US CPI Preview: Rhetoric aside who’s watching CPI?

- Headline inflation expected to rise slightly, core stable

- Inflation third on Fed list behind growth, trade

- CPI result will not sway Fed policy

The Bureau of Labor Statistics, (BLS) will issue its consumer price index for July on Tuesday August 13th at 12:30 GMT, 8:30 EDT.

Forecast

The consumer price index is expected to gain 0.3% in July after June’s 0.1% increase. Annual inflation will edge to 1.7% from 1.6% in June. Core CPI is forecast to slip to 0.2% in July from 0.3% in June. Core annual inflation is forecast to be unchanged at 2.1%.

Federal Reserve policy and inflation

When the FOMC lowered the fed funds rate for the first time in over a decade on July 31st inflation was not the first, or even the second thing on the governors’ minds. Chairman Powell made the order of preference quite clear: the US economic expansion, trade tensions with China, the global slowdown and then inflation, or inflation expectations. That doesn’t mean that higher inflation ‘symmetric around 2%’ as the Fed likes to say, wouldn’t be welcomed and that lower interest rates wouldn't be the traditional policy application.

This order of concern is not new. For most of the three year period from December 2015 until December 2018 as the FOMC was bringing the fed funds rate from 0.25% up to 2.5% inflation was below the 2% goal.

Reuters

Then as now the Fed had a more important goal. Under Janet Yellen the Fed was determined to normalize interest rates at the fastest pace the economy could bear. The bank was successful. The Fed’s 2.5% achievement can only be envied by the industrial world’s other central banks who are now facing the same economic circumstances with far less in the way of available interest rate stimulus.

Federal Reserve Mandates

Mr. Powell’s primary goal and we assume of the FOMC as a whole is to keep the US expansion, currently the longest on record, running and delivering employment and wage gains to the far reaches of the economy. That is a goal wholly commensurate with the Fed’s ‘maximum employment’ Congressional mandate.

The Fed’s second mandate, ‘price stability’ was formulated in an era where rampant inflation was the chief economic threat. The success of central banks around the world in controlling debilitating inflation has made the price based mandate much less important.

It is one thing to bring uncontrolled consumer price inflation from 12%, where it is a severe danger to growth, employment and the reasonable functioning of an economy, down to 2% as the Fed has accomplished. It is another to push price changes 0.5% higher to meet a somewhat arbitrary 2% target. The first is basic first order economics; the second is minor technical adjustment.

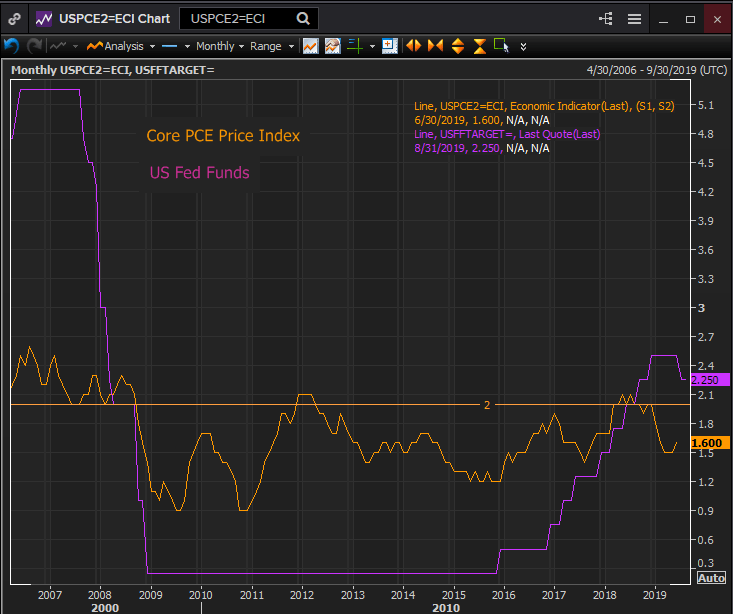

CPI and PCE

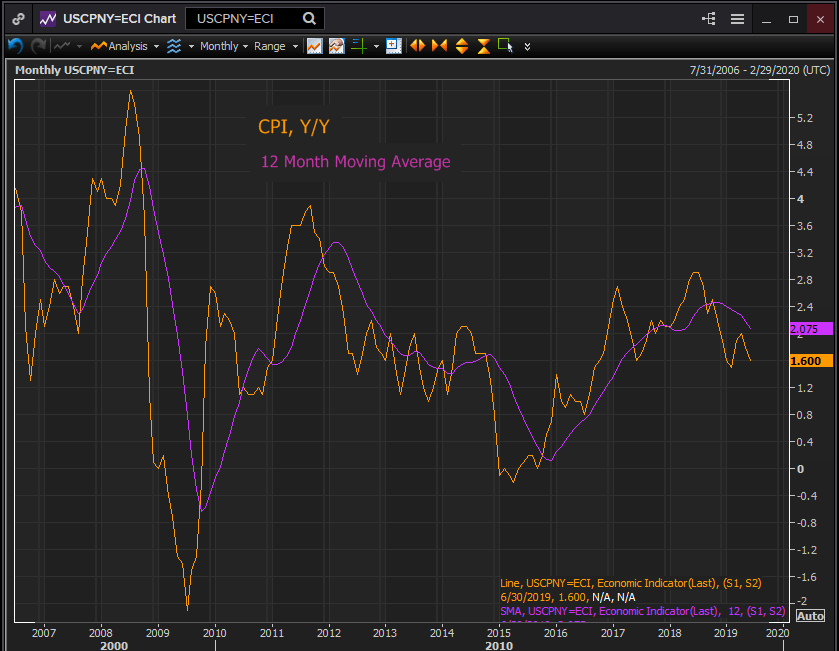

The consumer price index has averaged 2.075% in the 12 months to June. The core rate averaged 2.15%. Both have been falling since peaking last July. The overall rate from 2.9% in July 2018, and the core rate from 2.4% that same month.

These declines are the same at a differential as the core PCE price index which has fallen from 2.1% last July to 1.6% in June.

Fed Inflation Policy

The consumer price index and the Fed’s preferred measure the core PCE index have become secondary concerns for the bank’s governors as they oversee the US economy.

Inflation has ceased to be the threat that it was in the heroic days of Paul Volker and Ronald Reagan. Whether the core PCE price index is at 1.6% or 2% or 2.2%, the impact of prices and the difference between those rates on the economy is close to nil.

If CPI and by implication PCE are lower than anticipated that offers mild reinforcement for the Fed’s July cut and perhaps future reductions. If they are higher that is pleasant, but unimportant.

Either way the Fed has not tied its rate policy to inflation. Sustaining the US expansion, mitigating as best it can the trade and global threats to growth and the American labor market are the governors’ priorities and the fount of their rate policy. Inflation is window dressing.

The core PCE index for July will be released on August 30th.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.