US Initial Jobless Claims Preview: Defining improvement

- Initial claims expected to fall to 1.550 million from 1.877 million.

- Continuing claims to drop to 20 million from 21.487 million.

- Total filed claims may rise to 44 million with continuing claims 20% from peak.

- Equity and currency markets are positioned for economic recovery.

- Federal Reserve issues its economic projections covering 2020, 2021 and 2022 on Wednesday.

Jobless claims continue their slow retreat from the March and April peak but despite improvement they remain in a different universe from the pre-pandemic US labor market that existed just four months ago.

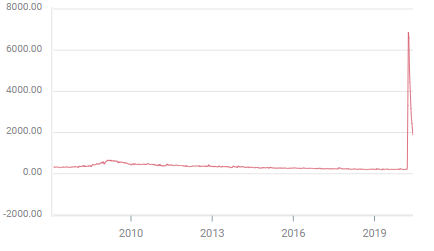

Labor market statistics

Initial claims are forecast to decline to 1.55 million in the June 5 week from 1.877 million in the last week of May. This would be a 78% drop from their high in the March 27 release of 6.867 million, but it is seven-fold increase over the claims four week average just two weeks before of 232,500.

Initial jobless claims

Continuing claims are predicted to drop to 20 million in the May 29 week from 21.487 the previous week. Here too that would represent a 20% improvement from the claims high of 24.912 million in the week of May 8 but it is an eleven-fold jump from the March 6 level of 1.702 million.

Non-farm payrolls and ADP for May second the improving job picture. Yet again the better statistics are in the context of the running debacle. Payrolls added 2.509 million positions in May far ahead of the forecast 8 million drop but that is barely 12% of the 20.687 million job eliminated in April.

The loss of 2.760 million employees from ADP’s private payrolls in April instead of the projected 9 million is to be welcomed, but it brings the two month total 22.317 million.

Purchasing managers’ indexes

Purchasing managers’ surveys from the Institute for Supply Management have come up from their April lows. Manufacturing PMI registered 43.1 up from 41.5. The new orders index rose to 31.8 from 27.1 and the employment index edged to 32.1 from 27.5.

Services showed greater improvement with the overall PMI rising to 45.4 in May from 41.8 and new orders jumping to 41.9 from 32.9. Employment inched to 31.8 from 30 in April.

Hiring decision are normally the slowest to accommodate, the last to fall as conditions deteriorate and the last to improve as the economy improves.

Conclusion: Market conditions

The decline in initial and continuing claims and the resumption of employment in May indicate that the reopening of the US economy, variable by state as it may be, is having a positive effect but there is a very long way to go. Without an acceleration of hiring it would take another seven months to fully replace the April payroll at the May hiring rate.

The assumption that all the business that existed prior to the shutdowns are waiting to resume is unsupportable. An unknown percentage will have folded already or be unable to sustain operations on the limited basis granted in many states. The riots in many US cities over the last two week will have destroyed a further number of mostly small businesses.

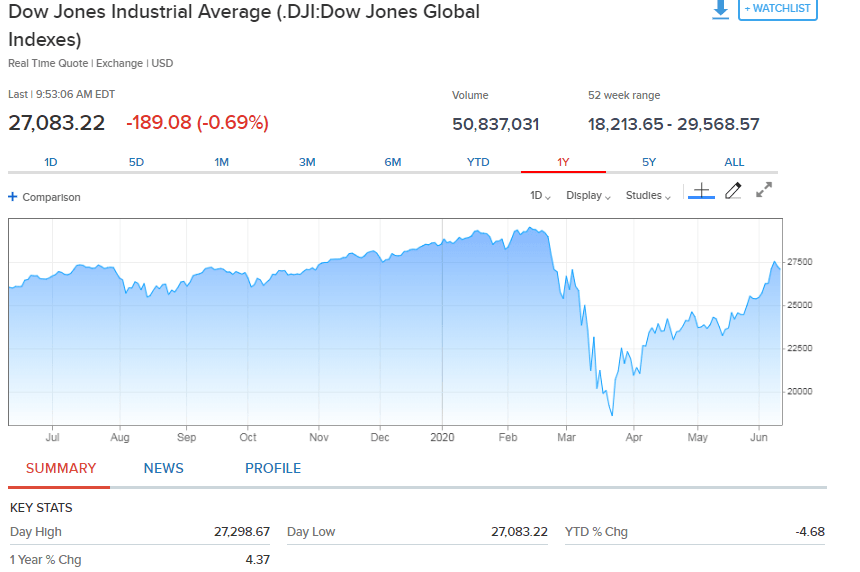

Markets have largely priced in a recovery. Equities are close to their levels of early March with the Dow down just 4.68% on the year and from its record and the S&P off just 0.73% in the same measures at the Tuesday close. The Nasdaq treaded over 10,000 for the first time ever on Tuesday.

Currencies have rescinded all of the US dollar’s risk-premium with the greenback weaker than late February levels in all major pairs except the sterling this week.

Only Treasury yields with prices supported by the Fed’s extensive purchase program are at half or less of their February returns.

Wednesday’s Federal Reserve meeting, slated to unveil the first economic projections for this year, is unlikely to stir any changes in the market assessment of recovery.

With regional Fed second quarter GDP estimates from Atlanta at -48.5% and New York at -25.3% and Fitch Rating at -10%, it will not be hard for the Fed to trace a moderate path to optimism on Wednesday afternoon.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.