US Dollar Weekly Forecast: DXY driven by Fed policy expectations, FOMC Minutes in the docket

- The USD Index (DXY) bounced off multi-week lows near 104.00.

- Investors expect the Fed to start reducing rates in September.

- Fed speakers lean towards a cautious note regarding rate cuts.

- Fedspeak, FOMC Minutes, and flash PMIs are next on tap.

A dreadful week for the Greenback saw the USD Index (DXY) retreat to the area of five-week lows in the 104.00 neighbourhood, managing to regain some composure in the latter part of the week.

It was all about inflation

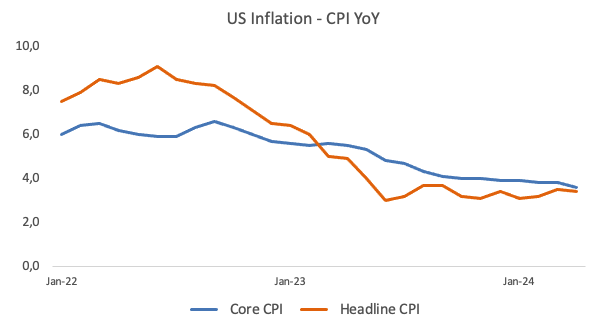

The weekly performance of the US Dollar (USD) was almost exclusively driven by the release of US inflation figures gauged by the Consumer Price Index (CPI) for the month of April, which confirmed once again the continuation of the disinflationary trend in the US economy.

Despite the positive surprise from the Producer Price Index (PPI) earlier in the week, investors seem to have accelerated their conviction of an interest rate cut by the Federal Reserve (Fed) in the next few months, with September being the most-likely candidate.

According to CME Group’s FedWatch Tool, the probability of a lower Fed Funds Target Range (FFTR) in that month hovers around 70%.

Prudent Fedspeak needs more conviction

Contrario sensu to what markets and investors seem to believe, most Fed officials showed a great deal of prudence when it came to the rising likelihood of the start of the Fed’s easing cycle.

That said, Federal Reserve Vice-Chair Phillip Jefferson (permanent voter) argued on Monday that, in an otherwise healthy economy, the central bank should maintain its current monetary policy until it is evident that inflation is moderating back to the 2% target. Federal Reserve Chair Jerome Powell also indicated that he expects inflation to continue declining through 2024, as it did last year, though his confidence has waned after prices rose faster than expected in the first quarter. Later on, Minneapolis Federal Reserve Bank President Neel Kashkari (non-voter) reiterated his uncertainty about how restrictive monetary policy is currently, suggesting that borrowing costs "probably need to sit here for a while" as central bankers evaluate inflation. Finally, Federal Reserve Bank of New York President John Williams (permanent voter) welcomed the recent softer consumer inflation data but said this positive development is not sufficient to justify cutting interest rates soon, while Federal Reserve Bank of Cleveland President Loretta Mester (voter) stated that maintaining the current policy levels will help bring the still-high inflation back to the 2% target.

US yields appear inclined towards lower rates

In the US money markets, the recent performance of the Dollar coincided with a resurgence of the downward bias in US yields across different timeframes. This occurred against an unchanged macroeconomic backdrop, suggesting the potential for only one or no rate cuts for the rest of the year by the Fed.

Looking at the broader interest rate trajectories among G10 central banks and inflation dynamics, the European Central Bank (ECB) is anticipated to cut rates during the boreal summer, possibly followed by the Bank of England (BoE). However, the Federal Reserve and the Reserve Bank of Australia (RBA) are expected to start easing later in the year, possibly in the fourth quarter.

In the upcoming week, the key event will be the release of the FOMC Minutes as well as preliminary readings of Manufacturing and Services PMIs for the month of May, all amidst further comments from Fed rate-setters.

Technical Analysis of USD Index (DXY)

Increased downward pressure could prompt the USD Index (DXY) to revisit the May low of 104.08 (May 16), a region propped up by the interim 100-day SMA. Further south comes the weekly low of 103.88 (April 9), ahead of the March bottom at 102.35 (March 8). A deeper retracement might lead the index to test the December low at 100.61 (December 28), ahead of the psychological barrier at 100.00 and the 2023 bottom at 99.57 (July 14).

Conversely, a bullish move could prompt a retest of the 2024 peak at 106.51 (April 16). Surpassing this level might encourage a move towards the November high at 107.11 (November 1), just before the 2023 top at 107.34 (October 3).

From a broader perspective, the prevailing bullish bias is expected to persist as long as DXY remains above the 200-day SMA.

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.01% | -0.24% | 0.06% | -0.09% | -0.10% | -0.15% | 0.19% | |

| EUR | 0.01% | -0.23% | 0.08% | -0.07% | -0.07% | -0.12% | 0.22% | |

| GBP | 0.24% | 0.23% | 0.32% | 0.17% | 0.19% | 0.10% | 0.44% | |

| JPY | -0.06% | -0.08% | -0.32% | -0.17% | -0.16% | -0.23% | 0.13% | |

| CAD | 0.09% | 0.07% | -0.17% | 0.17% | -0.00% | -0.05% | 0.29% | |

| AUD | 0.10% | 0.07% | -0.19% | 0.16% | 0.00% | -0.05% | 0.29% | |

| NZD | 0.15% | 0.12% | -0.10% | 0.23% | 0.05% | 0.05% | 0.35% | |

| CHF | -0.19% | -0.22% | -0.44% | -0.13% | -0.29% | -0.29% | -0.35% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Economic Indicator

FOMC Minutes

FOMC stands for The Federal Open Market Committee that organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

Read more.Next release: Wed May 22, 2024 18:00

Frequency: Irregular

Consensus: -

Previous: -

Source: Federal Reserve

Minutes of the Federal Open Market Committee (FOMC) is usually published three weeks after the day of the policy decision. Investors look for clues regarding the policy outlook in this publication alongside the vote split. A bullish tone is likely to provide a boost to the greenback while a dovish stance is seen as USD-negative. It needs to be noted that the market reaction to FOMC Minutes could be delayed as news outlets don’t have access to the publication before the release, unlike the FOMC’s Policy Statement.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.