The Bank of England Preview: Dark side of Brexit makes MPC uncomfortably numb

- The Bank of England Monetary Policy Committee (MPC) is widely expected to keep the monetary policy on hold at the meeting with the November Inflation Report set to highlight Brexit uncertainties.

- Brexit darkens the growth and policy outlook for MPC with the main question being what kind of trading relationship will ultimately evolve from the Brexit negotiations.

- The MPC is likely to express increased satisfaction with the development of the UK economic fundamentals, especially the UK inflation.

The Monetary Policy Committee (MPC) of the Bank of England is expected to keep the monetary policy unchanged at the November meeting at its decision scheduled for Thursday, November 1 at 12:00 GMT. Apart from the rate decision, the November Inflation Report is out with the Bank of England Governor Mark Carney justifying the decision at the subsequent press conference.

The reasons behind the broad market consensus not to expect any changes is clear, the Brexit uncertainty. In fact, it is all about Brexit these days as the time for both the European Union and the United Kingdom to close the Brexit deal is ticking up. After the October European summit failure, the need to come up with some kind of the deal in November is imminent, as there is no more time to negotiate further.

Related stories

In terms of UK economic development, the Bank of England should be happy as the labor market tightness confirms its August decision to hike the Bank rate by 25 basis points.

The UK regular pay growth accelerated to 3.1% y/y in the three months to August after posting three 0.4% monthly increase, making the regular pay growth rate the strongest in almost a decade. The corresponding total pay including bonuses rose from 2.7% y/y to 2.8% y/y in three months to August while the unemployment moved toward a multi-decade low of 4.0%.

The labor market tightness has started finally feed through into somewhat higher wages, allowing employees to be compensated a bit for the previous rise in inflation and keeping the real, inflation-adjusted wages in positive.

The key policy target, the UK headline inflation decelerated to 2.4% over the year in September missing the market estimate of 2.8% y/y rise, while core UK inflation stripping the consumer basket off food and energy prices at the same time decelerated to 1.9% y/y.

In terms of inflation expectations of UK households, recent surveys indicate that inflation should stay relatively weak. IHS/ Markit’s Household Finance Index survey indicated that inflation expectations over a 12-month horizon fell to their lowest in two years, even as households still reported a steep rise in current living expenses.

The move of inflation moving back towards the inflation target and the inflation expectations of UK households well anchored should keep the Bank of England in check, at least for now. The Bank of England now has more time to maneuver and watch how the labor market is affecting UK wages and inflation at the end. The next move on UK rate will see the UK officially outbound from the European Union making August or possibly November next year conditionally realistic. Of course depending on the upcoming Brexit deal and the data. That’s the sure shot.

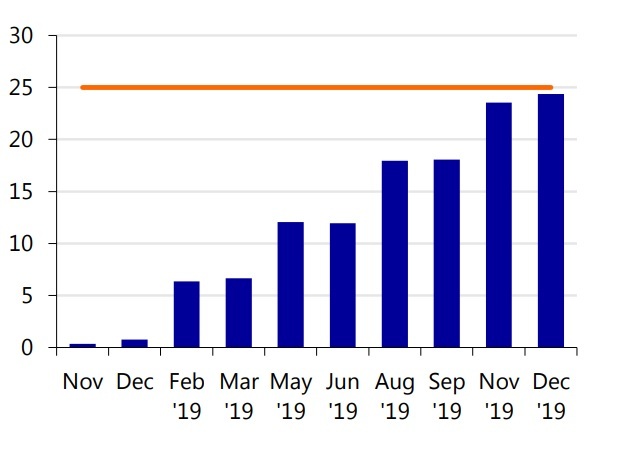

Market probability of Bank of England hiking the Bank rate

Source Bloomberg

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.