GBP/USD Weekly Forecast: Slipping or plunging, the direction is down

- Volatility has been compounded by several fundamental uncertainties.

- COVID-19 lockdowns, Brexit and resurgent dollar have battered pound.

- Risk-aversion is driving traders from the sterling.

- FXStreet forecast poll suggests near-term GBP/USD decline

Sterling has lost all of its summer bounce and is threatening to break back into its immediate post-pandemic range of 1.2300-1.2700. Several factors have withered the appeal of the UK currency but the primary cause has been the risk-avoidance resurgence of the US dollar as the continuing economic impact of COVID-19 makes the August and September sterling optimism outdated.

The dollar retreat in the last two months was more a relief reaction to the declining infection rates than an endorsement of the UK and Eurozone economies. Unfortunately what goes down also goes up.

Central banks around the world are on hold. The Federal Reserve extension of zero rate guidance one more year to the end of 2023 did not weaken the dollar because it simply acknowledged what is the standard practice. The Bank of England’s recent pushback on negative rates was equally unproductive in supporting the pound because it reiterates the bank’s long-standing policy.

The return of limited economic closures in the UK from rising COVID-19 cases and the rancorous Brexit talks are the major domestic weights on the pound. Neither is headed for a quick solution and they will continue to exert negative pressure.

Predictions of fast-rising unemployment from the Bank of England and the Office for Budget Responsibility "Don't make for good reading," Chancellor of the Exchequer Rishi Sunak told reporters. Notwithstanding the limited rise of unemployment from 3.9% to 4.1% in the three months to July, the BOE has predicted 7.5% by year-end if there was no replacement for the current furlough program.

The US election has had little impact on currency markets in general or the sterling in particular. The tightening presidential race will see its first debate between Donald Trump and Joe Biden on Wednesday and though the US economy will be a topic the rhetoric will not travel far from the stage in Cleveland, Ohio.

GBP/USD Outlook

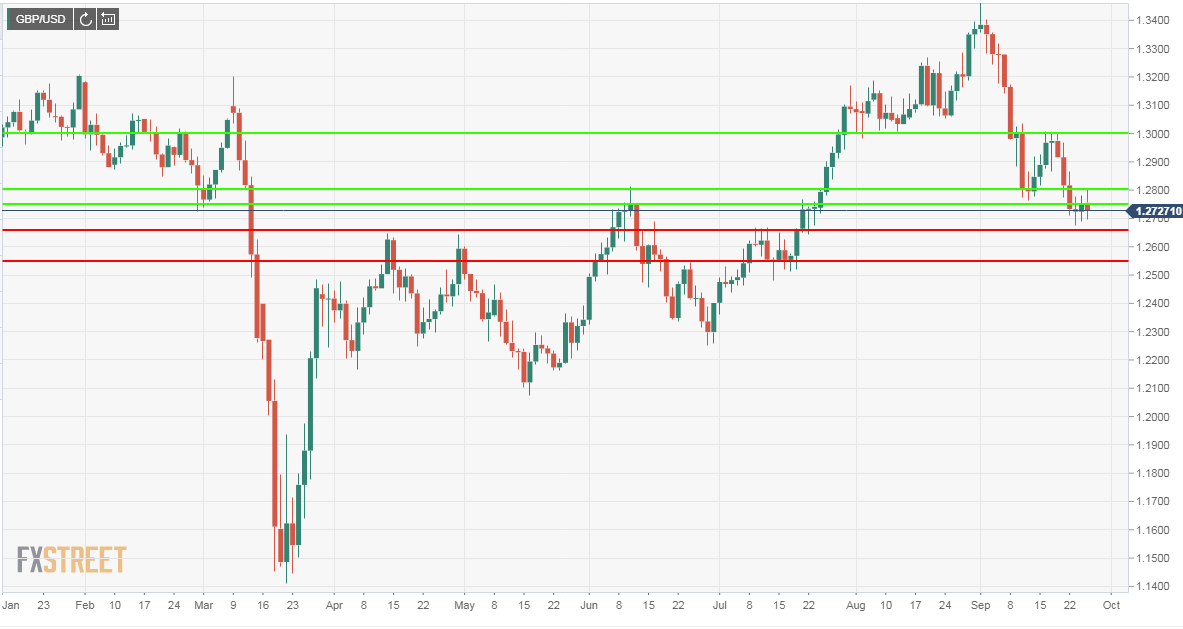

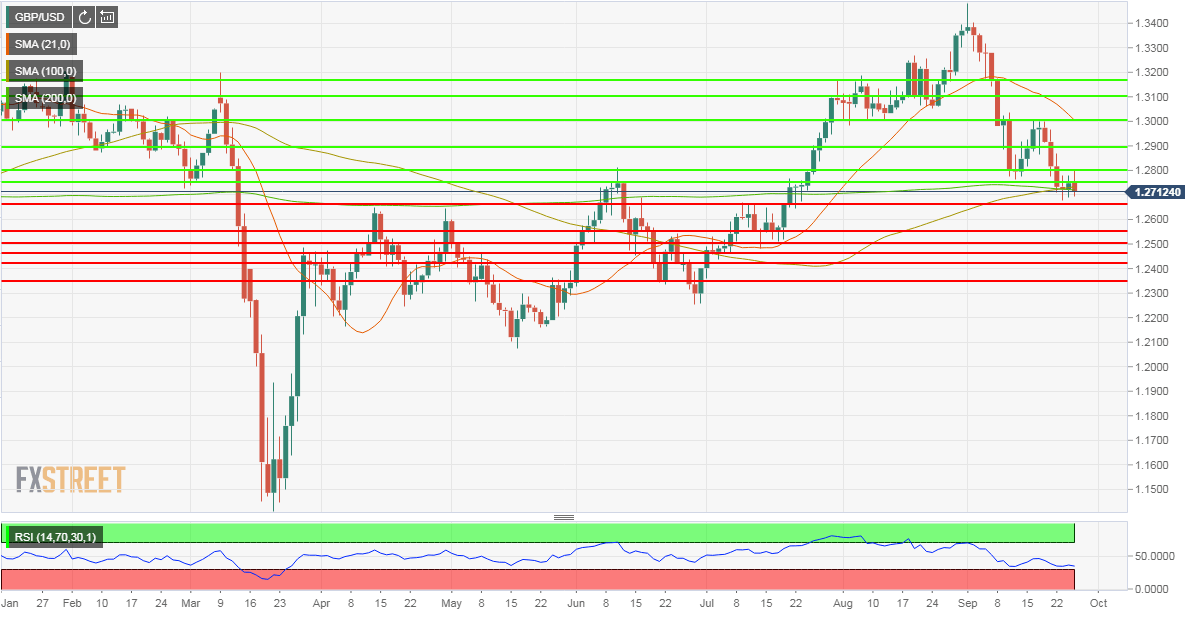

The rapid descent from the September high, sterling closed at 1.3385 on the 1st of the month, and the sharp two-figure drop at 1.3000, once support now tested resistance, argue for a lower pound.

Fundamentally the UK economy has largely recovered from the lockdowns but the currency is not trading on its economic prowess either vis-a-vis the dollar or the euro, but on the assessment for future progress. The reversion to closures to control the pandemic and Brexit talks will undermine any improvement in the economy.

The two-month sojourn above 1.3000 was closed out with three steep descents on September 7, 8 and 10 which brought the pound from 1.3280 to 1.2805. The range on September 10 of 1.2773 to 1.3035 defined markets for the next eight sessions and when the lower limit was breached on September 22, it then became new resistance and has not been crossed since.

The progression of sharp drops followed by new resistance line at the base of the decline is typical for a declining currency. Though the area below 1.2700 has a full complement of support lines from five months of trading that should not deter entry.

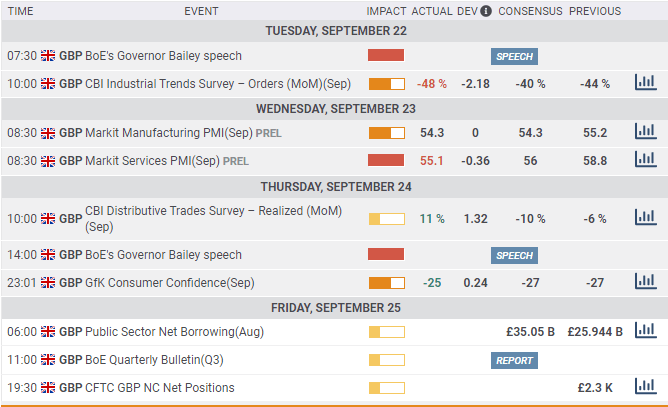

UK and US statistics summary September 21-September 25

Business and consumer sentiment in the UK evinced improved confidence in September.

Markit Economics of London reported its purchasing managers’ indexes at 54.3 for manufacturing, down slightly from August’s 55.2. Services registered 55.1 off from August’s post-lockdown high of 58.8. The service figure missed its 56 forecast and manufacturing matched its prediction. Both readings are above their February pre-pandemic scores of 51.7 and 53.2 respectively.

Consumer sentiment continues to lag its business partner. September confidence from GfK was -25, a bit better than the -27 forecast and August score but far from the February rating of -7. The low was -34 in April.

In the US Fed Chairman Powell and Treasury Secretary Mnuchin testified in Congress three times, calling for continued government support for the economy and a new stimulus bill. It is unclear whether the Democrats and Republicans, in the grip of a presidential campaign, will be able to bring themselves to compromise.

August durable goods order reflected the fading economic support coming in at 0.4% on a 1.5% forecast, though the July number was revised to 11.7% from 11.2%. Non-defense capital goods, the business investment proxy surprised at 1.8%, more than tripling its 0.5% estimate and its July score was revised to 2.5% from 1.9%.

Markit’s preliminary September PMIs were as advertised, 53.5 in manufacturing on a 53.2 forecast and 53.1 in August. The service sector registered 54.6, under its 54.7 prediction and August’s 55.

Jobless claims disappointed with 870,000 filings in the latest week, over the 843,000 prediction and 866,000 in the previous week.

The layoff of nearly one million workers each week is the main negative note for the US economy, showing that some areas of the economy continue to contract.

UK statistics September 21-September 25

US statistics September 21-September 25

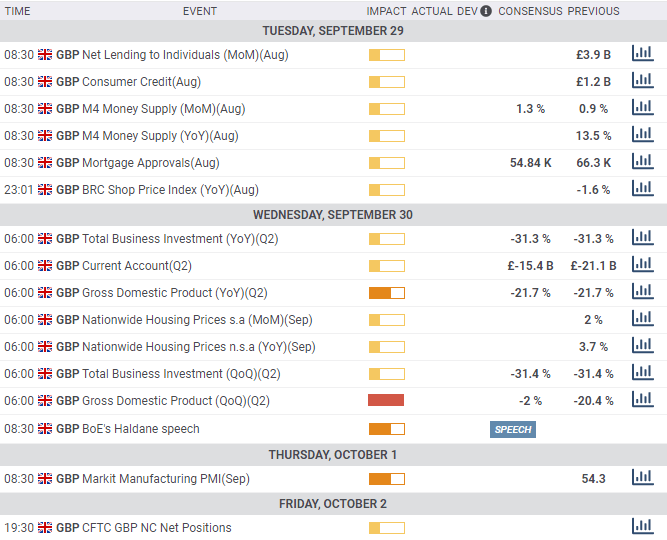

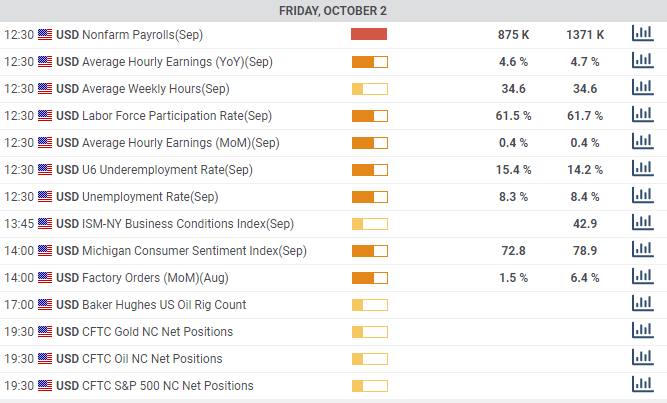

UK and US statistics summary September 28-October 2

The UK produces data on second-quarter GDP and business investment, mortgages and consumer credit for August and manufacturing PMI and housing prices in September. Of these only the September numbers have potential market impact, particularly the manufacturing figures. The more resiliency the economy can show the better for the pound.

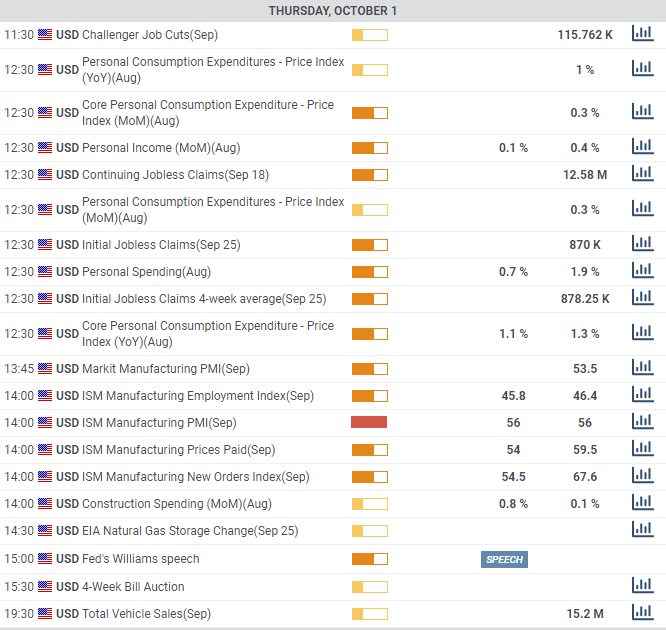

In the US the major news comes from the labor market with the September Nonfarm Payrolls and unemployment data on Friday. Payrolls are expected to drop to 875,000 from 1.371 million in August and the unemployment rate to be largely unchanged at 8.3% from 8.4%.

The recovery of the job market is the main focus for the US economy and the translation is straight forward, better statistics support the dollar and equities. Credit markets are less impacted by the Fed long-term rate hold.

Initial jobless claims are an important secondary data point as the continuing high level of filings undermine confidence in the recovery and tilt the NFP risk lower.

The presidential debate between Donald Trump and Joe Biden on Wednesday, September 30 is not strictly an economic event but any unexpected development or cancellation would roil markets though the specific dollar direction would depend on the circumstances.

Other notable statistics will be the Conference Board Consumer Confidence figures for September, the final revision of second-quarter GDP, Personal Consumption Expenditures and prices for August, ISM manufacturing figures for September and the revision for September's Michigan Consumer Sentiment.

None of these statistics are normally sufficient to provoke markets but the September ISM and the two consumer reading have the most potential.

UK statistics September 28-October 2

US statistics September 28-October 2

GBP/USD technical outlook

The Relative Strength Index is approaching oversold at 34.78 but will not enter that status until the support at 1.2660 is broken. Two moving averages, the 100-day at 1.2734, and 200-day at 1.2720, are in a somewhat unusual situation with both sitting at the market on Friday morning (1.2716. 10:00 am EDT) providing either support or resistance depending on the immediate movement of the currency. In fact, the impact of the averages is very limited as they have already been crossed several times in trading. The 21-day average at 1.3004 coincides with resistance at 1.3000.

The area below 1.2700 is replete with support, a product of five months of trading activity. While the fundamental picture for the sterling points lower it is not as yet a definitive view. The support lines will slow any fall until the fundamental picture is clear.

Resistance: 1.2750; 1.2800; 1.2890; 1.3000; 1.3100; 1.3170

Support: 1.2660; 1.2550; 1.2500; 1.2460; 1.2420; 1.2350

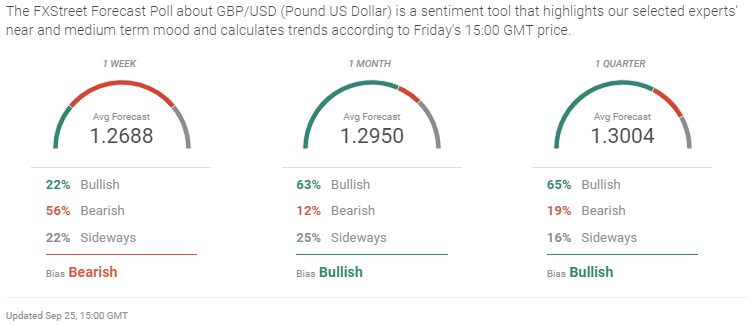

GBP/USD Forecast Poll

he bearish sentiment in the near term Forecast Poll is relatively weak despite its statistical dominance as the forecast of 1.2688 is just north of support at 1.2660. The reversals in the one-month and one-quarter outlook are perhaps justified by the substantial support lines beneath 1.2700 but the fundamental picture is far less sanguine due to Brexit and COVID-19.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.