Political stuff keeps overwhelming fundamentals

Outlook:

The ECB meets in ten days (Oct 26) and may announce a cut in asset-buying to begin next year, aka tapering. This is going to be euro-supportive at some point. We repeat this com-ment from yesterday because we are bombarded on all sides by political and institutional sto-ries that are overwhelming economic fundamentals.

Even Spain gets into the act, saying growth will be cut to 2.3% next year from 2.6% earlier projected because of the Catalonia showdown. It's far too early for anyone to be able to guess the effect on growth. An announcement like this is designed not to disclose valuable information, but to influence political opinion.

We are seeing our judgment vindicated that "institutional factors" outweigh economic fundamentals. This is usually a reflection of the low regard in which most people, traders included, hold economics. Economics deserves the bad reputation. It bases expected outcomes on unrealistic assumptions and un-workable postulates, including that economic man is rational and always decides in favor of his own self-interest.

Besides, political bombshells are so much more fun than dreary old economics. For example, Canada stared down the EU over a trade deal last fall and walked out of talks. It got the deal in the end. All the talk about damage to the respective economies was a waste of time. More recently, the White House imposed tariffs on Canadian company Bombardier, naming unfair subsidies. The top headline in the FT this morning is that Airbus will take over the contested program, which includes ramping up production in Alabama (of all places). You might think Trump or Commerce Secy Ross was crazy like a fox to have engaged in the trade war between Boeing and Airbus, but in practice, nobody really knew how the contretemps was going to end, unless Airbus was colluding with Boeing. This was not a well thought-out strategy based on principles, but rather a risk-risk gamble based on impulse and emotion.

We have the same thing in NAFTA. Trump initially wanted to withdraw entirely but in the end was "persuaded" to reform, instead. Reform initiatives are unreasonable, implying the other guys are being herded into withdrawing or walking out. To make matters more complicated, Trump wants The Wall and has said the government can go dark when it runs out of money in December if it doesn't approve funding for the wall, although hardly anyone believes him. Then there is Trump's preference for bilat-eral deals over multilateral deals, so much easier to be a bully. Trump's idea of negotiating is to wear the other guy down, like a 2-year old and an exhausted parent.

The unintended consequences are enormous and spill all over the place. The peso is at the lowest since May. Even the CAD is starting to suffer, with questions arising over what the BoC really does want—hikes or not? Nobody knows how much the NAFTA talks are influencing the BoC, let alone the price of oil, and the price of oil does have a correlation with the dollar, although it's weird and unreliable.

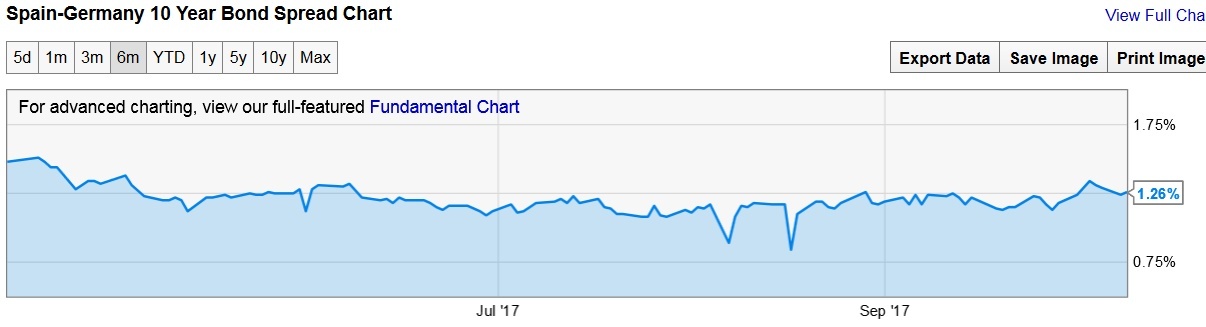

Where the rubber meets the road is the yield differentials. We may want to jump to the conclusion that the euro is soft because of Catalonia. But if that were the case, we'd expect the yield differential be-tween Spain and the Bund to be soaring. It's not. See the chart. The diff is 1.26% now, but was higher six months ago.

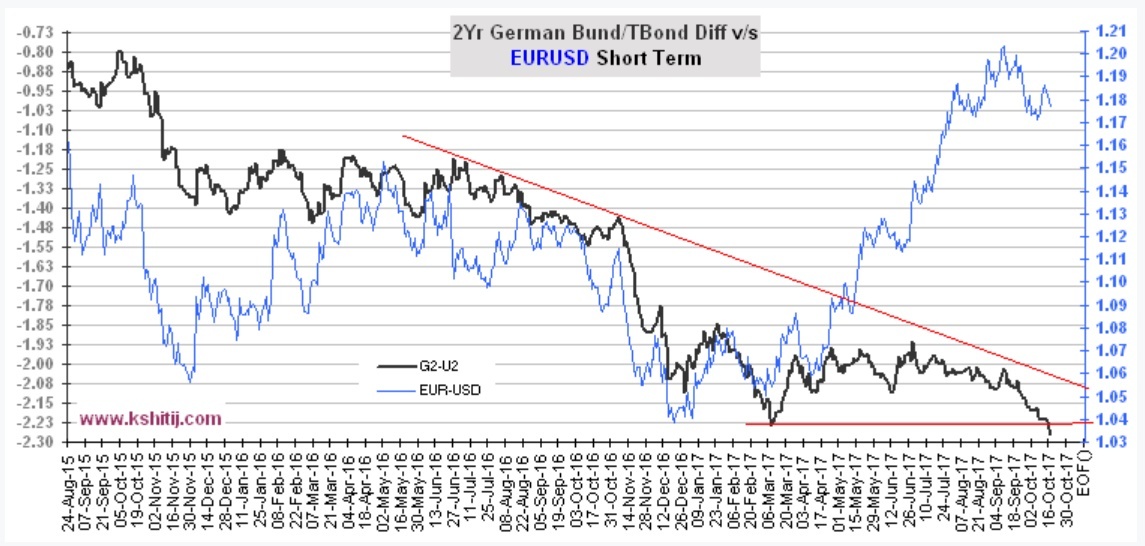

Similarly, the yield differential between the US and Germany should be rising strongly to justify the stronger dollar. Granted, the US 2-year is higher, supposedly the tenor most sensitive to central bank expectations, but the yield curve is flatter. This presumably means the market accepts the Fed rate hike in Dec but doesn't believe additional hikes will be justified by the data. Besides, the recent rise in the differential is barely making a dent in the euro/dollar. See the Kshitij chart.

Perhaps the euro "should" fall to get back in sync with the differential. But since March, the diver-gence is going the wrong way. Golly, what happened in March? Plenty of things, but we would pick the rising acknowledgement that Trump is not going to deliver on campaign promises, especially tax reform and infrastructure spending, and can't get along with Congress, i.e., doesn't play well with oth-ers. So there we are again, with shiny political stuff overwhelming fundamentals. That implies that fun-damentals like today's industrial production (and Treasury capital flows report) will take a far back seat. Bah.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.16 | SHORT USD | 10/15/17 | WEAK | 111.82 | -0.30% |

| GBP/USD | 1.3256 | SHORT GBP | 10/03/17 | WEAK | 1.3247 | -0.07% |

| EUR/USD | 1.1759 | SHORT EURO | 09/27/17 | WEAK | 1.1741 | -0.15% |

| EUR/JPY | 131.89 | SHORT EURO | 10/15/17 | WEAK | 131.86 | -0.02% |

| EUR/GBP | 0.8871 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 1.79% |

| USD/CHF | 0.9768 | LONG USD | 09/25/17 | WEAK | 0.9732 | 0.37% |

| USD/CAD | 1.2532 | LONG USD | 09/27/17 | WEAK | 1.2389 | 1.15% |

| NZD/USD | 0.7178 | SHORT NZD | 10/06/17 | STRONG | 0.7088 | -1.27% |

| AUD/USD | 0.7852 | SHORT AUD | 09/25/17 | WEAK | 0.7963 | 1.39% |

| AUD/JPY | 88.08 | SHORT AUD | 10/11/17 | WEAK | 87.35 | -0.84% |

| USD/MXN | 19.0474 | LONG USD | 09/22/17 | STRONG | 17.8066 | 6.97% |

| USD/BRL | 3.1717 | LONG USD | 09/27/17 | WEAK | 3.1670 | 0.15% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat