US Federal Reserve Interest Rate Decision and Economic Projections: We know where we are and how we got here but where are we going?

- No changes expected in policies or programs from the FOMC.

- Projection materials for 2020 and beyond are of overriding market interest.

- Fed estimates due in March were skipped as the pandemic took hold.

- Chairman Powell’s press conference will be key to understanding Fed view.

- Dollar has stalled after surrendering risk-aversion gains.

After an extraordinary three months of policy initiatives the Fed will present its first statistical estimate of the pandemic induced economic collapse with its projections for GDP, inflation, interest rates and unemployment over the next three years.

No change is expected in either the central bank’s interest rate policy or its emergency quantitative easing and loan programs at the Wednesday Federal Reserve Open Market Committee (FOMC) meeting. The overriding market interest will be in its Projection Materials detailing the bank’s views on economic growth, prices and policy for the next three years.

The first quarterly projections for 2020 had been scheduled for the March 17-18 FOMC meeting that was superseded by the two emergency meeting on March 3 and March 15 and then cancelled.

Chairman Powell has said that the current policies will remain in place until the US has fully cleared the effects of the economic shutdown but the bank’s surmise for the economy this year and the next two will be of great interest to markets that have largely priced in a rapid economic recovery.

Fed policies and balance sheet

Since March 3 the Federal Reserve has cut the upper fed funds target from 1.75% to 0.25%, opened a $700 billion bond purchase program, instituted swap lines with central banks around the world to prevent a dollar shortage in the global financial system, begun unlimited quantitative easing and commenced a $2.3 billion loan provision for business and local governments.

Treasury rates have dropped as the Fed has forced bond prices higher. The yield on the 10-year Treasury has fallen by half from 1.61% in mid-February to 0.82% on June 8 and the 2-year has gone from 1.42% to 0.24%.

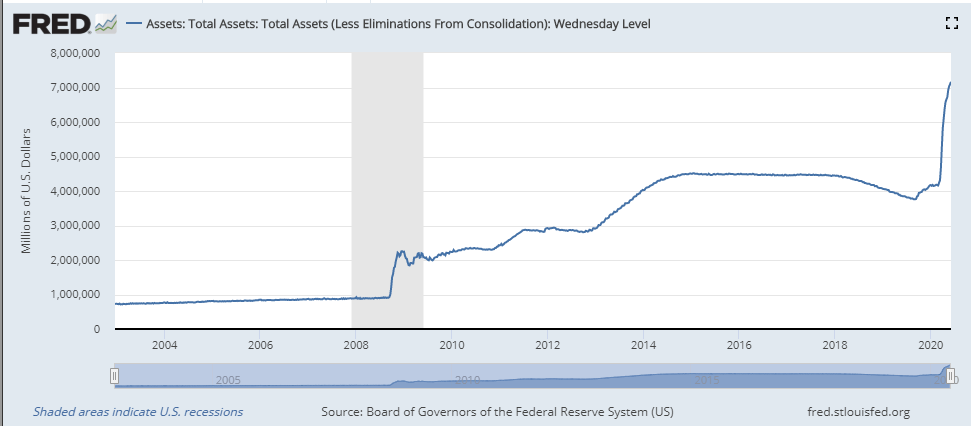

To force that decline in rates the Federal Reserve balance sheet of total assets has expanded 69% from $4.24 trillion on March 4 to $7.165 trillion on June 3. That $2.9 trillion addition is almost as much as the $3.6 trillion the central bank balance sheet grew in the six years of financial crisis purchases (September 2008 to January 2014)

GDP projection and markets

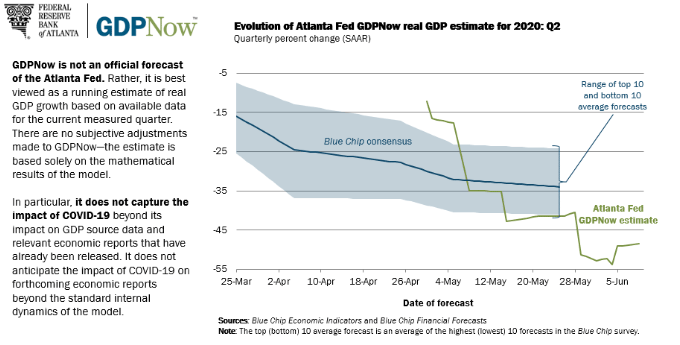

The latest Atlanta Fed GDPNow forecast (June 9) has US economic growth dropping 48.5% on an annualized basis in the second quarter after falling 5% in the first. The New York Fed's Nowcast for second quarter GDP was -25.5% and -12% for the third on June 5. Fitch Ratings, the US credit rating agency is projecting a 10% drop in the second quarter.

Bank officials have repeatedly stated that these projections should not be treated as forecasts but since they are the product of the governors themselves markets have generally ignored that caveat.

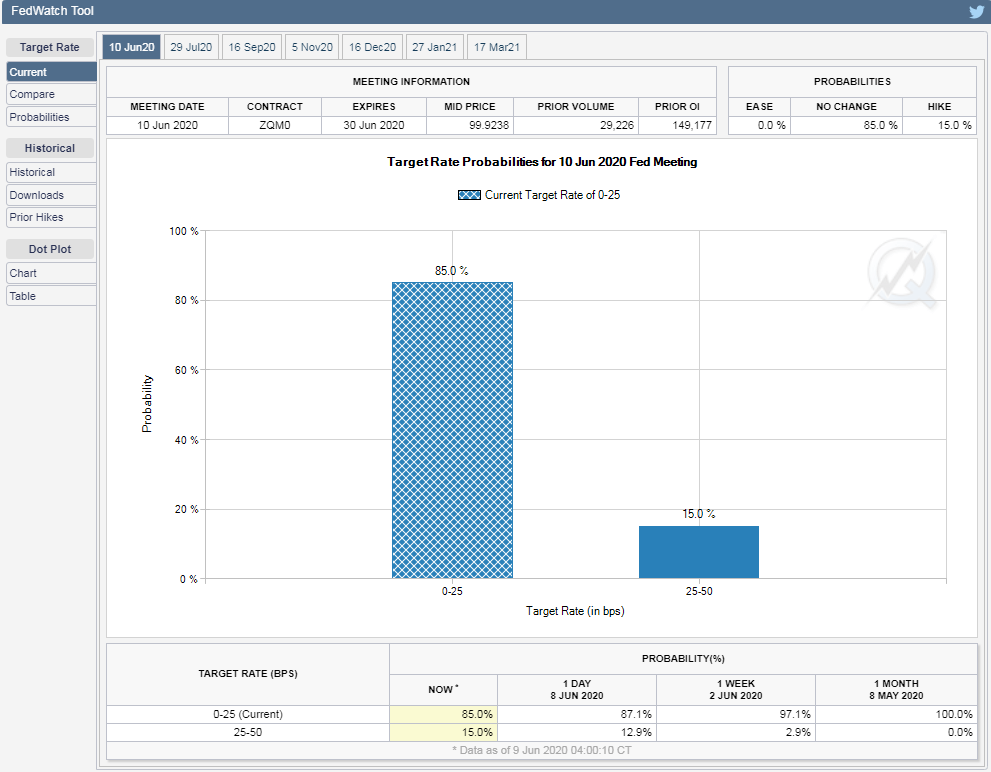

Fed futures offer a market based projection for the base rate. At the December 16, 2020 FOMC meeting the estimate for a 0%-0.25% fed funds rate is 87.4% and 12.6% for a 0.25%-0.50% rate. At the March 17, 2021 meeting, the farthest out the futures measure, the percentages are virtually unchanged at 88.2% and 11.8%.

Equity markets have recovered the bulk of their losses with Dow down 4.4% on the year at Tuesday’s close and S&P 500 essentially even at -0.73%. The Nasdaq set a 52 week high and is up 10.9% on the year.

Currency markets have revoked all of the US dollar’s pandemic risk aversion differential with all major pairs at or beyond their late February levels.

Only the Treasury market as noted above has retained its pandemic pricing and yields and these are supported by the Fed’s massive and continuing purchases.

Conclusion: Markets

The equity and currency markets have priced a rapid if not complete US economic recovery for which there is as yet only the tenuous statistical evidence of the May non-farm payrolls.

In comparison the ECB expects an 8%-12% contraction in the eurozone economy in 2020.

The end of the dollar panic trade has left currency markets without a clear direction.

Economic estimates from the American central bank tend to become the market reference and this month’s will be that and more. Chairman Powell will likely be cautiously upbeat in his assessment for the US economy but the grist will be in the economic projections. The Fed is unlikely to be overly pessimistic and when the novelty of the economic situation is combined with the wide range of current forecasts it should be relatively easy for the bank to be find a moderately optimistic outlook.

If the projections present a reasonably positive view for the balance of the year and next, equities and the dollar will immediately begin to price that future.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.