US Dollar Weekly Forecast: All point to a 25 bps rate cut by the Fed

- US Dollar Index drops for second consecutive week.

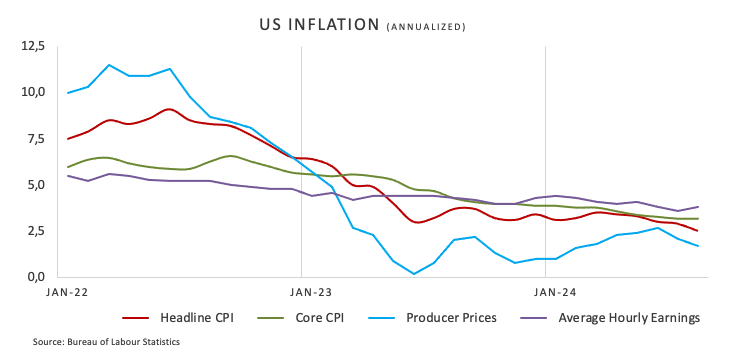

- US disinflationary trends remained well in place in August.

- Fed is largely anticipated to cut rates by 25 bps next week.

The pessimism around the US Dollar (USD) intensified in the latter part of the week, sending the US Dollar Index (DXY) back into negative territory for the second consecutive time on the weekly chart.

A glimpse at the DXY’s price action so far in September signals quite a decent resistance zone just below the 102.00 barrier, although the broader bearish outlook is expected to remain unchanged while below the critical 200-day SMA at 103.85.

The weekly decline was mainly driven by investors’ adjustments to the most likely 25 basis points (bps) cut to the Federal Reserve’s (Fed) Fed Funds Target Range (FFTR) at its meeting on September 18.

In the meantime, concerns over a potential “hard landing” of the US economy seem to have dissipated for the time being.

The decision is made: It will be a 25 bps rate cut

Despite the commencement of the Fed’s easing cycle never being under scrutiny, the size of the first interest rate cut has been under persistent debate over the last few weeks.

Until last Wednesday, in fact, following the publication of mixed Nonfarm Payrolls for the month of August on September 6, investors’ attention shifted to inflation. On this, the release of the US inflation data measured by the Consumer Price Index (CPI) on Wednesday showed further confirmation that the disinflationary pressures remained well and sound in August.

Still around inflation, a report released on Monday by the New York Federal Reserve indicated that the US public's expectations for inflationary pressures remained largely unchanged last month, even as current price pressures continued to ease. The New York Fed's latest Survey of Consumer Expectations showed that, in August, respondents anticipated inflation to be at 3% one year from now and 2.8% five years from now, consistent with the levels reported in July. The survey also revealed that respondents expected inflation to be 2.5% three years ahead, up from 2.3% in July.

In fact, and despite a small uptick in the Greenback soon after the CPI release, market participants have started to unwind their Dollar’s positions, putting the DXY under increasing pressure and motivating it to once again break below the key 101.00 support towards the end of the week.

It is worth recalling that Fed Chair Jerome Powell opened the door to rate cuts in his speech at the Jackson Hole Symposium in late August, a view that was subsequently reinforced by other Fed policymakers: Atlanta Federal Reserve President Raphael Bostic warned that high interest rates could harm employment. San Francisco Fed President Mary Daly suggested cutting interest rates to maintain a healthy labour market, but the extent of the cuts would depend on upcoming economic data. Federal Reserve Bank of New York President John Williams suggested a more balanced economy created the possibility for rate cuts, with the exact course of action depending on future economic performance. Finally, Fed Governor Christopher Waller and Chicago Fed President Austan Goolsbee advocated for multiple interest rate cuts to support full employment and align wage growth with the 2% inflation target.

According to the CME Group's FedWatch Tool, there is around a 57% chance of a quarter-point rate cut in September, while the likelihood of a 50-basis-point cut stands at about 43%.

After the anticipated rate cut in September, market participants are expected to shift their focus to evaluating the performance of the US economy to better predict any future rate cuts.

Currently, investors have priced in around 250 basis points of easing over the next twelve months. While earlier concerns about a recession seem to have lessened, upcoming economic data could still influence the Fed's monetary policy decisions.

Outlook on international monetary policy: What’s next?

The Eurozone, Japan, Switzerland, and the United Kingdom are all facing increasing deflationary pressure. In response, the European Central Bank (ECB) implemented its second interest rate cut on Thursday and maintained a cautious stance regarding any potential move in October. While ECB policymakers remain uncertain about additional rate cuts, markets are already pricing in two more reductions later this year.

Similarly, the Swiss National Bank (SNB) surprised markets with a 25-basis-point cut on June 20, and the Bank of England (BoE) followed with a quarter-point cut on August 1. Meanwhile, the Reserve Bank of Australia (RBA) took a different approach by keeping rates unchanged at its August 6 meeting, while sticking to a hawkish narrative in subsequent comments. Market expectations suggest the RBA could start easing rates sometime in Q4 2024.

In contrast, the Bank of Japan (BoJ) took markets by surprise on July 31 with a hawkish move, raising rates by 15 basis points to 0.25%. Despite the recent hawkish tone from some BoJ officials, money markets see only 25 bps of tightening by the central bank in the next 12 months. At its gathering next Friday, the central bank is expected to keep rates unchanged.

When politics meets economics

Since the latest US presidential debate, the Democratic Party's presidential candidate and US Vice- President, Kamala Harris, appears to be leading the run-up to the upcoming US election on November 5 by a slight margin vs. Republican candidate and former US President Donald Trump. It is important to consider that a second Trump administration, along with the possible reinstatement of tariffs, could disrupt or even reverse the current disinflationary trend in the US economy, potentially leading to a shorter period of Fed rate cuts. Conversely, some analysts argue that a Harris victory might result in higher taxes and increased pressure on the Fed to ease monetary policy if economic growth begins to slow.

What’s up next week?

The Fed meeting will be the key event to watch next week. Meanwhile, the release of Retail Sales data for August on Tuesday will also play an important role by providing further insights into consumer spending trends. Additionally, data on Industrial Production, the Philly Fed Index, and the usual weekly jobless claims will offer more clues on the overall health of the US economy.

Techs on the US Dollar Index

The chances of continued downward pressure on the US Dollar Index (DXY) have risen after it broke decisively below the important 200-day Simple Moving Average (SMA), currently positioned at 103.85.

If the bearish momentum continues, the DXY could first target the 2024 low of 100.51, recorded on August 27, and then the psychologically important 100.00 level. Further south emerges the 2023 bottom of 99.57, seen on July 14.

Bullish attempts should meet immediate resistance at the September top of 101.95, seen on September 3, prior to the weekly peak of 103.54 from August 8 and the critical 200-day SMA.

The day-to-day Relative Strength Index (RSI) has returned to the sub-40 region, accompanying the bearish price action in the index.

Economic Indicator

Fed Interest Rate Decision

The Federal Reserve (Fed) deliberates on monetary policy and makes a decision on interest rates at eight pre-scheduled meetings per year. It has two mandates: to keep inflation at 2%, and to maintain full employment. Its main tool for achieving this is by setting interest rates – both at which it lends to banks and banks lend to each other. If it decides to hike rates, the US Dollar (USD) tends to strengthen as it attracts more foreign capital inflows. If it cuts rates, it tends to weaken the USD as capital drains out to countries offering higher returns. If rates are left unchanged, attention turns to the tone of the Federal Open Market Committee (FOMC) statement, and whether it is hawkish (expectant of higher future interest rates), or dovish (expectant of lower future rates).

Read more.Next release: Wed Sep 18, 2024 18:00

Frequency: Irregular

Consensus: 5.25%

Previous: 5.5%

Source: Federal Reserve

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the New Zealand Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.06% | -0.04% | -0.75% | 0.07% | 0.22% | 0.24% | -0.38% | |

| EUR | 0.06% | 0.00% | -0.67% | 0.12% | 0.29% | 0.37% | -0.31% | |

| GBP | 0.04% | -0.01% | -0.67% | 0.09% | 0.27% | 0.37% | -0.32% | |

| JPY | 0.75% | 0.67% | 0.67% | 0.82% | 0.96% | 1.05% | 0.38% | |

| CAD | -0.07% | -0.12% | -0.09% | -0.82% | 0.13% | 0.27% | -0.44% | |

| AUD | -0.22% | -0.29% | -0.27% | -0.96% | -0.13% | 0.11% | -0.59% | |

| NZD | -0.24% | -0.37% | -0.37% | -1.05% | -0.27% | -0.11% | -0.70% | |

| CHF | 0.38% | 0.31% | 0.32% | -0.38% | 0.44% | 0.59% | 0.70% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.