US ADP Employment Change February Preview: Fears but few facts

- February private payrolls projected to moderate after very strong January.

- ISM manufacturing employment index rose in January.

- First quarter GDP estimate from Atlanta Fed is 2.7%.

Automatic Data Processing (ADP) the US private payroll processing company will release its National Employment Report for February on Wednesday March 4th at 13:15 GMT, 8:15 EDT

Forecast

Payrolls for ADP’s clients are expected to have increased 170,000 in February after adding 291,000 workers in January and 199,999 in December.

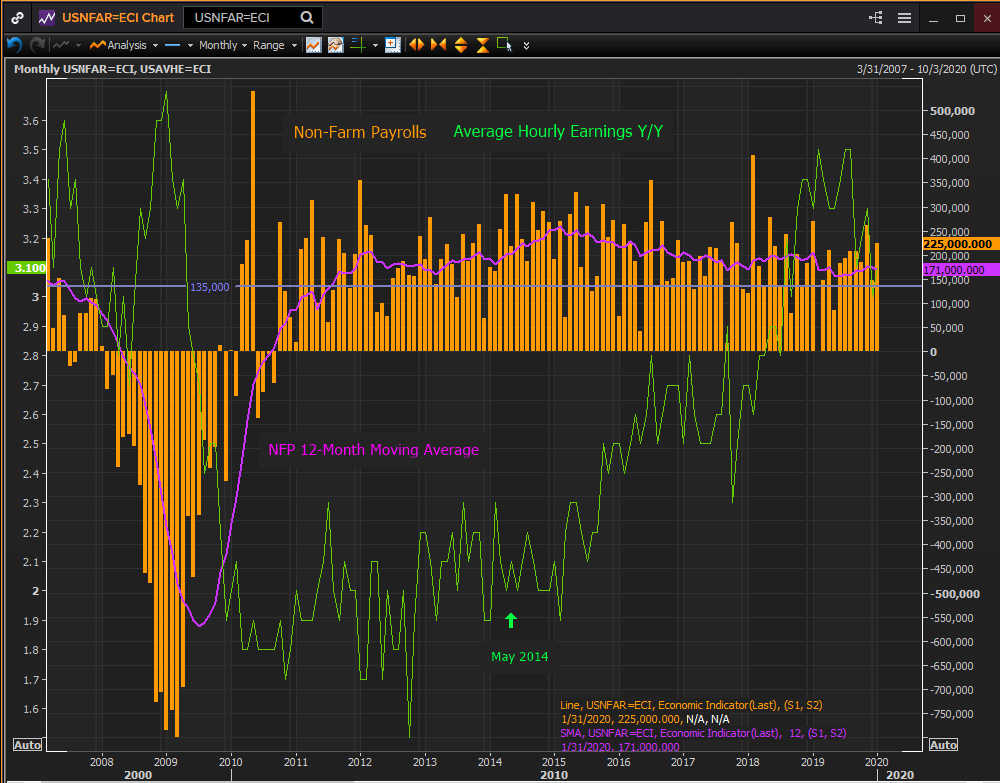

ADP and NFP: Labor market trends

Payrolls moderated in 2019 with the 12-month moving average for the national NFP falling from 235,000 in January to 174,000 in December and ADP’s private accounting dropping from 222,000 to 163,000. Both were surprisingly robust in January with ADP at 291,000 its strongest month in a year and NFP at 225,000.

The US labor force adds about 135,000 new workers each month through population growth and immigration. Payrolls have been above this limit in the 12-month average since August 2011 though the 8.7 million jobs lost in the recession were not replaced unlit May 2014.

That is the primary reason wage gains for the first half of the recovery were well below their historical average. It was not until labor shortages began to build from 2016 on that employers began to offer higher compensation to attract workers.

Reuters

ADP and NFP: Labor market part and whole

The ADP Employment Change Report is the closet match for the Employment Situation Report from the Bureau of Labor Statistics (BLS). It is essentially a limited version of the NFP private payrolls measure. The chief difference between the overall NFP figures and the ADP measure is the inclusion of local, state and federal government employment in the BLS information.

Reuters

Over time the trend correlation between the NFP and ADP measures is high though individual monthly variation is not uncommon. In 2019 the 12-month moving average for the NFP and the ADP both decreased 26%, (NFP 25.9%, ADP 26.5%).

Labor Market Actors: PMI, jobless claims, unemployment

Despite the evolving impact of the Coronavirus on global economic growth, China appears to be returning to work, the manufacturing purchasing managers’ index for February maintained expansionary sentiment. The overall index was 50.1, missing the 50.5 forecast and below January’s surprise jump to 50.9 from 47.8 which had matched the lowest post-recession reading. The employment index rose to 46.9 from 46.6 where it had been expected to remain. New orders fell to 49.8 in February from 52.0 in January as forecast.

Reuters

The index for the much larger services sector will be released on Wednesday March 4th. The general gauge is projected to decrease to 54.9 from 55.5 in January and the employment index is expected to rise one point to 54.1. New orders are also predicted to increase to 56.3 from 56.2.

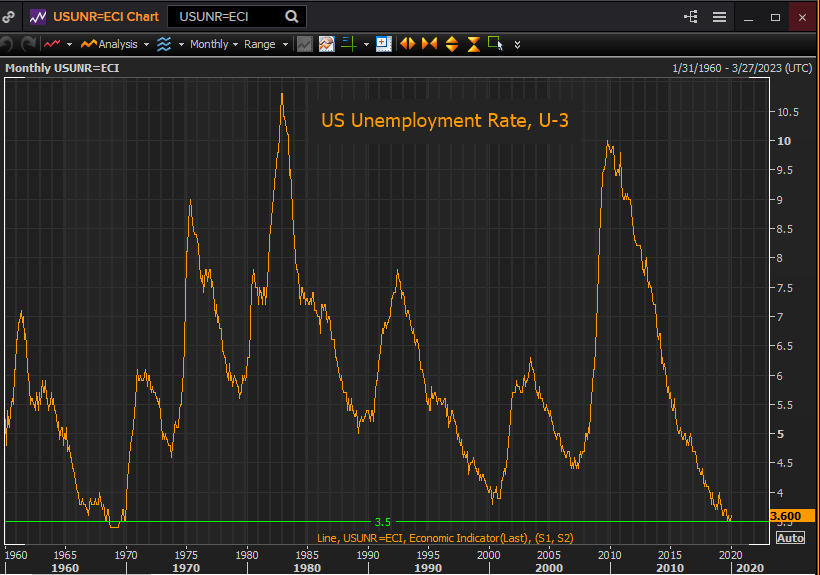

Initial jobless claims are a reliable indicator of pending trouble in the labor market. In the latest reporting week (February 28) the four-week moving average was at 209,750 a half-century low. Coupled with the unemployment rate of 3.6%, also a 50 year low, there is little notice of labor market stress.

Reuters

Conclusion and the dollar

The trade war and Brexit threats to US employment, except in manufacturing, never materialized. Purchasing managers’ indexes for January and February in the factory sector indicate that damage from the viral problem has not yet made managers change their outlook substantially.

We will see on Wednesday if the service sector is a sanguine as its smaller cousin, but it would be unusual if manufacturing industries, which are far more exposed to problems in China, maintained their confidence and their service colleagues did not.

It may be that the supply disruptions from the mainland have not made it to factory floors in the US, or it may be that stockpiles were sufficient to ward off production delay, or it could be that the impact will be felt in coming months.

In the current tight labor market it would be a surprise to see managers cut back on hiring without concrete information that the viral threat is going to result in real and prolonged cutbacks in production.

The dollar has paid the price over the past two weeks of the world’s safety surge into US Treasuries. The yield on the 10-year bond has fallen over 60 points since February 12th, cutting to a record low under 1% in Tuesday trading. The Fed 0.5% rate cut will soon be matched by similar reductions at most major central banks, in what was evidently a concerted move by the bankers to head off the equity contagion.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.