Stagflation embrace

S&P 500 didn‘t look back following the underwhelming NFPs and the stark tech leadership coupled with meaningful enough retreat in yields provide for an inflection point in equities. Not that yields would have topped, but running with Powell‘s not hawkish message easing Treasuries financing and ushering more of yen appreciation as well, is changing the game, and answering the dip vs. deeper downleg question for the week ahead.

Junk corporate bonds and Treasuries support more gains ahead as the QT taper means less pressure when financing budget deficits, hence less competition for stocks from bonds. It‘s a subtle change that has to play out still more – so ingrained has the belief in dovish Fed become that the market is once again ready to salivate for rate cuts (for now Sep only, but we are to see some more rise in the underdog Jun cut bets) even if all that‘s responsible for such a stark shift, is the absence of government hiring that did not bring NFPs in line with expectations as a result, just as per my tweet linked to above.

This also allows for more risk taking as yields become less attractive. Look though at 2y Treasury and compare its daily candle to the 10y year – the more sensitive 2y yield failed to keep all the daily decline made, meaning that it‘s less convinced about easy Fed from here on. This is semantics for very short-term traders that are likely to get a little retracement of sharp equities gains before Monday‘s US open – but bigger picture, the boot on equities‘ neck courtesy by bonds, is being lifted for as long as sensitivity to poor incoming data is on par with Friday - in other words, for as long as Powell is taken as dovish when all he is doing via the QT taper, is helping to keep a lid on rates.

This is still the most important chart, indicating some relief from risk-off environment, is at hand, and may even send gold with silver a bit up following the disappointing sell into Friday‘s turn.

Source: stockcharts.com

Just as the dollar struggled at my 106.50, so the 10y correspondingly won‘t make it this fast above 4.90% - and that‘s a generally risk-on development that makes a break below pre-FOMC S&P 500 lows unlikely. At least till the week of May 13 when new inflation data come out.

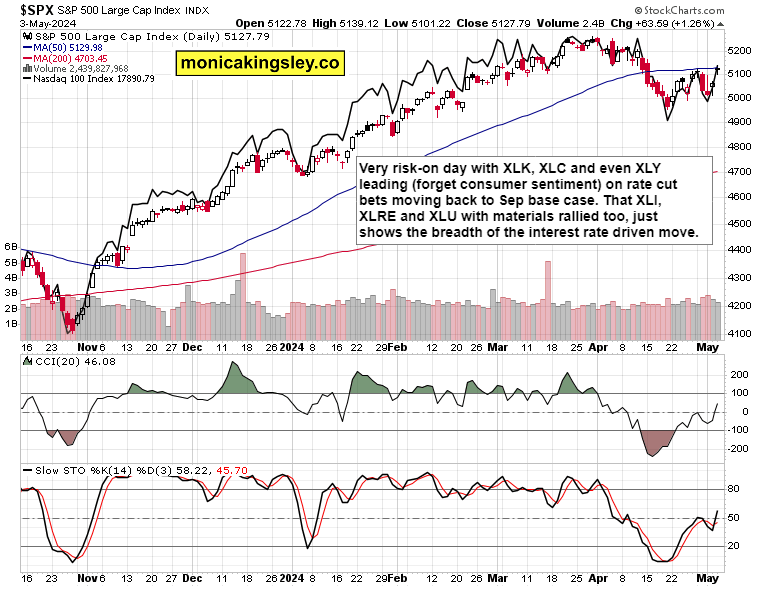

S&P 500 and Nasdaq

Source: stockcharts.com

S&P 500 even moved up 1 min before NFPs announcement, and looked back just once, typically midsession and after hot ISM services prices. Russell 2000 is a bit mirroring the 2y Treasury‘s relative caution – but the market breadth is good, and strong Nasdaq showing shaking off META, NFLX, SMCI and TSM earnings impact via AAPL follow through, bodes well for higher stock prices in the days ahead.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.