US China trade and the global economy: Q&A with FXStreet senior analyst Joseph Trevisani

Q: The US and China seem to be getting closer to a partial trade deal and a removal of previous tariffs is in the cards.

After the meetings in October it was unclear if the new levies planned for December would be called off. And now, reports suggest that past duties may be removed.

All in all, a positive development, isn't it?

A: Yes but the economic improvement from the trade deal, assuming it is completed, will take time.

Q: But has the damage been done? It is easy to destroy trust and hard to rebuild it.

A: It’s a certainty that the US and China view each other quite differently than they did two years ago. From the US point of view and for this administration in particular trust in China was limited. It has been their contention that China had failed to fulfill prior agreements. The desire to enforce any agreement was one of the factors behind the trade confrontation. Whether the current agreement or a subsequent one will provide compliance is open but performance checks are now an expected topic between the parties.

Q: For now, commodity currencies have advanced and the Japanese yen lost ground. That makes sense. But the greenback had also been gaining ground against the euro and the pound.

A: Dollar strength is an interplay between two factors: safety and growth. The recent move against the dollar has been a retreat from safety or risk-off sentiment. It has been very limited because the fear was minor, a deal has been assumed now for three weeks. The coming balance for the dollar will be on growth. Will the US economy, particularly business investment respond to the fact and the terms of this deal? We do not know the answer. If we see a surge in agricultural orders from China and a recovery in exports then the dollar should respond along with the commodity currencies, the aussie and the kiwi and to a lesser extent the Canadian dollar. It will be the euro and the yen among the majors that will suffer. The fate of the sterling will be determined by the British election and Brexit.

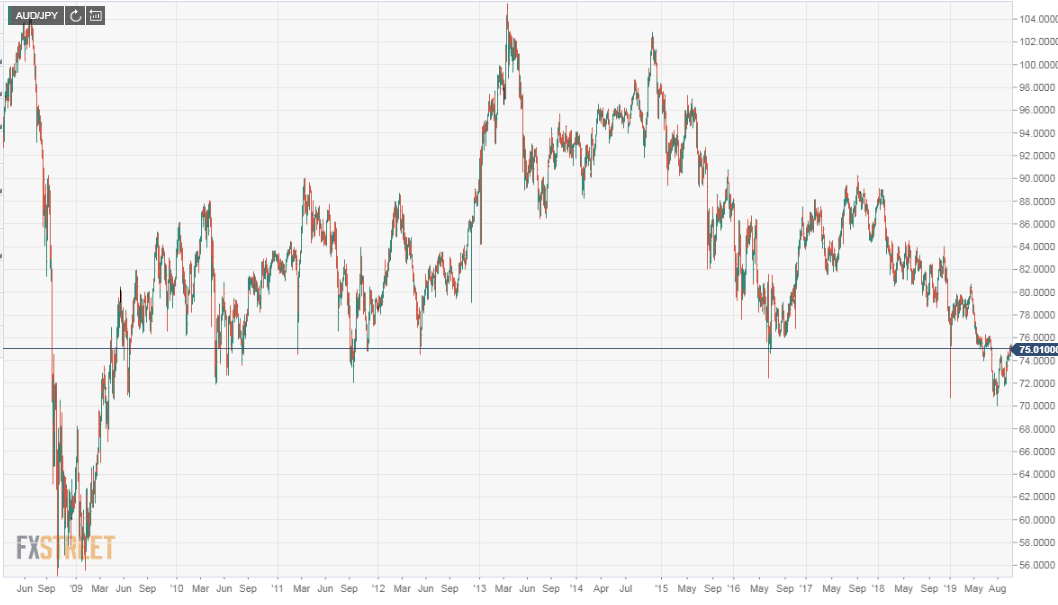

Q: If the trade deal goes through and the aussie and yen go in opposite directions it could be the 2007 carry trade in play again. Could we see the same type of extreme market positioning that was prevalent before the financial crisis?

Q: Probably not. The interest rate differential that drove the cross before the recession is much diminished. In 2007 and 2008 the Australian cash rate was above 6%. However that wouldn’t mean that the cross might not be a smart play. If the trade deal revives the Chinese and the US economies then we could have a scenario that determines trade and currency patterns for a year and more. In that case the AUD/JPY could see a long rise.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.