists of information gathered by two separate surveys. The establishment survey polls executives of non-farm businesses about various and detailed aspects of their businesses. It produces the payrolls numbers, wages, weekly hours, labor force participation rate and other statistics.

The household survey selects a representative sample of US households and asks if its members are part of the non-military working age population, if they are employed and if not when they last looked for work. The BLS computes its various unemployment rates from the answers.

The unemployment rate normally cited by economists and reported in the media is the U-3 rate. Inclusion as unemployed is limited to non-working individuals who have looked for a job in the month prior to the survey. Any individual who is not working but has not searched for work under the U-3 terms is not counted as part of the workforce.

A second unemployment rate, the U-6 or underemployment rate has a wider definition. It includes anyone who has looked for a job in the prior year. It is considered by many analysts a more accurate measure of joblessness.

The monthly payroll figures also incorporate an estimate for the number of new jobs created. The BLS utilizes its so-called birth–death model to project the new hires each month based on past labor market performance.

Once total payrolls have been reported to the government the estimated figures are revised against actual tax rolls in the annual baseline revision. Adjustment are often 500,000 a year or more.

Payroll data is one of the most up-to-date of government statistics as its data is about one month old.

Payrolls and the GDP

The gradual decline in payrolls this year has tracked the slippage in GDP and the plunge in business sentiment.

Economic growth has slowed from 3.1% in the first quarter to 2.0% in the second and 1.9% in the third.

Non-farm payrolls have dropped from 245,000 in the 3-month moving average in January to 157,000 in September. The descent has been measured though punctuated by two anomalous months, February and May with payroll totals far below trend.

Reuters

Private payrolls from ADP exhibit a similar if steeper pattern. They have decreased from 244,000 in the 3-month average in February to 126,000 in October.

Reuters

Some of the disparity can be laid to the cushioning effect of government hiring at all levels in the non-farm payroll numbers.

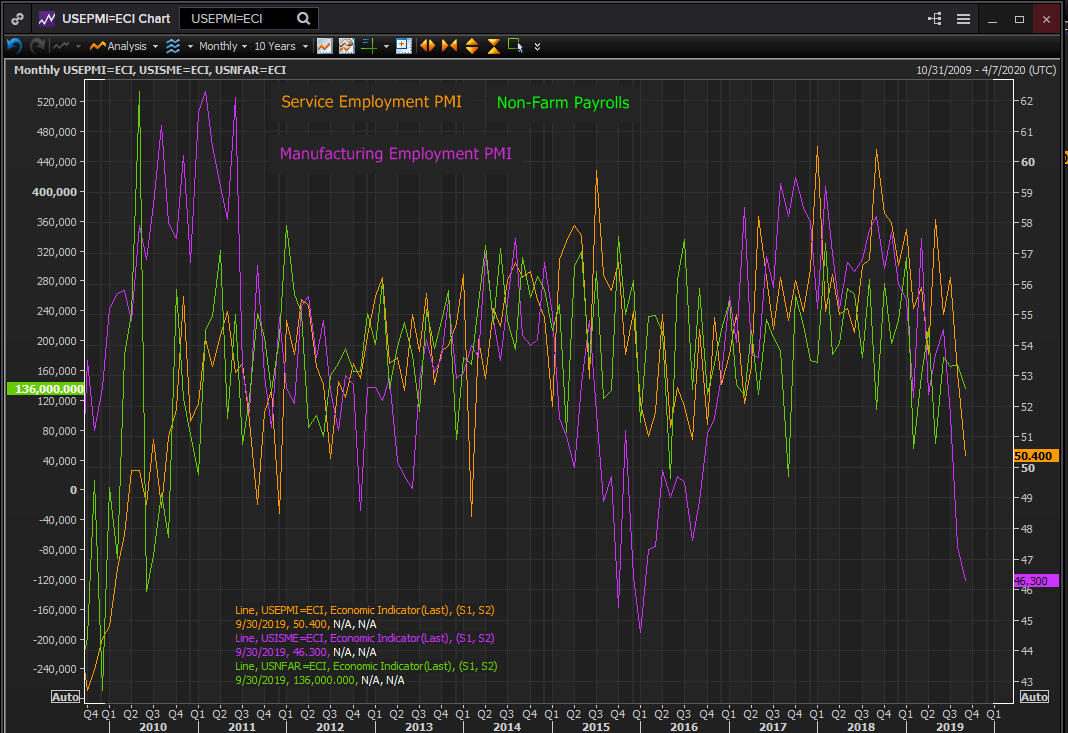

Purchasing managers indexes and payrolls

Business confidence has suffered a slow debilitation this year from the China trade dispute and the collapse in exports.

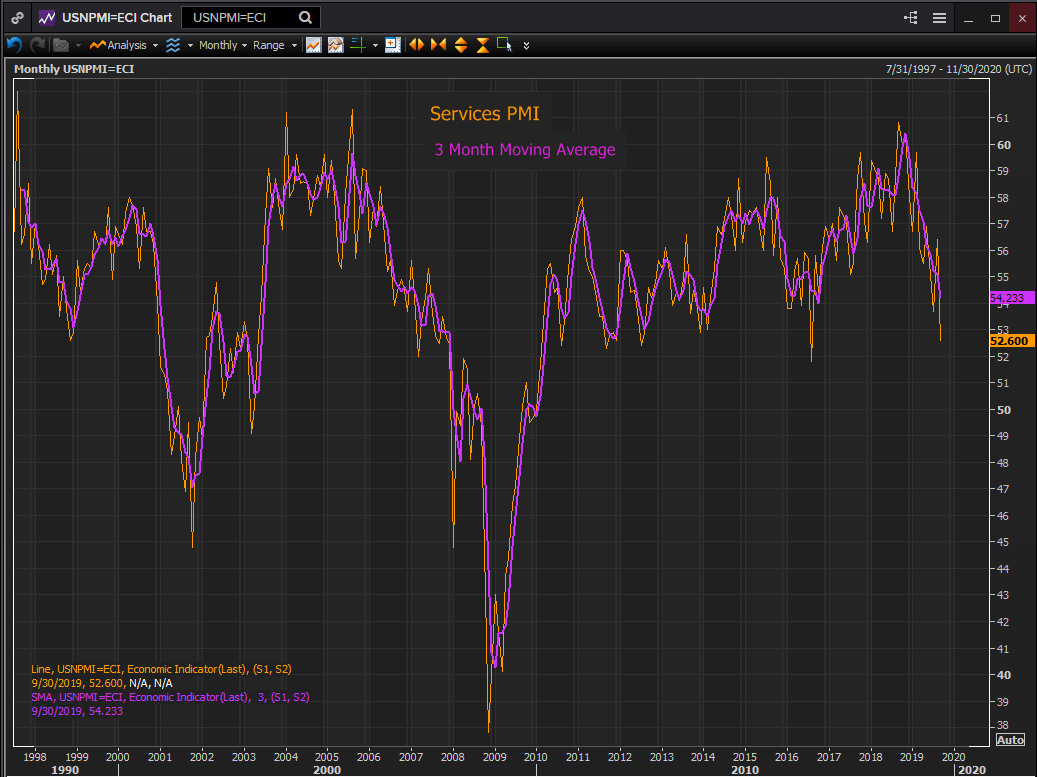

The purchasing managers’ index for the service sector has fallen from 59.7 in February to 52.6 in September. It is forecast to recover slightly to 53.2 when the October score is reported by the Institute for Supply Management on November 5th.

Reuters

The services employment index has seen an equally sharp and more rapid fall, descending from 58.1 in May to 50.4 just four months later in September.

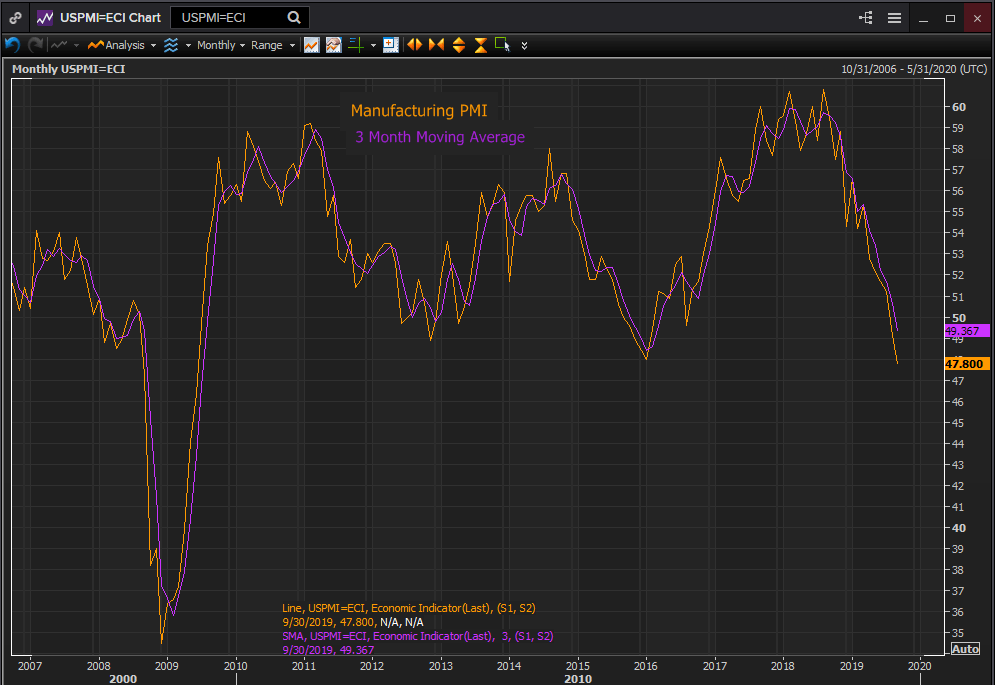

The PMI for manufacturing has descended from 56.6 in January to 49.1 in August and 47.8 in September. It is forecast to rise to 48.9 in October when released on November 1st. The overall drop from 60.8 in August 2018 is the steepest and longest since the collapse in the second half of 2008 leading into the financial crisis and recession.

Reuters

The manufacturing employment index has fallen from 57.3 in March of this year to 46.3 in September, the second month below the 50 expansion contraction demarcation.

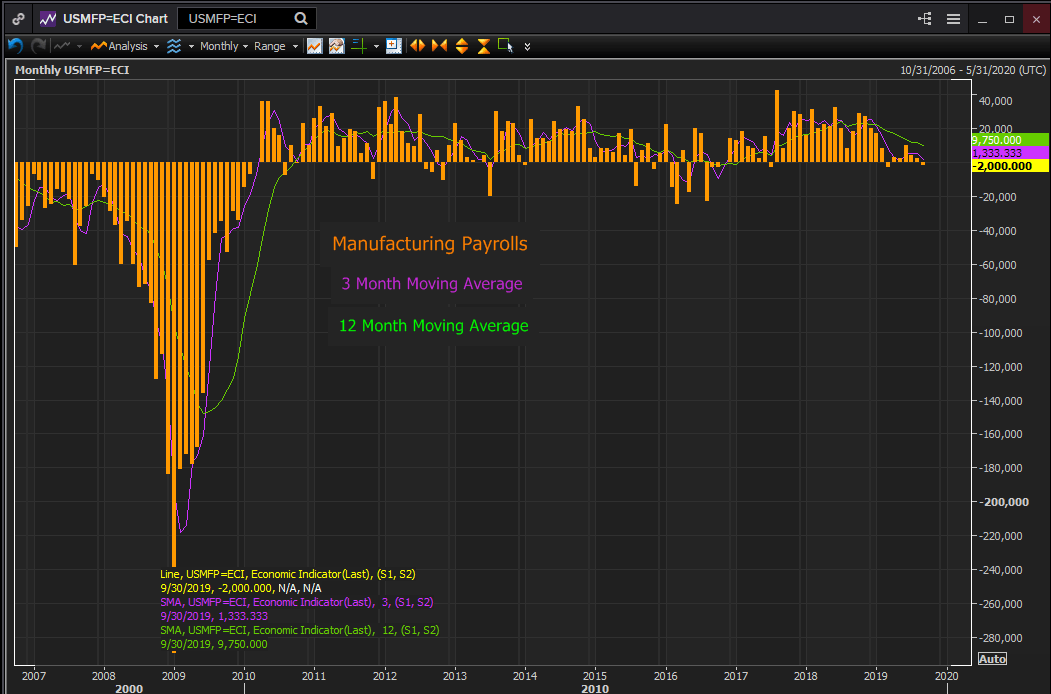

Manufacturing payrolls have fallen this year from 7,000 in the 3-month moving average in March to 1,000 in September.

Reuters

It should be noted that a prolonged period below 50 for the manufacturing employment index does not mean that employment in the general economy will follow factory work into contraction.

From August 2015 through September 2016 the manufacturing employment index was below 50 for 13 of 14 months but non-farm payrolls was barely affected. The monthly average for the entire 14 month period was 208,000.

Reuters

Manufacturing payrolls however declined from 3,000 a month in the three month moving average in July 2015 to -3,000 in September 2016. Employment for the entire 14 month period was just negative at -900 per month.

Employment and the overall economy

One of the surprising economic facts of the current record breaking expansion is that the near depression in business sentiment has had a limited effect on hiring. Most of the reason must go to the robust consumer economy.

Retails sales have been healthy. Consumer sentiment while lower than its record at the end of last year remains strong. Unemployment and initial jobless claims have been at half-century lows for more than a year. Households have seen the best gains in disposable income in a decade.

The 70% of the economy that depends on consumption and the approximately 85% tied to the service sector are flourishing. Household spending decisions are informed by the still excellent labor market which in turn has spread income into hitherto unemployed corners of the economy.

Conclusion

The October non-farm payrolls will be reduced by the impact of the General Motors strike during the payroll count. According to the Labor Department 46,000 General Motors workers were on the picket lines at the firm’s Michigan and Kentucky plants. Unpaid striking workers are counted as unemployed, subtracting from the payroll totals.

The total impact of the GM strike on payrolls could be as high as 75,000 or 80,000 when laid off workers in related industries are included.

If these figures are accurate the unaffected payrolls of around 160,000 would be almost exactly at the 157,000 three month moving average. There is little in the economy that would indicate anything else.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.