US Michigan Consumer Sentiment Preview: Who's got trouble?

- Consensus estimate is for limited recovery after August’s large fall

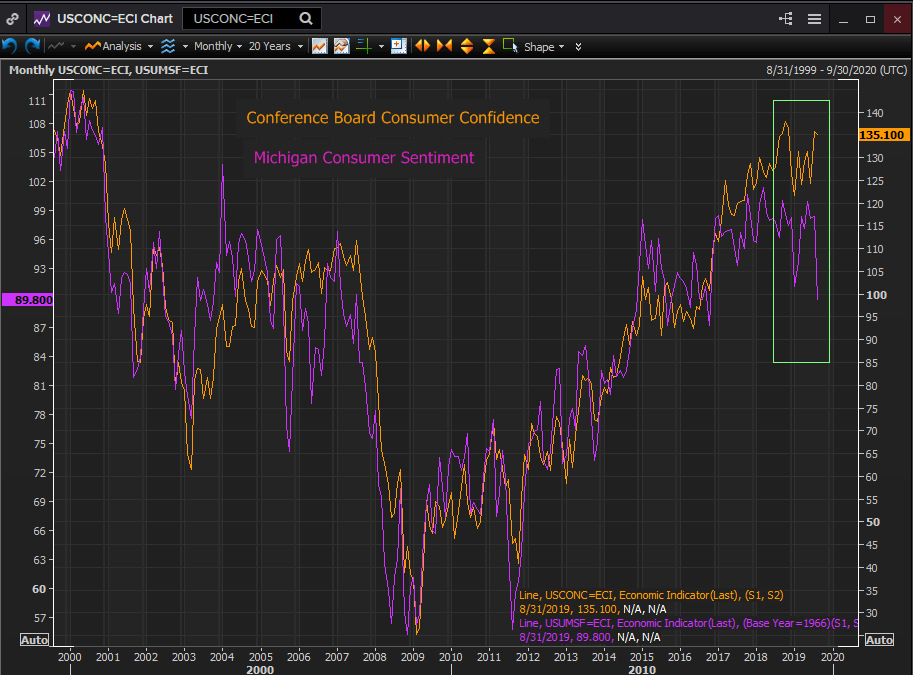

- Michigan Survey at odds with the Conference Board number

- Labor market backs strong consumption

The University of Michigan will issue its preliminary Survey of Consumers for September on Friday September 13th at 14:00 GMT, 10:00 EDT.

The survey consists of three indexes--the Index of Consumer Sentiment, the Index of Current Economic Conditions and the Index of Consumer Expectations. Each result is revised once. The survey began in 1978.

Forecast

The Consumer Sentiment Index is expected to rise to 90.9 in September from 89.9. The Current Conditions Index is projected to climb to 107.0 in September from 105.3. The Expectations Index is forecast to increase to 82.0 from 79.9.

Michigan Survey and the Conference Board

Reuters

The 8.6 point August decline in the Michigan Sentiment Index to 89.8 from July’s 98.4 was the largest one month drop in the index in six years. The prior record was the 9.8 point slide from November to December 2012.

The Conference Board Consumer Confidence Index for the same month, August, shows a minor decrease from 135.8 to 135.1.

Even though last month was not an outright divergence, both indexes fell from July to August, the scale of the difference and more importantly the resulting relative position was unusual.

For the Michigan Survey the index went from a July score at the upper end of the post-2016 election range to the absolute low of that range. By its assessment American consumers are as unhappy as any time since October 2016.

This is true despite the best job market in decades, the lowest unemployment rate in 50 years and the best wage increases since the recession. It does not seem a likely mix.

The Conference Board score for August places it as the fifth highest in the same two year range. This seems more compatible with the objective economic criteria.

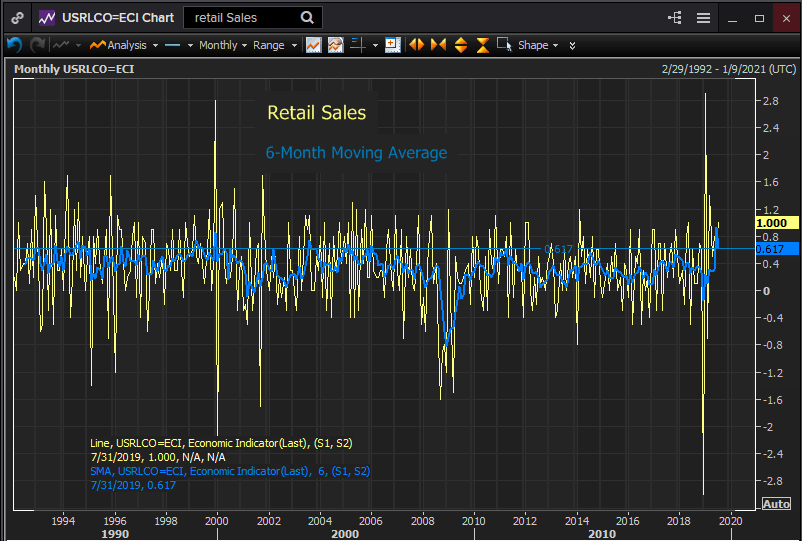

Retail Sales

Retail sales since January give additional evidence that consumer attitudes have not collapsed.

Starting in February, which avoids the two month reporting volatility in December -3.0% and January 2.9%, caused by the partial government shutdown, sales have averaged a 0.617% gain each month. That is the second best half year average in 14 years.

The June six month average of 0.933%, which is the highest, is tainted by including the January score of 2.9% without including the December figure of -3.0%. The 12-month moving average of 0.425% is the highest since May 2018.

Reuters

Conclusion

The objective facts of the labor market, job creation, the unemployment rate, wages and labor force participation rate are not normally associated, absent external events like the January government shutdown, with a precipitous drop in consumer sentiment. The notion is backed up by the Conference Board results and the evidence that consumers are spending at their highest rate in years.

Reuters

It may be that the Michigan survey registers discontent not assayed by other methods, or not. Friday will tell.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.