UK growth surge takes GDP above pre-virus level

The UK economy reached its pre-virus level in November, and early evidence suggests Omicron's damage may be modest enough not to take activity back below. A February Bank of England rate hike is growing more likely.

At 0.9%, UK monthly growth was surprisingly strong in November, surging well above consensus and our own expectations of a 0.4% gain. And interestingly the move is fairly broad-based. Construction and manufacturing were strong, though the former has been pretty volatile admittedly. A strong Black Friday gave retail sales a boost, but also the associated transport and warehousing activity.

Reading through the ONS press release, it feels like some of this bumper growth is down to unseasonally large swings in certain components that might be partly unwound in the next couple of readings, which might have the effect of amplifying the impact of Omicron on the December and January GDP readings.

But the bigger question is whether the arrival of the new variant has been enough to take monthly GDP back below its pre-virus level, which was comfortably surpassed in November. We suspect it may not, though it will be close. The impact of Omicron appears to have been fairly modest, at least relative to past waves.

Partly, that’s because it looks like Covid-19 cases have now peaked nationally – suggesting Omicron’s wake has been sharp but hopefully short-lived. That should help ease the staff shortages that have become particularly acute over recent weeks. The latest ONS business survey suggests sickness rates were in excess of 5% in the consumer services industries.

But early signs also suggest Omicron hasn't prompted a long-lasting change in consumer attitudes towards Covid-19. No doubt that is linked to the booster vaccine still offering strong protection against serious illness.

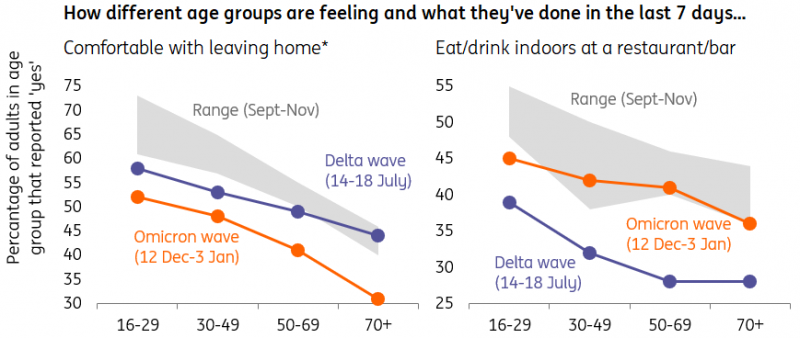

Admittedly, if we look at the most recent ONS attitudes survey, we did see a noticeable fall in the proportion comfortable with leaving home towards the end of 2021, and more so than during the Delta wave last summer.

People were more willing to visit hospitality than during Delta wave

Source: ONS Coronavirus and the social impacts on Great Britain

'Range' covers surveys between early September and late November

But as the chart above shows, the same survey showed only a minor change in the percentage visiting indoor hospitality venues. One possible outcome of this is that people hunkered down to avoid isolating over Christmas, but may become less cautious now the festivities are over.

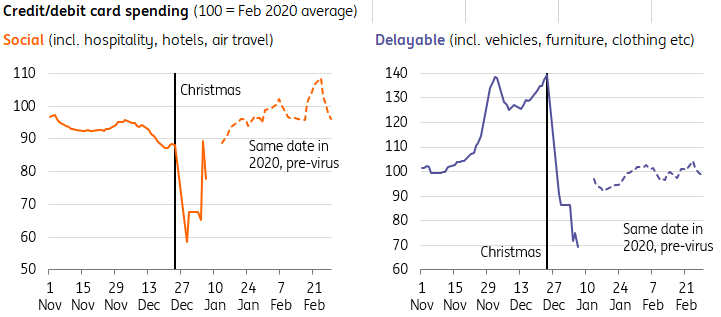

There are traces of that story in the latest card spending data. While this has been highly volatile over Christmas, the most recent readings for January aren’t that dissimilar to spending around the same time in 2020, before the pandemic.

Social spending is close to comparable 2020 levels, according to CHAPS data

Source: Macrobond, ING

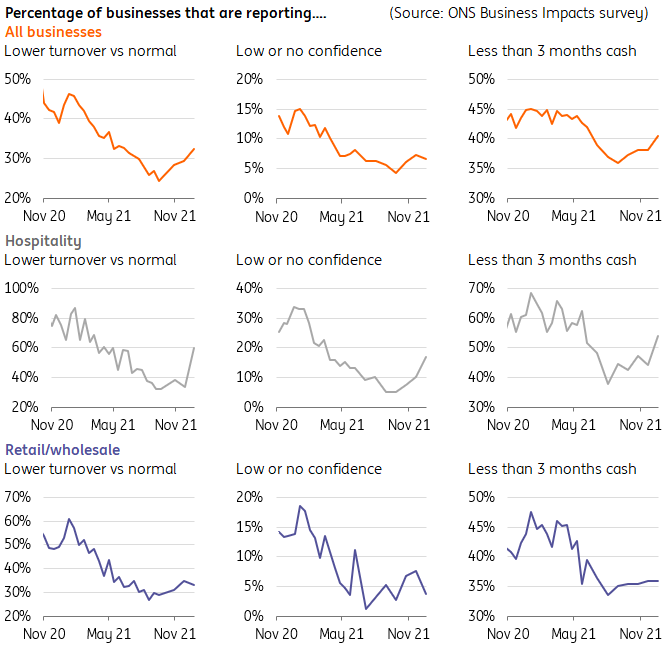

That offers hope that the hit to firms’ finances over Christmas won’t be long-lasting either. More firms reported lower turnover, cash reserves, and confidence in the latest ONS business survey, and unsurprisingly more so in hospitality. But these percentages are still a fair bit lower than they were last winter/spring, as the charts below show.

In short, the hit to GDP across December and January may not amount to much more than half a percent, not least because the recent booster vaccine and testing expansions may help boost health spending yet further, offsetting weakness elsewhere. For comparison, GDP fell by over 2% last January, from already compressed levels.

For the Bank of England, this suggests the chances of a February rate hike are rising. While there’s a reasonable case for waiting to get full clarity on Omicron, December’s surprise rate hike decision showed that the committee, like that of the Federal Reserve, is less worried by Covid-19 than it was previously.

The early impact on businesses has been less pronounced than past waves

Source: ONS Business insights and impact on the UK economy, ING calculations

Read the original analysis: UK growth surge takes GDP above pre-virus level

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.