GDPNow forecast for 2022 Q3 barely positive despite New Home Sales surprise

New home sales for August were a major surprise, but the Atlanta Fed GDP forecast didn't budge.

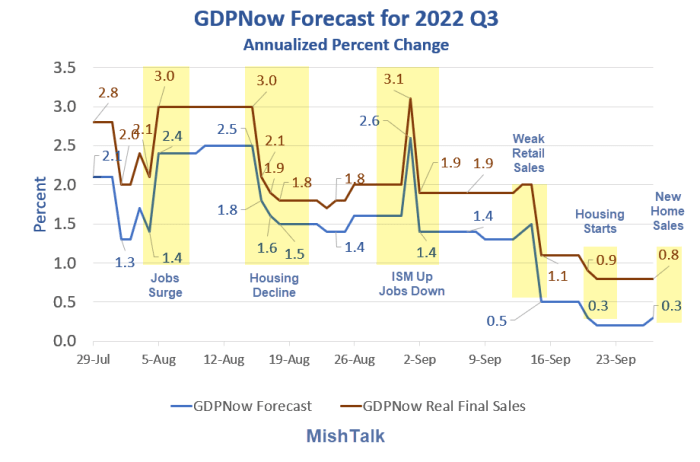

Please consider the September 20 update to the GDPNow Forecast for Q3 GDP.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 0.3 percent on September 27, unchanged from September 20 after rounding. After releases from the National Association of Realtors and the US Census Bureau, the nowcast of third-quarter gross private domestic investment growth decreased from -7.4 percent to -7.6 percent.

The up-down, up-down pattern of the GDPNow forecasts finally collapsed into a down-down-down pattern on weak jobs followed by weak retail sales. The forecast then fell slightly despite a seemingly strong new residential construction report, then very strong new home sales.

Base forecast vs real final sales

The real final sales (RFS) number is the one to watch, not baseline GDP. RFS ignores changes in inventories which net to zero over time.

RFS was positive in the second quarter and April had a big retail sales splurge in spending.

Things fell apart in May and that's when I believe recession started.

This is a good reason to ignore the talk of two quarters of declining GDP being a recession.

Spotlight on current real final sales (RFS) estimate

- RFS Total: 0.8 Percent (Lead Chart).

- RFS Domestic: -0.2 Percent.

- RFS Private Domestic: -0.7 Percent.

The real final sales RFS Total is the bottom line estimate for the economy. The rest is inventory adjustment that nets to zero over time.

Note that government spending and exports (military exports?) are propping up the numbers.

Real private sales to private domestic purchasers is negative 0.6 percent.

On September 20, I noted GDPNow Forecast for 2022 Q3 Barely Positive Following Housing Starts Report

The seemingly strong new residential construction report for August had a negative impact on the Atlanta Fed GDP forecast for the third quarter of 2022.

Today we see a little reaction in the GDPNow model despite New Home Sales Jump an Astonishing 28 Percent in August

What's going on?

- Existing home sales are far bigger and thus more important.

- August sales will start construction with a delay.

- For whatever reason, the numbers may not hove been a huge surprise to the model.

- At the beginning of August, mortgage rates dipped from over 6 percent to 5 percent. Rates did not stay near 5 percent for long, but perhaps thousands of people bought the dip.

Some combination of the above is in play.

Regarding point 3, it's not the numbers that matter but rather what the data does vs what the model expects.

I was very surprised by the actual new home sales numbers but was not at all surprised by the GDPNow reaction being aware of points 1-3 for a long time.

Recession off?

Following the new home sales report a friend asked if the recession was called off.

It hasn't been, and the Atlanta Fed estimate is proof enough.

The quarter ends in three days but there is still over a month's worth of data that hasn't been published. The big remaining reports are retail sales and existing home sales.

Revisions to these housing reports are also in play. Revisions have generally been very negative and the level of confidence in the initial numbers is not that high.

For example, here is a statement from the commerce department on new home sales: New home sales were "28.8 percent (±18.3 percent) above the revised July rate of 532,000."

±18.3 percent is one heck of a lot of leeway.

I still expect a third consecutive quarter of negative GDP.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc