New Zealand dollar rally under threat from rising political risks

The New Zealand dollar had surged by around 10% between May’s 2017 low point and July’s two-year high, making it one of the better performing currencies of the year against the US dollar. However, central bank unease about the strength of the currency, downgrades to the government’s growth forecasts and an unexpectedly tight election race have derailed the rally.

Even as the New Zealand economy enjoys strong growth and a huge government surplus, the kiwi has stumbled upon some unexpected risks, forcing the currency into a sharp downside correction.

The kiwi first came under heavy pressure on August 10 after the Reserve Bank of New Zealand stepped up its concerns about the strong exchange rate. Its downslide intensified on August 23 after the government revised down its forecasts for economic growth for 2017 and 2018. The revision was mainly due to reduced expectations for the construction sector as a result of capacity constraints, with the overall outlook remaining bright. But the lower projections allow less room for future tax giveaways, and thus diminished chances of further fiscal stimulus.

More recently, a surprise boost in support for the Labour party has unnerved markets as the country heads off to a general election on September 23. Labour’s 37-year old leader, Jacinda Ardern, has only been in the job for just over a month but has managed to close the party’s gap with the ruling National party, led by Prime Minister Bill English. The National party was comfortably expected to win the elections before “Jacindamania” swept the country. Labour were trailing the National party by 10 points prior to Ms. Ardern’s appointment as party leader on July 31.

The prospect of a surprise win for Labour has investors worried as the party plans to cancel the tax cuts announced by the National party to fund increases in health and education spending. They also want to introduce new taxes such as on tourism and water, cut immigration, and reform the country’s central bank, the Reserve Bank of New Zealand.

Labour is proposing to change the RBNZ’s mandate from focusing on just inflation to a dual one to include employment, similar to the Federal Reserve in the United States. Such a reform is seen as being negative for the New Zealand dollar as it would probably lead to lowered expectations on future interest rate hikes. A dual objective of inflation and employment could force the RBNZ to keep rates lower for longer to accommodate growth in the labour market.

The elections have already disrupted operations at the RBNZ as it has delayed the appointment of a new governor. The current governor, Graeme Wheeler, is due to step down on September 26 and will be replaced temporarily by Deputy Governor Grant Spencer, who will act as a caretaker for six months. The next meeting on September 28 will be his first as Governor. Spencer is known to be more hawkish than Wheeler, however, it’s unlikely there will be a significant shift in RBNZ policy until a permanent Governor has been appointed.

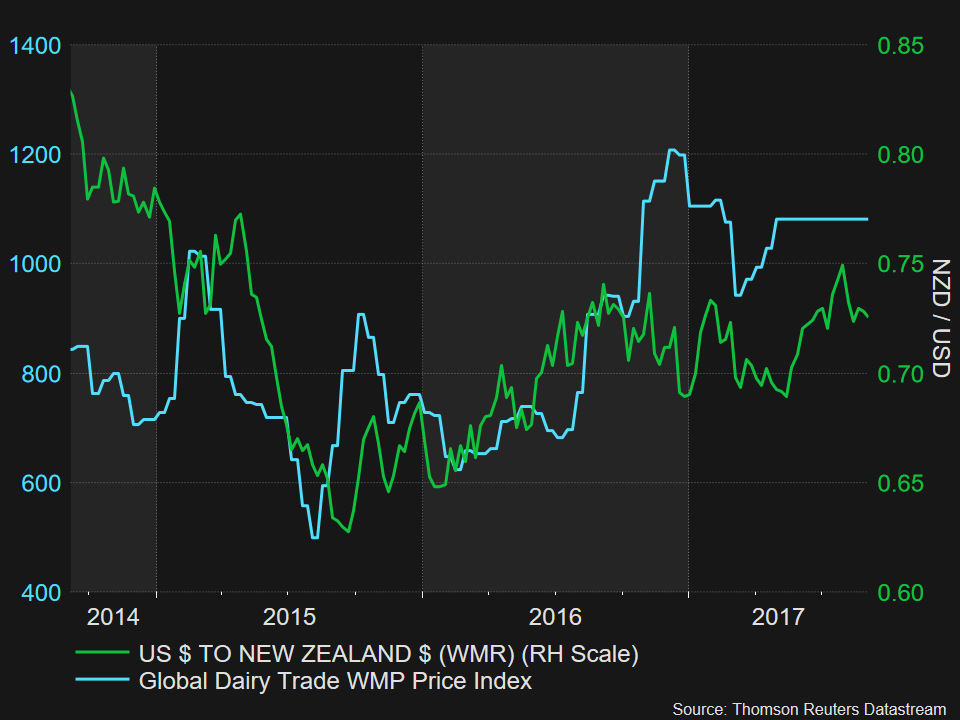

In the meantime, the kiwi is struggling to find its bearings, having retraced about half of its May to July gains, as uncertainty over both the future government and central bank policy hang over the currency’s outlook. External factors have also weighed on the kiwi, as the bout of risk aversion associated with the geopolitical tensions in the Korean peninsula has dampened sentiment for riskier assets. Strengthening demand for commodities has not been much of a boost for the kiwi either as prices for New Zealand’s main export, dairy, has been largely flat this year.

An election win for Labour could propel the kiwi to further declines in the near term, though strong economic fundamentals should prevent a sharp depreciation. Moreover, the odds of a change to the RBNZ’s mandate are very strong if Labour were to form a coalition with the likely election kingmakers, the New Zealand First party, who also support reforming the central bank. Such a move could push up the yield on long-term government bonds as markets would view the RBNZ to be more tolerant of inflation.

On the other hand, an expected win for the National party could potentially act as a trigger to reignite the kiwi’s rally, and with the US dollar looking increasingly bearish, a break of July’s two-year peak of $0.7558 could prove an easy challenge. However, traders will be wary of driving the kiwi higher too fast and by too much as it could prompt an intervention by the RBNZ, which remains an open option for the bank.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl