US ADP Employment Preview: This trend is not your friend

- ADP private payrolls to fall slightly below trends in October.

- Diminished volatility in the third quarter to continue.

- Payrolls’ three month moving average has declined over 25% since February.

Automatic Data Processing (ADP) the largest private payroll processing firm in the United States will issue its National Employment Report on Wednesday October 30th at 12:15 GMT, 8:15 EDT.

Forecast

Companies using ADP’s payroll services are predicted to have employed 120,000 new workers in October following 135,000 in September and 157,000 in August.

NFP and ADP

The chief interest of the ADP report is as a precursor to the Bureau of Labor Statistics (BLS) Employment Situation Summary, commonly known as non-farm payrolls or NFP for its closely followed eponymous statistic.

The ADP number is issued on the Wednesday (occasionally Thursday) before the monthly NFP report which comes out on the first Friday of each month. The payroll report contains the two most watched labor market statistics, non-farm payrolls and the u-3 unemployment rate.

The BLS Employment Situation Summary is the broadest assessment of the US labor market from either the government of the private sector. It tracks the status of job creation, payrolls, wages, unemployment, labor force participation, average work week and other topics.

ADP and NFP

The ADP report is analogous to the private payroll statistic of the NFP information.

There are three primary differences between the ADP report and the BLS summary.

The ADP figure is drawn from the payroll calculations of the company’s approximately 411,000 US clients. The BLS report is compiled from government information nationwide, including all private and government employment at local, state and federal levels.

The ADP report covers only payrolls. The BLS survey is a labor market assessment that tracks many types of information including unemployment rates, average hourly earnings, length of the work week, labor force participation and several others.

The BLS information is the raw material of many government and private studies. It is divided into various categories, private and government employment, type of work, jobless rates and several others and breaks down many of its classifications along age, race and gender lines. In all the BLS report contains 25 different tables of employment statistics and provides the most complete available picture of the US labor economy.

The final difference between the two reports is that ADP is wholly factual, the BLS Summary is not.

The ADP number is transferred from the payrolls processed by the company. If a worker is receiving a check he is counted, otherwise not. There are no estimates.

The BLS non-farm payroll figure is partially a forecast. Each month includes a projection for the number of new jobs created by small businesses that are not known from official government statistics.

This forecast is generated by the so-called birth-death model, referring to the creation and demise of new businesses. This model projects past rates of job creation into the future, its estimates are later compared to the tax rolls and revised.

The revision to the annual NFP figures from this comparison can be substantial. In past years it has been 500,000 or more.

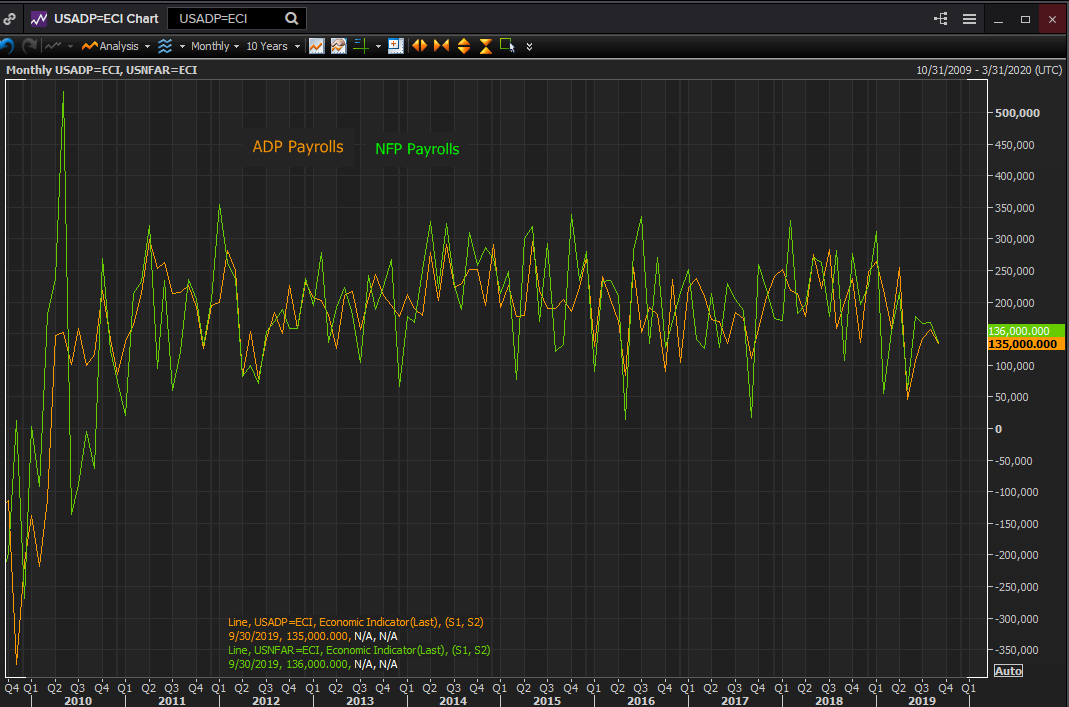

ADP and NFP Trends

Job creation has been on a downward slurge this year.

For the ADP figures the three-month moving average has fallen 28%, from 244, 000 in February to 175,000 in September. The 12-month average has dropped from 220,000 in February to 176,000 last month.

Government statistics have followed suit. Non-farm payrolls are down from 245,000 in January to 157,000 in September in the three-month average and in the 12-month average from 235,000 to 179,000 in the same months.

Despite separate instances of both coincident and divergent volatility in the statistical sets this year, the overall correlation between ADP and NFP has been strong.

Reuters

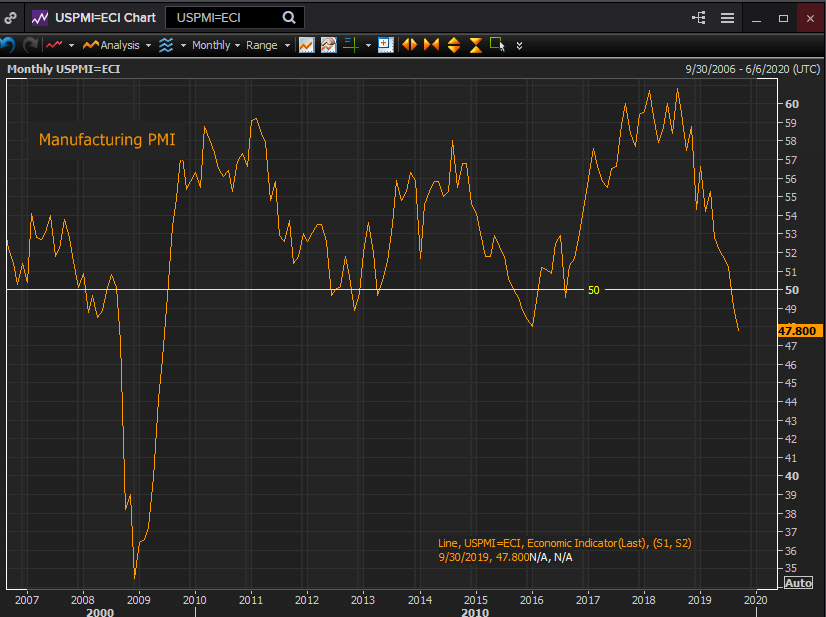

Business confidence and job creation

The trade dispute with China has been the overriding factor in rearranging business optimist from last year's best attitudes in a decade to a borderline recession outlook.

Manufacturing PMI has plunged from 60.8 in August 2018 and 56.6 in January of this year to 49.1 in August and 47.8 in September. These are the first back to back months below the 50 division between expansion and contraction since the five months from October 2015 to February 2016.

Reuters

Attitudes in the far larger service sector, about 85% of US economic activity, have not dipped into contraction but the decline has been as steep, if not as far.

This purchasing managers’ index has fallen from 60.8 in August 2018 to 59.7 in February and 52.6 in September. That is the lowest reading since August 2016 just before the surge that began with the November Presidential election.

Conclusion

The retreat of business optimism has brought a sharp change to the labor market this year. New employment has slowed about 25% from its high of ten months ago. It is not the current level of job creation, which remains healthy, that is of concern but the continuation of the trend lower.

The ADP and NFP figures are approaching levels where new work is scarcer than the available supply of labor. With the backlog of unfilled posts accumulated over the past two years it might be some time before the decline in new work was felt in wages and consumer sentiment.

Coincident labor market indicators from jobless claims to unemployment rates and wage gains do not suggest trouble ahead. But though they are important in gauging consumer sentiment, these statistics are largely retrograde. Employers are reluctant to fire workers and it is not until problems are imminent that these measures register danger.

The Federal Reserve has repeatedly said that its goal in keeping the economic expansion running is to bring the benefits of the work to as many people as possible.

With business sentiment and investment moribund until the China trade deal takes concrete form, it has been consumer spending that has maintained near 2% growth since the first quarter. In turn it is their relatively optimistic sentiments, maintained by the job market, that have kept consumers in the stores and on the web.

The Fed’s expected rate cut on Wednesday and the two previous ones have been justified by global threats to the US economy. If job creation continues to fall, external threats will no longer be needed to explain future accommodation.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.