The State of the US Electorate and the Markets: A one way street until the Fall

- Economic recovery is the key to the re-election of President Trump.

- Markets have recovered most of their pandemic losses.

- Treasury rates have been held down by Federal Reserve bond purchases.

Presidential election years are the pinnacle of political entertainment in the United States. There is more public interest, more press coverage, more voting and this year more polarization than in any election in a generation.

There are also more than the usual number of moving parts. Aside from normal political rhetoric, since the election of Donald Trump more angry and divisive than ever, there have been large protests over racism in many American cities, riots, looting and attacks on public monuments in others, rising urban crime, and vehement cultural and historical disputes that have boiled over into almost every sphere of American life. If that wasn't enough, the pandemic continues to course through society fraying nerves and unemployment is at its highest level since the Depression.

The candidates this year, Republican President Donald Trump and Joe Biden the presumptive Democratic nominee whose official nomination is not until August, are probably the two most unusual competitors since the early days of the Republic two centuries ago.

Without entering the political arena ourselves, we will look at the state of the parties and their relation to the candidates, the view from the financial markets and venture some guesses about the campaign in the summer before its unofficial start on Labor Day.

Candidates and parties

Both candidates have high approval rating from their respective parties, President Trump at 85% from Republicans and Biden at 74% from Democrats in surveys from Gallup.

President Trump’s overall approval rating, a good but not infallible guide to incumbent reelection odds, has fallen from 47.3% in early April to 43.0% on June 21 in the RealClearPolitics (RCP) average as the coronavirus, unemployment and then protests and riots have dominated news coverage for more than three months. Historically a president’s chances for a second term drop as approval falls below 45%.

Another comparison is between the approval ratings of Presidents Trump and Obama at comparable points in their first terms. Until the pandemic and its economic damage Trump had held a notable advantage for the first time in his presidency.

The national average for the election currently gives Biden an 9.5% lead, 50.6% to 41.1% (RealClearPolitics, 6/21) though polls this far out are not a good indicator for the November vote. At this point in the 2016 contest Clinton was ahead by 10 points. She won the popular vote by 2.1% due to large pluralities in California and New York but lost the Electoral College which elects the president 306 to 232.

All 435 representatives are up for reelection as they are every two years and 35 out of 100 senators. The Democrats control the House 235 to 197 with two vacancies and one Libertarian member. They won 40 seats and took control of the chamber in the 2018 elections. Republicans run the Senate 53 to 45 with two independents who caucus and vote with the Democrats. Republicans have 23 Senators for election this year and the Democrats 12.

The Democrats lead in the so-called generic Congressional vote, which asks which party is more likely to get an individual’s vote irrespective of candidates, by 8.5%, 49.0% to 40.5% (RCP, 6/21). Given the voter distribution any lead above 6% shows a Democratic advantage.

Geography gives the Democrats, with huge margins on the West Coast and in the Northeast a decided advantage in the popular vote and the Republicans an edge, though not as large, in the Electoral College that actually elects the US chief executive. In 2016 Mr. Trump secured victory by winning Pennsylvania, Michigan and Wisconsin, traditionally Democratic states by the small margin of about 100,000 votes across the three states.

US Economy

The state of the economy, particularly employment is historically the most telling condition for a president’s reelection.

Prior to the advent of the pandemic in the US the economy had been President Trump’s strongest asset. With unemployment below 4% for all of 2019 and minority rates at record lows, the longest economic expansion and job creation stretch in US history coupled with rising wages for lowest paid workers. The President seemed on the way to a relatively easy election. The pandemic has upset almost every aspect of that calculation.

Unemployment is at its highest since the Depression, 46 million people have filed for jobless benefits and 20 million were fired or laid off in April, though 2.5 million were rehired in May. Retail sales collapsed 16.4% in April but then rocketed 17.7% in May, each month setting the all-time directional record. Industrial production plunged 12.5% in April and rebounded just 1.4% in May.

Consumer sentiment has recovered from its April low, 78.9 in the Michigan June index but is far from its near decade high reading of 101 in February.

Initial claims remain punishingly high. The four week moving average was 1.773 million and continuing claims stayed above 20 million in the latest figures though a decline had been forecast.

That the unemployment was caused by government mandated shutdowns and social restrictions in most states matters less for the election than the ability of the administration to point to a strongly reviving economy. By and large American supported the initial restrictions as necessary to counter the coronavirus pandemic.

Federal Reserve and government actions

The Federal Reserve and Washington has expended enormous efforts to mitigate the impact of the pandemic shutdowns on individual, families and businesses across the country.

More than six trillion dollars have been granted or loaned in various programs providing financial resources to keep workers on payrolls and as direct gifts to individuals and families. These government expenditures are in addition to the standard 26 weeks of jobless benefits that almost all fired workers can receive.

US economy and the election

The past is less important than the future. While there is no expectation that the economy or the labor market will recover its pre-pandemic verve by the November election that probably matters less than the ability of President Trump to be able to point to a strong, if incomplete recovery.

Three factors will determine the rate of improvement in the next five months.

Will the reopening economy bring large numbers of people back to work? The 2.5 million added to non-farm payrolls in May is an encouraging sign but it needs to mount quickly for the impact to be self-sustaining.

Second was the burst of consumer spending in May the result of three months of deferment or is it an indication that Americans are ready to resume their normal habits undeterred by the lingering social restrictions?

Third will the consumer economy encourage employers, especially of small and medium sized firms to bring back workers, creating a feedback loop of employment leading to higher consumption and in turn to more hiring?

Were there no other factors but a one-time exogenous shock to the economy the course of the recovery would likely follow the path outlined above.

The coronavirus pandemic is the unknown. If states are forced to institute business closures again and unemployment rises the limited improvement that has happened and the prospect for more would be badly undermined. The victims would be not only President Trump’s election chances but the optimistic outlook that has governed markets for the past three months.

But even if cases in the US continue to rise governments may have difficulty re-imposing restrictions because of the tolerance given to the many protests over the past several weeks. A number of governors have said they will not order business closures.

The country may have to learn to live with the virus until a treatment or vaccine is found. An open but wary US economy will grow more slowly than a fully restored one.

Markets: Equities, currencies and Treasuries

Markets have not begun to price the November election but are still absorbed by the reaction and recovery from the pandemic panic.

Equities have rebounded smartly from their March 23 low. The S&P 500 closed at 3097 on Friday down just 4.12% on the year and that includes its all-time high of 3393 on February 19. On the full year it is up 5.85%. The Dow has had almost equal success. It finished at 25,871 last week , down 9.35% this year and 2.39% over 12 months, (all close on 6/19).

The dollar has surrendered all of its pandemic risk premium in the major pairs with some like the euro and the aussie returning to their immediate pre-panic ranges and others as the yen and the sterling trading at levels from earlier last year.

Treasuries are the outlier among three major markets with yields well below their ranges in February. The 2-year Treasury was returning 0.188% on Friday far lower than its 1.447% close on February 6. The 10-year closed on Friday at 0.699% less than half its February 6 finish of 1.644% (all close 6/19).

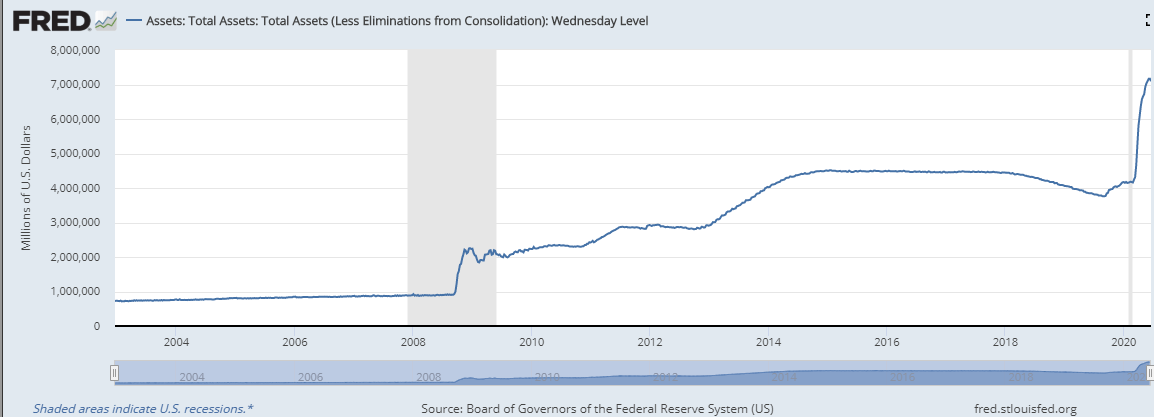

The absolute and sustained decline in Treasury yields and commercial interest rates overall is solely due to the Fed’s revived quantitative easing bond purchases initiated in March. Fed assets have soared $3 trillion in the past three months, almost as much as the $3.5 trillion gain in the six years of financial crisis purchases and the bank has extended its buying to various commercial issues.

Conclusion: Markets and the election

Markets are likely to remain agnostic on the election until the Fall. The reason is quite simple. Polls this far from November 3 have little predictive value. Short of a change in candidates what happens between now and Labor Day is the preliminary for the main event.

Historically, Republican candidates and party platforms have been viewed as more favorable to business and markets and better stewards of the economy. That has been changing in recent years with a majority of Wall Street money going to Ms Clinton in 2016. Mr. Trump was emphatically not the candidate of the Republican Party or corporate establishments in that election.

With the Democratic Party’s pronounced left-ward move in the last four years that balance may shift again. Mr. Biden will be presented as a moderate but it will be difficult to discount the many alternate and far more radical voices from the party. All of the cities that have seen riots have been under Democratic control for many years, a fact that may not be lost on the electorate and that the Trump campaign is sure to use.

For July and August the economic recovery and the progress of the pandemic will be the central focus for the markets. The faster and more secure economic growth the better the chances for President Trump in November.

If the economy does continue to improve the coinciding gains in equities and the dollar should not be considered a reflection of President Trump’s rising odds but the normal interplay between markets and Main Street.

The attitude of the markets to this election and its highly unusual economic, political and cultural landscape and the enormous degree of polarization in the electorate may make a strict good or bad for business analysis next to impossible.

Mr. Trump’s approach to politics and the economy is well-known, the markets have yet to hear from Mr. Biden.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.