How much longer can the Trump reflation trade go on?

Outlook:

We get some useful data today, including Case-Shiller house prices and the prelim Conference Board consumer confidence index. The big one is the Q4 GDP revision from 1.9% to an expected 2.1%, according to the consensus at Econoday.com. This will take some of the curse off the weak Q4 from Q3's splendid 3.5%.

And going forward to Q1, the Atlanta Fed GDPNow model has 2.5% as of yesterday from 2.4% on Feb 16. The New York Fed has 3.1% for Q1 as of last Friday. Yesterday's Credit Suisse GDP forecast for the 2017 year—flattish around 2%--could be overly pessimistic.

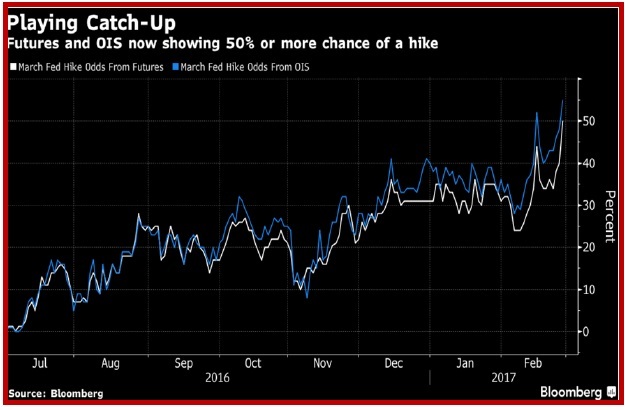

Steady growth and expectations of rising growth are essential to the strong dollar scenario, with or without new policy initiatives. Growth (and the assumption of rising inflation that should accompany growth) are essential for the Fed to sell the "Yes, March" bill of goods, too. For some reason nobody can identify, "Yes, March" became more likely in a single day. Bloomberg reports its analysis of Fed funds futures puts the odds of March up 10 points to 50% yesterday. Swaps concur.

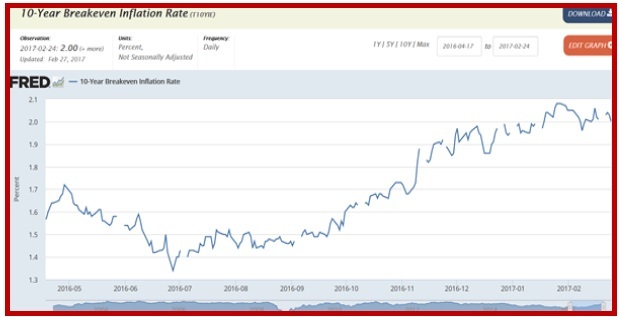

A probability of 50% is still not a dead cert. Dallas Fed Kaplan said the FOMC should raise rates "sooner rather than later" and to hell with market expectations. Remember that chart yesterday showing the Fed has never hiked when the market had not built it in. Blackrock's Rosenberg, who knows a hawk from a handsaw, says we could be on the cusp of a genuine rise in inflation. Tomorrow we get the PCE price index, the Fed's preferred measure, and it could hit the 2% target, according to a Bloomberg survey. It would be the first time at 2% since 2012. Confirming this expectation is the breakeven rate (nominal minus TIPS), hitting 2.09% recently (but 2.0% as of last Friday, according to the St. Louis Fed).

We get another three Fed speakers in a single day today (Philadelphia Harker, San Francisco Williams and St. Louis Bullard). As noted yesterday, normally the regional Fed presidents do not coordinate their comments but if the Fed needs the market to expect "Yes, March," maybe Yellen/Fischer made a few behind-the-scenes phone calls. Rising expectations of "Yes, March" plus renewed hopes of a bold fiscal stimulus from Trump tonight combined to push yields upward and the dollar along with them, although not in what you can name a decisive manner.

Case in point—yesterday in the morning, yields and the dollar slipped downward on the White House deferring the tax plan until the Obamacare health care replacement plan is figured out and priced. They recovered on later announcement of the "bold agenda" to come today. In the end, what we know of the bold plan is "long on rhetoric and short on details," as Market News puts it.

Market players, who see themselves as the pinnacle of high finance, as the slaves of the Trump PR machine.

While Trump may appear clownish—and former Pres Bush II positively credible and dignified (who would have thought it?)—the sad fact remains that among the committed Trumpies, his popularity is holding up very well. Polls indicate an approval rating of 88-89% among Trump voters, and a disapproval rating of about the same among opponents. This may not have anything to do with the response to tonight's TV show. Financial analysts and traders are supposed to leave their political bias at the door and make decisions on what the crowd is likely to do in response to the Trump initiatives. One such judgment in the past has been that while Congress may shut down the government, actual default is simply unthinkable. The dollar did not crash.

The question now is how much longer the Trump reflation trade can go on. The FT's Plender makes a salient point when he says US equities are reflecting momentum, not valuation. And "The more direct problem for investors in equities and bonds is simply that the current historically high level of markets ensures low future returns. In their annual survey of investment returns for Credit Suisse Elroy Dimson, Paul Marsh and Mike Staunton of the London Business School provide convincing evidence that low real interest rates mean a low return world for both equities and bonds. Their estimate for the long-run equity risk premium over the US Treasury bill return is 3-3.5 per cent, which is lower than many have assumed in recent decades. So be warned that the Trump reflation trade is clearly about momentum, not value."

This means that at some point, those who must remain invested in something (i.e., a cap on cash) need to get out of equities and into something else. Some like emerging markets, although here again, managers often face from above caps. If they move into bonds, prices go up and yields go down. From the perspective of forecasting the dollar, we need to weigh whether a surge into bonds is bigger than the pull of higher yields from Fed rate hikes. At this point it looks like the large and growing bond positions could easily overwhelm the Fed, March or not. It's a see-saw at the moment.

What will be the Trump effect tonight? We can reasonably assume Trump likes the stock market rally and sees it as validation of himself. You can just imagine him asking advisors what he can say to keep it going. The tax plan and infrastructure splash-out may be deferred, but Trump can make promises about other kinds of spending that will push some sectors higher, as in the $54 billion in new military spending. Never mind that it's almost certainly not needed. Smarter spending, maybe, not more. But never mind. Trump just needs to keep optimism going. And never mind that some in Congress have already done the homework on deficits and the debt, and want something other than unfunded spending. Knowing how Trump operates, he is going to tell them "figure it out."

And therein lies the risk. Trump is careless and reckless. He is also undermanned and lacks the staff expertise to present anything resembling a true "plan." He will throw out shiny new things to distract attention from the absence of serious and credible initiatives. We will get a lot of adjectives ("phenomenal") but little substance. We can pretty much take it for granted that beneficiaries will be military contractors, oil companies, and Wall Street.

The problem with no substance is that it lets imagination runs wild. Roger Cohen in the NY Times today rants about how and why people are so angry. Bottom line—they think they are being cheated. And so they elected Trump. "People ask, and it's a reasonable question, why everyone's so angry, why they're voting against their own-self-interest, even electing hucksters like Donald Trump who never really had anything but mean little thoughts and now says he'll clean the swamp as he replenishes it daily.

"They ask what the deal is when job numbers are pretty good and Warren Buffett, no less, says the American economy will continue to perform its wealth-making miracle and the world has known a solid quotient of peace for way longer than is usual — and yet there is enough anger for a shallow con man to get elected who says he'll make America great again with ‘one of the greatest military buildups in American history.'

"What Trump knows about history (or for that matter the Constitution) would not fill a Post-it note. Just for the record, massive military buildups tend to precede a war. My bet would be with Iran, possibly before the midterms. But that's not the issue here, although it's scary."

This is possibly hysterical overstatement. But who doesn't worry that Trump intends to start a war so he can win it?

Trump said when he was in school, the US always won its wars. He failed to notice Korea and Vietnam, which he escaped with probably fictitious bone spurs. It's a sign of the feeble-mindedness of the libs that they add the War of 1812 to those we lost.

Net-net, we say the public (if not Congress) wants to be conned. The Trump speech will be well received by the markets. Let's see if Fed funds futures hold up, though.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.18 | SHORT USD | 01/05/17 | WEAK | 115.93 | 0.60% |

| GBP/USD | 1.2441 | LONG GBP | 01/24/17 | WEAK | 1.2451 | -0.08% |

| EUR/USD | 1.0604 | LONG EURO | 01/10/17 | WEAK | 1.0587 | 0.37% |

| EUR/JPY | 118.95 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 2.15% |

| EUR/GBP | 0.8522 | LONG EURO | 02/06/17 | WEAK | 0.8605 | -0.38% |

| USD/CHF | 1.0044 | SHORT USD | 01/05/17 | WEAK | 1.0113 | 0.20% |

| USD/CAD | 1.3171 | SHORT USD | 01/05/17 | STRONG | 1.3253 | -0.02% |

| NZD/USD | 0.7197 | LONG NZD | 01/10/17 | STRONG | 0.7014 | -0.17% |

| AUD/USD | 0.7673 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.49% |

| AUD/JPY | 86.08 | LONG AUD | 10/06/16 | WEAK | 78.48 | 0.19% |

| USD/MXN | 19.9389 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 4.19% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat