Risk–off in summer trading

Market Brief

The risk rally, which followed the UK referendum, has slowed somewhat with the Dow falling for the first time in nine sessions. Optimism over further stimulus from the ECB and BoJ was tempered slightly while questions over equity valuations forced investors to hit the pause button. Meanwhile, events in Turkey have fuelled a steady sell-off of Turkish assets and an avoidance of the broader EM complex. In yesterday's ECB policy meeting Draghi sounded ready to act but nevertheless preferring to postpone further easing. In Japan, speculation of impending “helicopter” money took a hit as an old BBC interview had the BoJ’s Kuroda apparently ruling out the extreme policy action. In response, the Nikkei fell -1.25% (gap down at open) pulling Shanghai and the Hang Seng lower. FX was mixed with the USD gaining broadly against EM currencies. USDJPY traded marginally higher to 106.26 on the Nikkei Asia Review headline that the Japanese composite stimulus package at the 28th-29th July policy meeting could reach JPY30trn. Yet, ahead of the G20 meeting in Chengdu, as well as the FOMC and BoJ meetings, traders remain cautious, with USDJPY quickly retracing earlier gains. Elsewhere, Japan's manufacturing sector remained in contraction territory as manufacturing PMI rose to 49 in July from 48.1 in June.

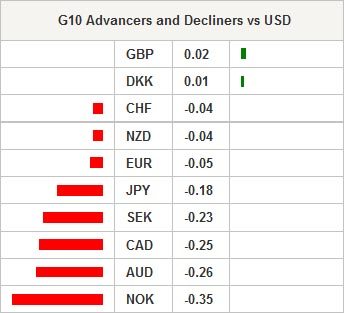

Overall, G10 currencies remain subdued with little directional momentum. Commodities traded lower, with oil slipping to $44.40brl, pulling commodity-linked currencies down. On this summer Friday, we suspect volumes will remain thin with price actions respecting near-term trading ranges.

In an uneventful ECB monetary policy meeting yesterday, policy remained unchanged. Mario Draghi, provided no surprises and though sounding ready to act he asserted his preference to hold fire with a view to reviewing policy in September. With the true extent of the Brexit fallout still unclear, and the Euro on the weaker side (due to renewed expectations for a September Fed rate hike), the central bank is under no real pressure to act. However, given the softness of growth data and the mounting risks to the inflation outlook, we suspect that the September meeting will announce a time extension of QE and an expansion of parameters for eligible assets of QE. EURUSD bounced around 1.1060 and 1.0980 but settled at the mid-point. With our expectation for additional ECB easing and growing speculation of a September Fed hike, EURUSD faces further downside risk. We remain bearish on EURUSD as upside should be limited by 21d & 200b MA located at 1.1074.

This weekend the world’s finance ministers and central bankers will meet in China. Key topics on the table will include the effectiveness of policy including QE and negative rates as the focus will have increasing shifted to fiscal policy. It goes without saying that the subject of Brexit will also loom large and potential economic challenges will dominate discussion. Yet despite talk over collaborative policy development, we don’t anticipate any meaningful progress.

With a light economic calendar summer trading should be in full effect. In the European session Euro area `flash` PMI will be released. Markets anticipate erosion across the board as economic conditions across Europe soften and the outlook due to Brexit dims. `Flash` PMI composite should decline to 52.5 from 53.1, dragged downs by a sharp fall in manufacturing (expected to decline into contraction territory at 48.7 from 52.1). There are no tier 1 events or economic releases in the US session.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 16627.25 | -1.08 |

| Hang Seng Index | 21920.27 | -0.36 |

| Shanghai Index | 3010.87 | -0.9 |

| FTSE futures | 6634.5 | -0.32 |

| DAX futures | 10119 | -0.43 |

| SMI Futures | 8153 | -0.28 |

| S&P future | 2158.5 | 0.02 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1323.81 | -0.55 |

| Silver | 19.65 | -0.7 |

| VIX | 12.74 | 8.24 |

| Crude wti | 44.36 | -0.84 |

| USD Index | 96.94 | -0.05 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| Markit/CIPS UK Composite PMI | 49 | 52.4 | GBP/10:00 |

| Markit Eurozone Services PMI | 52.3 | 52.8 | EUR/09:00 |

| Markit Eurozone Composite PMI | 52.5 | 53.1 | EUR/09:00 |

| Markit Eurozone Manufacturing PMI | 52 | 52.8 | EUR/09:00 |

Currency Tech

EURUSD

R 2: 1.1428

R 1: 1.1186

CURRENT: 1.1032

S 1: 1.0913

S 2: 1.0822

GBPUSD

R 2: 1.3981

R 1: 1.3534

CURRENT: 1.3260

S 1: 1.2851

S 2: 1.2798

USDJPY

R 2: 109.14

R 1: 107.90

CURRENT: 107.13

S 1: 103.91

S 2: 99.02

USDCHF

R 2: 1.0328

R 1: 0.9956

CURRENT: 0.9872

S 1: 0.9764

S 2: 0.9685

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Peter A Rosenstreich

Swissquote Bank Ltd

Peter Rosenstreich is Swissquote Bank’s Head of Market Strategy and manages the global strategy desk; he has held various positions in several banking institutions in the United States, Europe & Asia.