US Consumer Price Index November Preview: Inflation nostalgia

- Headline index expected to fall for the month and rise on the year.

- Core index projected to be stable above 2.0% PCE target.

- Inflation’s impact on Fed rate policy is minimal.

The Bureau of Labor Statistics will release its consumer price index (CPI) for November on Wednesday December 11th at 13:30 GMT, 8:30 EST.

Forecast

The consumer price index is predicted to increase 0.2% in November after adding 0.4% in October. Annual inflation is expected to increase 2.0% last month following October’s 1.8% gain. Core inflation is projected to be unchanged at 0.2% in on the month and 2.3% for the year.

US Inflation: CPI, PCE

The consumer price index and the personal consumption expenditure price index (PCE) are different measures of the change in consumer prices over time. The CPI gauge is calculated by the Bureau of Labor Statistics, the PCE by the Bureau of Economic Analysis. The CPI is the older version and it is probably cited more by the media but PCE is the gauge used by the Fed in setting rate policy.

The measures are broadly similar though not identical. Both indexes calculate rates from the price levels of a basket of goods, the main difference is the composition of each basket and the weight given to each the item. The consumer price index tends to produce a higher inflation rate. According to the Cleveland Federal Reserve CPI has run about 0.5% higher this century.

From a market perspective CPI’s chief interest is as an indicator for core PCE gauge and its impact on Federal Reserve interest rate policy.

CPI, PCE trends

Over the past year overall CPI has moved slightly lower. For the 12 months to October the average is 1.79%, from November 2018 to April 2019 the average is 1.85% for the remaining six months it is 1.73%. The range for the year has been 0.7% from 2.2% last November to 1.5% in February, but both of those rates are from the first half year, in the second half from May to October the range is just 1.6% in to 1.8%.

Core CPI has varied in the reverse, also but slightly. The year is 2.18% with the first six months November to April at 2.12% and the second six 2.23%. The range in the first half is 0.2% in the second it is 0.3%.

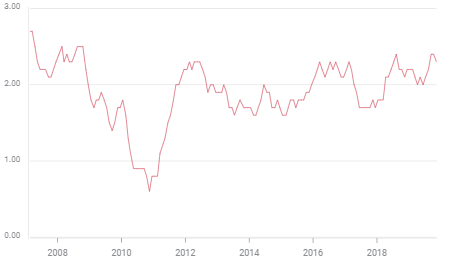

Taking a longer view beginning in May 2012 after the price declines around the recession had been recovered we see the same lack of directional movement.

Core CPI varies from 2.3% in May 2012 to 1.6% a year later, to 2.0% in June 2014, 1.6% in January 2015, 2.3% in March 2016 1.7% in August 2017, 2.4% In August 2018 , 2.0% the following April and then 2.4% this September. About all that can be placed as a trend is that from the first quarter of 2018 onwards the low in the core CPI rate has been 2.0%.

Core CPI

Core PCE provides the same stability. The last 12 months averaged 1.70%, 1.75% in the November to April six and 1.65 in the May to October half-dozen. Like the overall CPI the range was higher in the first half 0.5%, than the second 0.3%. The difference is not indicative of a trend.

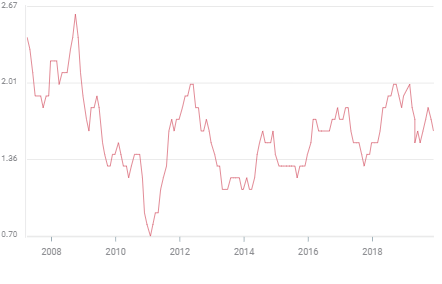

The trend in core PCE has been modestly higher since the recession recovery peaked at 2.0% in March 2012. From there it dropped to 1.1% in various month to January 2014, went back to 1.6% in September 2014, dropped back to 1.2% in June 2015, followed by 1.8% in December 2017, then 1.3% in August 2017, 2.0% in November 2018 and then 1.5% in May and 1.6% in October.

Lows have become progressively higher in the seven year period, 1.1% in 2013 and 2014, 1.2% in 2015, 1.3% in 2017 and 1.5% this year. The upper rate has not gone beyond 2.0% though only reaching there are the beginning and end of the period and nowhere making a symmetric path with the 2.0% Fed target in as the mid-point.

Core PCE

Inflation and Federal Reserve policy

Consumer inflation or specifically price stability is one of the Federal Reserve’s two Congressional mandates. As such it receives much notice and is an integral part of every FOMC statement.

The reference to inflation in the last FOMC statement where the governors cuts the fed funds rate for the third meeting in a row and then moved to a neutral policy could stand in for almost any statement for the past decade. “This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain.”

For the decade after the recession and financial crisis the Fed’s main concern has been restoring growth and employment to the US economy. Under three leaders, Ben Bernanke, Janet Yellen and Jerome Powell inflation has been a secondary goal. For a brief period Mr. Bernanke cited the threat of dis-inflation and outright deflation as a rationale for the early quantitative easing programs but since then prices are mentioned but never the source of policy.

Many analysts, with good monetary supply logic, had expected higher inflation from the massive QE purchases. It never occurred. The demand component of inflation turned out to be far stronger than expected.

Had inflation accelerated the Fed would have been forced to choose between economic growth and price stability. There is small doubt that in the aftermath of the recession the central bank would have chosen growth.

The economic logic of the three rate cuts this year has been defensive, to protect the long-running US expansion and labor market from the potential effects of a global slowdown and the US-China trade war. It was an additional but non-essential benefit that lower rates would be a traditional policy response to low inflation.

It has been more than a decade and it was in a different world when the Fed last made policy decisions based on inflation. The death of former Fed Chairman Paul Volker this week is a marker to the central bankers triumph over inflation.

With the Fed on hold at least through the first quarter, inflation’s importance to rate policy or the dollar is minimal. It’s more nostalgia than anything else.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.