Services PMI rebounds from thee year low, new orders, employment indexes rise

The US service sector grew more than anticipated in October as crucial gauges of new orders and employment rose suggesting that the yearlong descent may have stabilized, perhaps awaiting details of the proposed US China trade accord.

Purchasing managers’ indexes from the Institute for Supply Management (ISM) increased in four important categories last month mirroring the gains in the manufacturing survey released this past Friday.

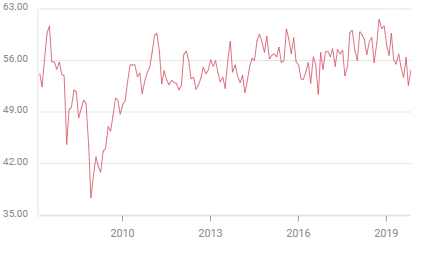

The headline index climbed to 54.7 in October from its three-year low of 52.6 in September. It has been forecast to reach 53.5. Business activity rose to 57.0 from 55.2, also outstripping the 55.0 median prediction. Employment jumped from a five-and a half year low of 50.4 in September to 53.7 and new orders mounted to 55.6 from their 37-month bottom of 53.7.

Services PMI

One caveat to the upturn was the new export orders index which fell to 50.0 in October, a more than two-year low, from 52.0 in September. This is in sharp contrast to the same index for manufacturing which soared 9.4 points to 50.4 in October.

US economic growth has paralleled the decline in the ISM indexes this year. Annualized GDP has slipped from 3.1% in the first quarter to 2.0% in the second and 1.9% in the third. Both the manufacturing and services indexes peaked at 60.8 in the third quarter of last year, manufacturing in August and Services in September.

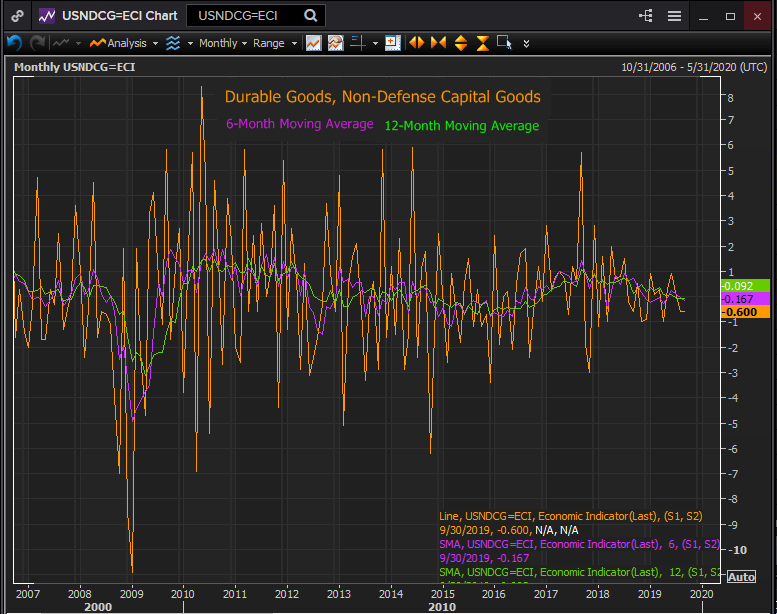

Business investment has been the weak link in the US economy for the last year responsible for most of the drop in GDP. The durable goods category of non-defense capital goods ex-aircraft, an oft used proxy for business investment spending, was negative in both the six-month and 12-month moving averages at -0.167% and -0.092% respectively in September.

Reuters

Despite the drop in economic growth the labor economy has remained healthy.

The October payrolls report showed 128,000 new positions in spite of the General Motors strike which cut between 46,000 and 80,000 from the job rolls. Revisions to August and September added 95,000 bringing the three-month moving average to 176,000. The GM jobs should return in November.

Between 125,000 and 150,000 monthly jobs are needed each month to provide employment for new entrants to the labor force.

Average annual earnings have risen at a 3% or better pace for 15 months and unemployment has been at or close to five decade lows for 18 months.

These three reports have helped to mitigate concerns that the decline in manufacturing was a harbinger for the much larger service sector.

They have also reinforced the judgement of the Federal Reserve in moving rate policy to neutral after last Wednesday’s third 25 basis point cut this year. Chairman Powell’s characterization of the US economy being in a “good place” now seems self-evident.

The yield curve in the 2 and 10-year Treasuries which had inverted briefly in late August exciting recession talk, has since reversed and widened to a normal 23 points, (2:00 pm EST).

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.