The faltering 10-year yield gets a lot of the blame for the dollar’s weakness

Outlook:

Today we get the Chicago PMI and University of Michigan consumer confidence sur-vey (with inflation expectations), but the important one is Q1 GDP. Bloomberg has a forecast of 1%. (Canada also reports GDP, expected at 0.1%.) Analysts are already brushing off a bad US number as consistent with previous first quarters and in any case, not likely to sway the Fed on its path to the June rate hike. We get nonfarm payrolls next Friday, considered more influential.

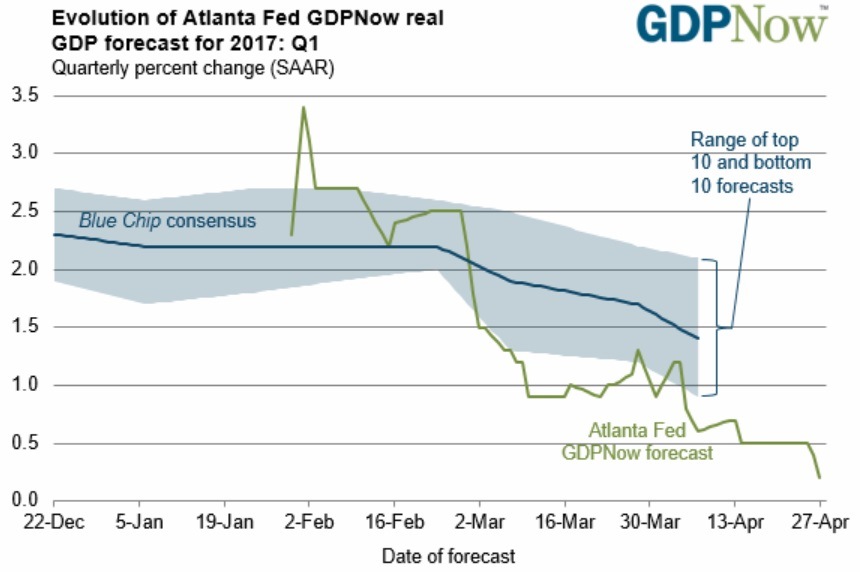

We are not so sure. What if the Atlanta Fed is right? Yesterday it reported its GDPNow model says 0.2%, from 0.5% last week and well over 2% in Feb. See the chart. This time the Atlanta Fed number was dragged down by weak consumer spending, inventory adjustments and durables. We get the next update on Monday.

We are worried about the divergence between the Atlanta and the New York Feds' economic forecasts. The NY Fed has 2.7% for Q1 and 2.1% for Q2. A giant discrepancy like this makes folks think econo-mists don't know what they are doing, or that the Fed doesn't know what it's doing. We have enough of that doubt from the White House.

We also have doubt about whether various segments of the financial world know what they are doing. One sector thinks the sky might be falling (bonds, commodities) while the equity gang is gung-ho, full speed ahead. Bloomberg asks "What do Treasury markets know that their credit and stock counterparts don't? That's the question investors are asking themselves as they survey a confusing market land-scape."

"Real interest rates, money-market rates and the U.S. Treasury curve are pricing in expectations that are inconsistent with the exuberance in the stock market. The term premium -- or the compensation inves-tors demand to own longer-date obligations versus shorter-dated ones, for example -- is back in negative territory, underscoring skepticism over the Trump-fueled reflation trade."

See the chart. How worried should we be? It's possibly a looming showdown between unwarranted risk appetite and overly gloomy fixed income sentiment. One analyst says it's too early to worry about the divergence between stocks and bonds. Worry normally comes later in the tightening cycle.

The FX market tends to be far more influenced by bonds than by stocks. The faltering 10-year gets a lot of the blame for the dollar's weakness. Equities get neither credit nor blame. Everyone keeps trying to find correlations between stocks and FX rates, but they are inconsistent and unreliable. Weirdly, for the most part rising equities are associated with a falling dollar—but don't count on it.

Meanwhile, money is pouring into Europe again. BoA ML reports today that inflows into eurozone equity funds are the biggest since the US election, $21 billion in the latest week. This is considered a "risk-on" flow following the first round of the French election, according to Reuters. "Much of this year's stock market rally across the globe is down to a $1 trillion ‘liquidity supernova' of financial as-sets that central banks in Europe and Japan have bought so far this year... The bull market is unlikely to end until bullish macro (data) makes central banks tighten (monetary policy) - we're not yet there."

Reuters reports "Investors poured $2.4 billion into European equity funds, the most since December 2015, and $13.8 billion into U.S. funds, the most in 19 weeks, BAML said. Bond funds attracted $10.9 billion of inflows in the week to Wednesday, with more than half of that ($5.6 billion) going into in-vestment grade funds and a further $2.1 billion into emerging market debt funds, BAML said."

This information is not much help in forecasting exchange rates, but it does imply that we have a long wait for central banks to take away the punch bowl, implying perhaps a range-trading environment.

Other forms of sentiment get blame for the soft dollar, too. As the 100-day mark arrives tomorrow, the Trump presidency can lay claim to no new legislation at all. Congress will avoid a government shut-down by passing a continuing resolution today, but Trump doesn't get credit for that. Trump failed in every initiative in the first 100 days and has a major administration figure, National Security Advisor Flynn, facing jail. Moreover, Trump has flip-flopped on a slew of campaign promises, including immi-gration, health care, NATO, the Wall, and NAFTA. If it's on-the-job training, good, but the guy is er-ratic and can flop back.

The new tax "plan" benefits the rich and the Trump family in particular. It also throws any notion of fiscal responsibility out the window. A battle with Congress looms. Don't count your chickens before they hatch.

Looking forward, it's a bank holiday in London on Monday, implying FX action will be muted—unless something awful happens in the geopolitical realm. But the latest on N. Korea is that China is helping, according to Trump (really?), and there might even be talks (Tillerson). But Trump ruined it by saying there is risk of a "major, major conflict." We can hope it's just another effort to distract attention from his dismal failures as a "leader."

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.46 | LONG USD | 04/26/17 | STRONG | 111.34 | 0.11% |

| GBP/USD | 1.2938 | LONG GBP | 04/12/17 | STRONG | 1.2495 | 3.55% |

| EUR/USD | 1.0936 | LONG EURO | 04/13/17 | STRONG | 1.0643 | 2.75% |

| EUR/JPY | 121.88 | LONG EURO | 04/25/17 | STRONG | 120.15 | 1.44% |

| EUR/GBP | 0.8452 | LONG EURO | 04/25/17 | STRONG | 0.8490 | -0.45% |

| USD/CHF | 0.9907 | SHORT USD | 04/13/17 | STRONG | 1.0043 | 1.35% |

| USD/CAD | 1.3634 | LONG USD | 04/24/17 | STRONG | 1.3415 | 1.63% |

| NZD/USD | 0.6870 | SHORT NZD | 04/12/17 | WEAK | 0.7022 | 2.16% |

| AUD/USD | 0.7479 | SHORT AUD | 03/28/17 | WEAK | 0.7607 | 1.68% |

| AUD/JPY | 83.36 | SHORT AUD | 03/22/17 | STRONG | 85.20 | 2.16% |

| USD/MXN | 19.0287 | LONG USD | 04/28/17 | NEW*WEAK | 19.0287 | 0.00% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat