The countdown

S&P 500 formed a fine bull trap – the intraday reversal making selling into worthwhile. How about today, given that bonds didn‘t exactly crater into Monday‘s close?

Premarket European session didn‘t disappoint me, and the prospects of a sustainable rebound today look shaky at best. The upcoming consumer confidence would be propped by the ability to withstand inflation through savings, access to credit and continued debt load relative serviceability.

Reminder from yesterday‘s key analysis before heading for the rich daily chart section:

(…) Tuesday‘s consumer confidence data are likely not to disappoint as personal savings rate had been recently revised upwards (4.7%), suggesting that the consumer still has the wiggle room to withstand inflation. Remember when I was telling you last year that consumer strength would be the defining factor in the shape of the upcoming recession – and contrast that with what we have seen play out in the markets in only the last couple of weeks – from hard to soft landing, then the no landing came (as if strong Jan data in non- farm payrolls and housing not tanking on, are to be proven as little more than a year entry oddity and brief respite).

Seriously, I expect the job market to start noticeably deteriorating (e.g. in unemployment claims) from Mar onwards, and the ongoing mortgage rates of 7% to snuff out the temporary housing stabilization. Circling back to the consumer, retail sales for now wouldn‘t be deteriorating either – while rising in nominal terms, they had been really flat in real terms since mid 2021, revealing the spending growth to be of merely inflationary nature.

So, that‘s Tuesday and consumer confidence which still shouldn‘t tank the markets – regardless of the woeful and nonchalantly ignored bond market performance over the recent weeks (these rates would keep biting even more, especially on the short end).

The latter half of this week doesn‘t look to be promising for stock bulls though – especially the manufacturing, and to a lesser degree services PMIs, are to reveal recessionary clues impossible to ignore.

Remember the sequence of recession countdown and progression – first real estate going down (check), manufacturing down (check), services with a lag (check), inflation peaking (sure the revisions and calculation „revamps“ helped here), and finally job market layoffs spreading (wait for Mar / Apr) together with earnings coming in weak (check) forcing sigtnificant earnings downgradeds for the quarters ahead (still to come, seriously starting late Q2 even as modest earnings recession has already arrived, and the low $180s EPS need solid downgrading).

Plenty to look for as stocks readjust to new economic realities!

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there (or on Telegram if you prefer), but the analyses (whether short or long format, depending on market action) over email are the bedrock.

So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open with notifications on so as not to miss a thing, and to benefit from extra intraday calls.

Let‘s move right into the charts.

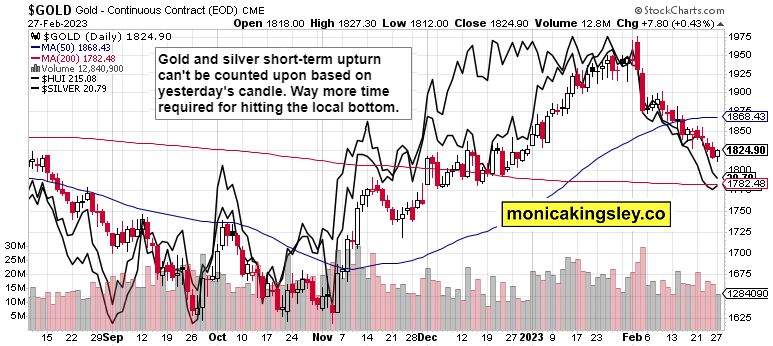

Gold, Silver and miners

Precious metals haven’t yet found a bottom – gold and miners daily upswing is a mere pause, which would be extended by USD relief rally topping out. We aren’t there yet, and gold and silver just can’t sniff out the nonexistnt Fed pivot till the summer short-term yields peak (best case scenario).

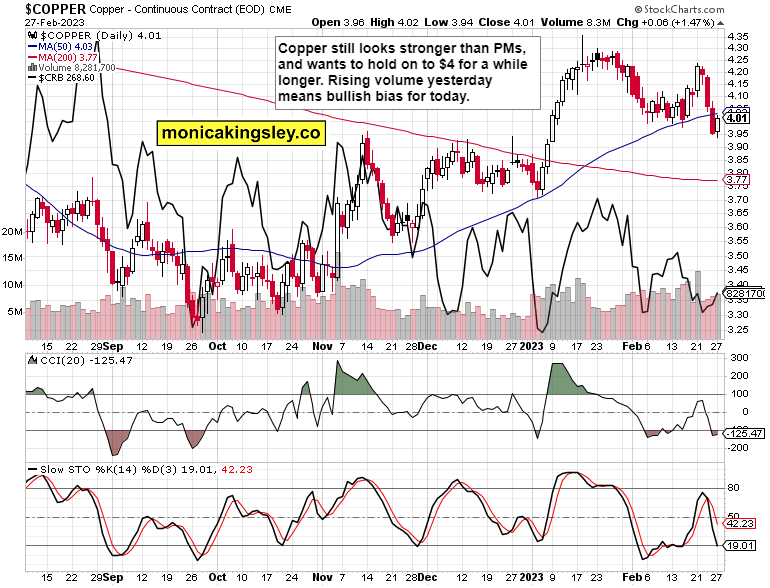

Copper

Copper acts still resilient, and $3.70 strong support may not come into play fast at all as stockpile fundamentals with China on top, win out. The same would support oil into the high $70s and you might have benefited from the bullish natgas call on Twitter too. The time for washouts in energy, seems over.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.