India’s retail inflation soars to 7.79% in April 2022, higher than most estimates

Key highlights

- UK economy shrank 0.1% in March as inflation and the Ukraine war takes a toll.

- US Inflation barreled ahead at 8.3% in April from a year ago, remaining near 40-year highs.

- Morgan Stanley cuts India growth estimates and warns of 'worsening' macros.

- China's money supply expanded in April as the central bank unleashed more liquidity

- Bank of Japan chief rules out the near-term chance of tweaking dovish guidance

- India’s Forex reserves fall $1.774 billion to $595.954 billion

USD/INR weekly performance & outlook

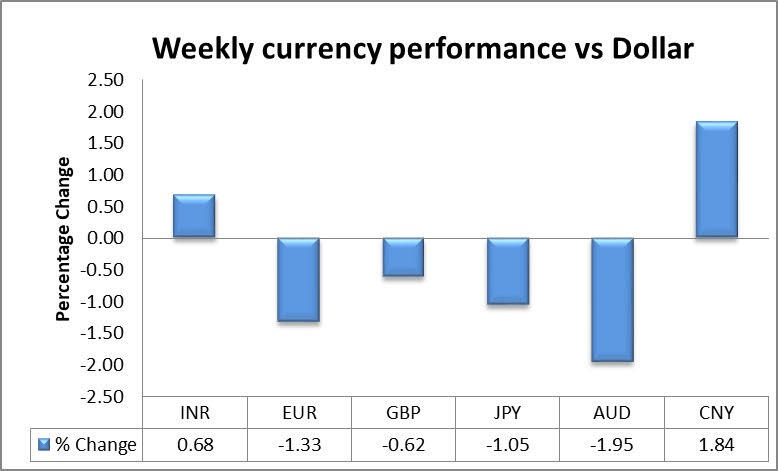

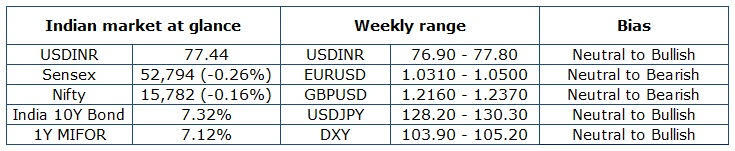

The USD/INR pair made a gap up opening at 77.12 and remained volatile during the week. The pair closed the last day of the trading session at 77.44 levels. The USDINR ended higher tracking a weak domestic stock index and a strong dollar on fear of an aggressive rate hike by the Federal Reserve and global risk aversion. Market's fears were mainly propelled by the inflation woes that push global central bankers toward dialing back the easy money and challenging the already weary economic growth. The elevated crude prices also kept the Indian rupee under pressure. The Indian Rupee is expected to remain under pressure amid a strong dollar and elevating inflationary pressure in India. Persistent FII outflows are also expected to weigh on the domestic currency. The US dollar is expected to remain strong in the week ahead amid risk aversion in the global market. Additionally, the outlook for the global economy is looking gloomy amid supply chain disruption, lockdown in China, and Russia’s war against Ukraine which is expected to keep the safe-haven dollar in demand. Since the time Russia invaded Ukraine, the Rupee has depreciated about 3.8% while other EM currencies have depreciated 4-7%. The Rupee has therefore strengthened in relative terms which are reflected in the 36 country REER which is at 123. The CNHINR has dropped 6.5% from its peak of 12.20 in March to 11.39 currently. The reason why RBI would have let the Rupee appreciate against the Yuan could have been to keep imported inflation in check at a time when food and fuel inflation are already high.

EUR/USD

The EURUSD pair finally left its consolidating phase after falling to a multi-year low of 1.0350. It closed the week a handful of pips above 1.0400 figures. The collapse took place on Thursday, following the release of US inflation figures the day before. The news that Finland is likely to apply for NATO membership in a matter of days and Russia's statement that it would take retaliatory steps if Finland joined the NATO, severely impacted the euro. Also, Ukraine's halting of Russia's gas flows also brought in the fear of higher inflation in the Eurozone. The outlook still remains tilted towards the bearish, in response to dollar dynamics, geopolitical concerns, and the Fed-ECB divergence. Multiple ECB officials stated that they would be comfortable hiking rates right after finishing the massive bond-buying program known as APP in July. The focus would be on the GDP, ECB President Lagarde's speech, and CPI data expected to be released later in the week.

Bank of England interest rate could hit 4% or more, ex-policymakers warn

GBP/USD

The Bank of England’s policy announcements-led sell-off extended into a second week, with cable making fresh multi-month lows almost each new trading day. The UK economy contracted 0.1% MoM in March while recording a meager 0.8% expansion in Q1 2022, exacerbating the pain in the pound. The GBPUSD pair sold off aggressively, as the macroeconomic, as well as, monetary policy divergence between the UK and US returned to the fore. Further, markets witnessed a classic risk-off profile that favored the ultimate safe-haven, the dollar, in times of mounting growth worries. A relief rally seeped into the final trading day of the week, offering a temporary reprieve to GBP bulls, as the dollar corrected amid an improving mood. Heading into a new week, the cable is looking to find a bottom, with all eyes on the US Retail Sales and UK inflation data. The pessimism surrounding Brexit and the UK's economic fears are negatives that are expected to keep the cable under pressure in the week ahead.

Global markets in recovery mode, the dollar index continues to climb

Dollar Index

The dollar shed some ground after hitting fresh peaks of 105 on Friday. The recent sharp move higher was exclusively in response to the abrupt re-emergence of the risk aversion. The index came under some selling pressure in the last trading session against the backdrop of a mild improvement in the risk-associated universe. Supporting the dollar appeared investors’ expectations of a tighter rate path by the Federal Reserve and its correlation to yields, the current elevated inflation narrative, and the solid health of the labour market. On the negative for the dollar turn up the incipient speculation of a “hard landing” of the US economy as a result of the Fed’s more aggressive normalization. The dollar index is expected to trade with a neutral to bullish bias on the back of a stronger dollar.

Domestic and global equities

Domestic equities

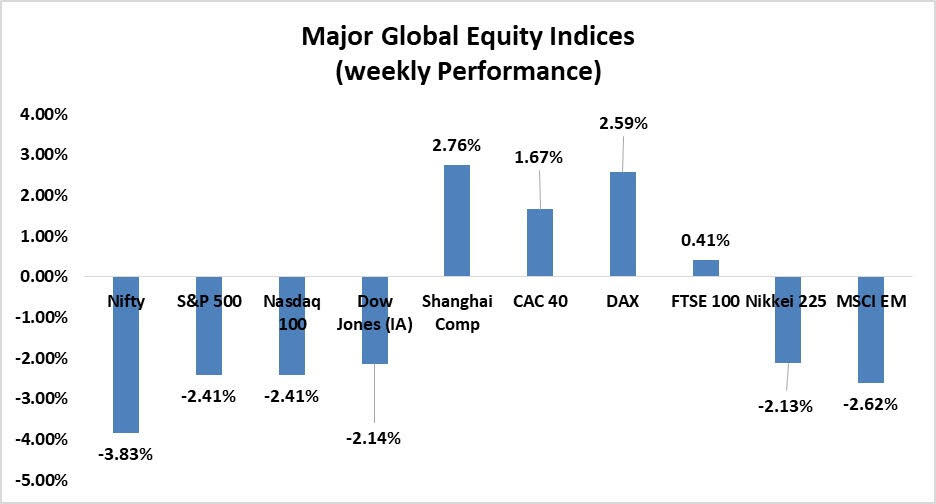

The India Nifty 50 traded in the range of 15,738- 16,404 over the week and closed with a downside. Auto, pharma, and FMCG were the only ones who remained on the positive side over the week rest sectors remained under pressure. Indian markets have corrected in the last few weeks due to rising global yields to counter inflation. A surprise hike by the RBI also contributed to this recent correction. Some small corrections further can’t be ruled out and volatility may remain at elevated levels due to tightening liquidity and earning season.

Global equities

US Stocks recorded another week of losses, as investors appeared to grow increasingly skeptical that the Federal Reserve will be able to achieve a “soft landing” for the economy by raising rates enough to tame inflation without causing a recession. Shares in Europe rebounded from earlier weakness to finish higher, despite ongoing concerns about inflation, tightening monetary policy, and the economic outlook. Japan’s stock markets fell over the week, as expectations that the U.S. Federal Reserve would aggressively tighten monetary policy, concerns about slowing global growth, and the economic implications of the war between Russia and Ukraine continued to weigh on risk appetite.

Domestic and global bonds

Domestic bonds

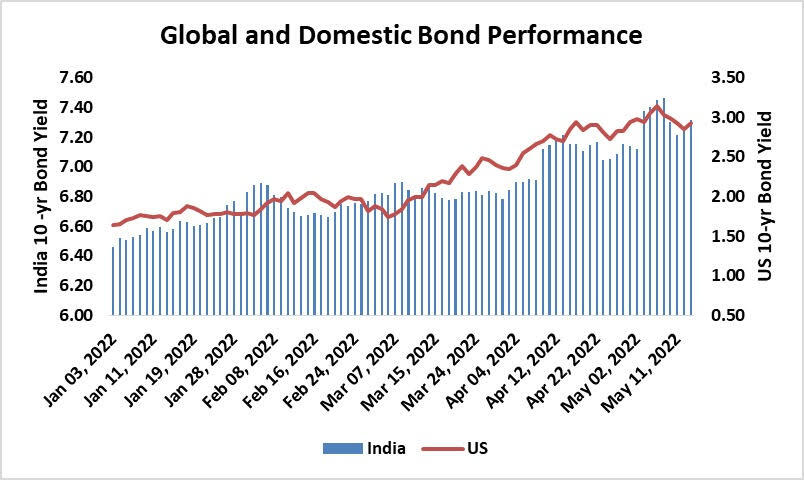

The yield on the domestic 10-year benchmark bond yield declined initially during the week, amid speculation that the Reserve Bank of India may soon buy debt to cap surging yields. However, later in the week, the bonds gave up the initial gains as the yields continued to move north. The 10-year government bond yield rose after India's consumer price inflation hit a nearly eight-year high, suggesting faster tightening by the Reserve Bank of India. Higher crude oil prices and US treasury yields also weighed on domestic bonds. The India 10-year benchmark closed the last trading session at 7.318 levels. the bond market is expected to remain under pressure on the back of high crude prices, elevated domestic inflation, and FII outflows.

Global bonds

The 10-year U.S. Treasury yield slipped below 3% after a release of key inflation data showed a faster-than-expected rise in prices. Initially, during the week, investors appeared to have rotated out of stocks and into Treasury in search of a safe haven, as persistently high inflation data has fueled recession fears. However, later in the week, the U.S. Treasury yields jumped, as investors sold out of government bonds and looked to move back into stock markets. The yield on the benchmark 10-year Treasury note surged to close the week at 2.93%.

Monthly FPI net investments

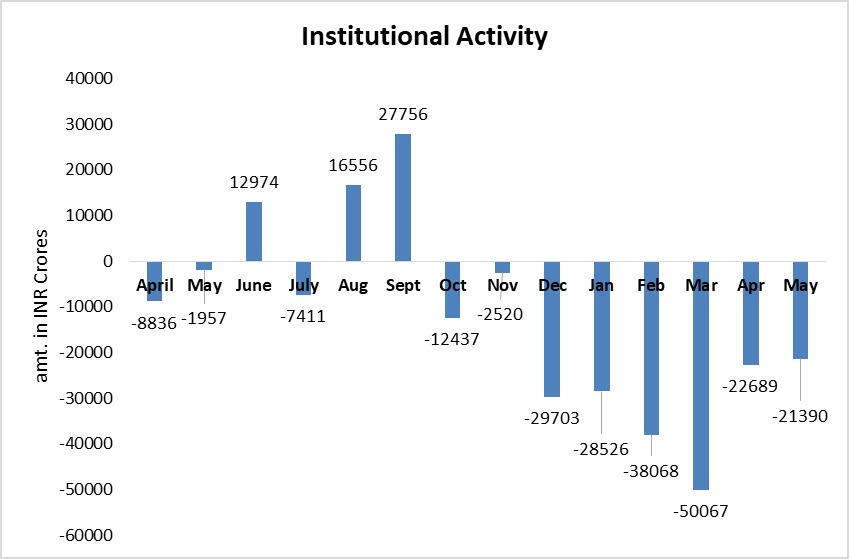

Over the past eight months, foreign institutional investors have embarked on their largest selling spree in Indian equities since the global financial crisis of 2008-09. The outflow is expected to continue in the week ahead due to the strengthening of dollars, aggressive rate hike expectation by the Federal Reserve, elevated global inflation, and other global cues which is making the emerging market less attractive compared to the US. Foreign Institutional Investors have net sold Indian equities every single month since October 2022. It is no secret that global factors are not exactly conducive for bulls to dominate stock markets at the current juncture. A host of central banks, including that of the world’s largest economy, have embarked on an aggressive monetary tightening cycle, implying tighter financial conditions the world over. The net outflow to date in the May month from equity and debt combined stood at INR -21390 crores.

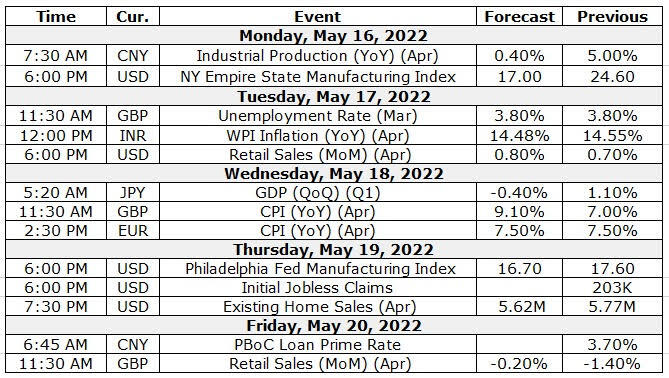

Macro-economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.