Reflation Rally Pauses as Safe Haven Flows Recover

The dollar, sovereign yields and global equities have drifted lower as political turbulence in the U.S. pushes investors to take profits on recent gains.

A percentage of the market remains unsettled by Trump’s administration’s focus on controversial topics such as immigration and a lack of news on how he plans to push through promises of tax cuts and fiscal spending made during his campaign.

Stiff opposition to some of POTUS’s cabinet picks and the resignation of his NSA adviser earlier this week is adding to the feeling of political uncertainty and we all know that capital markets despise uncertainty especially ahead of a long weekend stateside.

1. Stocks lose momentum after record-breaking week

Global equity markets have retreated modestly going into the weekend after solid gains for much of the week, tracking less upbeat sentiment on Wall St.

In Japan, the Nikkei closed -0.6% lower, down -0.7% for the week, while in Australian, shares fell -0.2% at the close, shrinking the week’s gains to +1.5%.

Chinese shares have fared little better, slipping after earlier touching a near two-month high after the securities regulator said that, starting Friday, it will relax certain rules on stock index futures trading. The CSI 300 index has lost -0.4%.

In Hong Kong, the Hang Seng tumbled -0.9% as financial snapped their winning streak.

In Europe, equities are trading under pressure, paring their second weekly advance, led by commodity producers. The Eurostoxx is down -0.6% from the weight of energy companies, while a disappointing U.K retail sales print (see below) has the FTSE back peddling.

U.S equities are set to open in the red (-0.3%).

Indices: Stoxx50 -0.6% at 3289, FTSE -0.2% at 7266, DAX -0.5% at 11702, CAC-40 -0.9% at 4855, IBEX-35 -0.7% at 9484, FTSE MIB -1.0% at 18896, SMI -0.3% at 8444, S&P 500 Futures -0.3%.

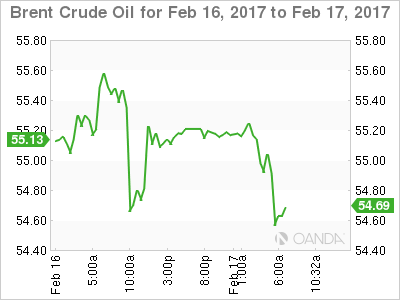

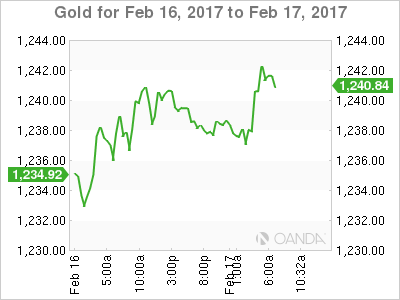

2. Oil prices slip, gold trades atop of three-month highs

Oil prices remain confined to a tight range ahead of the U.S open. On one hand, growing global stocks are pressuring crude prices, while expectations that an output cut by OPEC might eventually balance the market is helping to support prices.

Brent crude futures are trading at +$55.57 per barrel, -8c below yesterday’s close, while U.S. West Texas Intermediate (WTI) crude futures are down -4c at +$53.32 per barrel.

Note: OPEC has agreed to cut output by almost -1.8m bpd during the first half of 2017, with industry data showing that most producers are sticking to the deal (+93% compliance).

Despite this, inventories remain bloated and supplies high, especially in the U.S. This week’s EIA report showed that crude and gasoline inventories soared to record highs last week as refineries cut output and gasoline demand softened.

Crude inventories rose +9.5m barrels, while gasoline stocks rose by +2.8m barrels.

Note: Both Brent and WTI crude has traded within a +$5 per barrel price range so far this year.

Gold prices are holding firm (+0.2% to +$1,241.56 an ounce) and is and is set for its seventh weekly gain as the dollar hovers near its one-week lows amid political uncertainties in the U.S. and Europe.

Note: The yellow metal up +0.3% so far for the week, and has risen about +7.5% so far this year. The prospects of a stronger dollar and U.S yields pushed gold to +$1,216.41 on Wednesday, its lowest since Feb. 3.

3. Bund/French spreads widen on political worries

France’s election campaign took another twist this morning. The Socialist Party presidential candidate Hamon said he’s holding further talks with far-left candidate Melenchon about a potential single candidacy. A merger could bring about a showdown with Le Pen’s anti-euro National Front. Recent polls suggest the two candidates would make it to the second round of elections in May.

French 10-year yields climbed +3bps to +1.05%, widening the spread over 10-year Bunds (+0.31%) by +6bps.

Elsewhere, the yield on the U.S 10-year note is little changed at +2.46%. It dropped -5bps yesterday after increasing +16bps in the previous five-days.

Down under, Aussie 10-year yields were higher for a sixth day, adding just under +1bps to +2.80%.

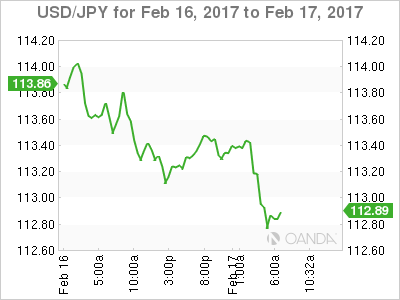

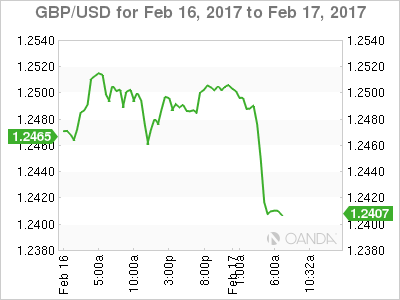

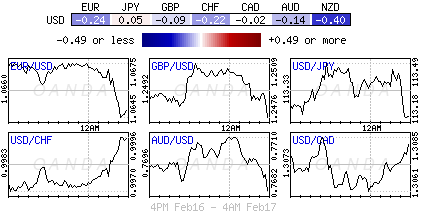

4. Dollar clueless in confined range

The FX majors (€1.0645, £1.2403, ¥112.86) are confined to tight trading ranges in the absence of meaningful data; with the USD index trading atop of its one-week lows. Already this week, U.S yields have brushed off most of the recent upbeat data and a “hawkish” Fed, which is capping the USD uptrend.

Investors can expect the upcoming elections in Europe (Netherlands and France) to continue to drive currency volatility over the coming months, while uncertainty over Trump’s domestic policies are expected to cap the ‘big’ dollar’s advance for the time being.

The overnight exceptions was the pound, GBP (£1.2397) saw a sharp break lower after a disappointing monthly sales print (see below), but remains contained within its recent ranges. Sterling bears are eyeing the key support level of £1.2350 for direction.

5. U.K retail sales disappoint again

U.K. retail sales fell last month for the third consecutive month, a sign that rising prices from a weakened pound (£1.2406) are beginning to weigh on consumer spending.

Note: Decembers data posted the fastest monthly decline in over five years, which suggests that rising prices are squeezing Britons’ wallets in the wake of the last June’s Brexit vote.

Retail sales declined -0.3% m/m, with higher prices for both food and fuel were “significant factors” in the drop. This is further proof for the Bank of England (BoE) that the U.K economy is set to slow this year as quickening inflation squeezes household budgets.

Note: The December print was also revised down to -2.1%. The annual pace of growth in January stood at +1.5%, the lowest pace of expansion in over three-years.

Author

Dean Popplewell

MarketPulse