How, exactly, does the Fed intend to implement the new policy?

Outlook:

We misjudged the Powell event. We thought that if it happened, it wouldn’t be anything new. And it wasn’t anything new, but the market wanted a knee-jerk anyway.

The adoption of average inflation targeting was widely expected but not built in as much as it should have been. The policy contains nothing surprising or new, and should not have caused such a big jump in currencies and yields, which implies that jumps will be short-lived. Rejection of negative rates (and presumably curve control) was also expected. Weakening the announcement even more is the absence of tools. How, exactly, does the Fed intend to implement the new policy? This is a bit like former TreasSec Rubin saying “a strong dollar is in the US’ best interests” as a “policy” statement but having no ability or means to take any action to push the dollar stronger. However, let’s not forget that the “strong dollar, best interests” mantra worked for a very ling time.

The Fed can only pray the same thing happens here and now with its new top priority on employment. That’s the only “new” thing--underweighting inflation and overweighting employment from a 50-50 mix. If the Fed thinks the inflation-obsessed are going to take it lying down, the Fed is delusional. We already see reference to the 10-year breakeven (inflation adjusted minus actual). See the chart from the St. Louis Fed. As of yesterday, the market expects inflation at 1.73% in 10 years’ time. It was 1.62% on Aug 20 (and 0.50% at the low on March 19). Inflation today is about 1% and with a target of 2%, today’s 1.73% in not anything to worry about. Never mind—inflation fear-mongers will be out in force starting today.

Note, however, that the expected inflation in the TIPS is very different from the inflation reported by the other government agencies, and the Fed’s focus on the PCE deflator in particular. Oh, rats, here we go again differentiating among various inflation measures. We know an otherwise very smart financial analyst who goes solely by the price of milk and eggs in his local supermarket. And sometimes he is right is his inflation forecasts.

Today the news plate contains preliminary July goods trade, inventories, the University of Michigan consumer confidence, and personal income and spending, with its embedded deflator. The headline PCE deflator is expected to rise to 1.0% from 0.8%, and the core (ex food and energy) is expected to rise to 1.2% from 0.9%.

The inflation hawks may very well jump on that small rise in the PCE deflator as a reason to sell the dollar, because the real rate is now lower unless the nominal rate rises proportionately. Which is what it may be doing. But we are not sure this way of looking at things is right. Yes, the yield differential needs to be judged in the context of real rates and not just nominals, but is that the ruling principle under current conditions?

First we have to look at growth. We tend to assume that growth brings inflation with it, but the textbooks point out this is a workable hypothesis only if growth stresses capacity. Capacity is weird today just about everywhere, obviously very high because of the massive slowdown and not everyone having a clear idea of whether growth will push against a capacity ceiling come next year.

Let’s say June 2021 is the real end of the pandemic (for argument’s sake). A zippy just-in-time capital spending program can increase capacity before inflation can get a grip. A wise tax plan could promote precisely this outcome, although here we go again on what a central bank can do and what the fiscal authorities should do. To predict future inflation between the countries is super-complicated. To look at conditions today and talk about what they mean for upcoming inflation data may seem necessary to some, but unlikely to produce more than a wild guess and not a bet anyone should put real money on.

In the end, the Fed has ruled out negative rates while the other major central banks have not, and note that at Jackson Hole, the ECB’s Lane wondered out loud if more QE is not warranted. The US has a yield advantage on both nominal and real differentials, and that is not going to change anytime soon. We continue to think that knee-jerks aside, the dollar retains the advantage.

There are a number of flies in this ointment, however. One of them is that in the absence of a new fiscal recovery bill, still awaiting Senate agreement, the outlook for US growth gets a lot dimmer. More importantly, uncertainty rises. Whether it rises to a negative risk-off shock remains to be seen. Then there’s the Mismanager-in-Chief biding his time before attacking China again with some outrageous demand or insult. This went on hold when the White House lackies claimed everything is hunky-dory in Phase One, but it can’t last. Waiting for that shoe to drop raises the outlook for a risk-off event, too.

We can see why so many analysts like the idea of dollar devaluation as a conventional “classic” response to super-dovishness, excess money supply, etc., but these are hardly conventional times.

Politics: Trump ended the Republican convention with hardly any mention of the pandemic, a bunch of lies about the economy and no mention of the social crisis today, income inequality and white cops shooting black men. The whole thing was a disgrace, including the illegal use of the White House to hold the “convention,” not to mention the big crowds close together and hardly anyone wearing a mask. But as with the Dems’ convention, it’s not worth talking about because the Plubs didn’t watch the Dems and the Dems didn’t watch the Plubs. Everyone is preaching to his own choir.

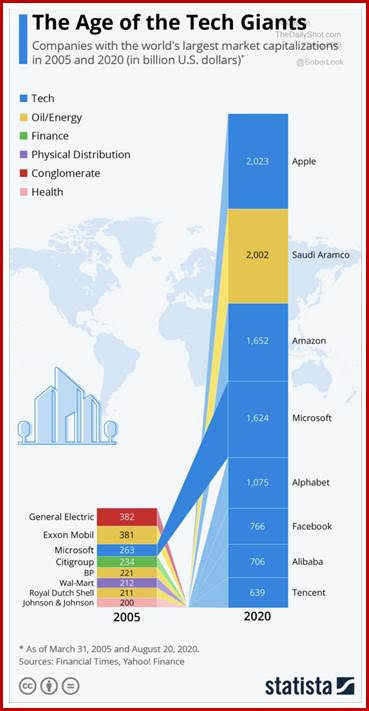

Tidbit: See the chart from The Daily Shot. What’s wrong with this picture?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat