FX market expects Powell to repeat that it’s time to dial back the aggressiveness

Outlook: Today the important data is the JOLTS report, the ADP forecast of the private sector component of payrolls, and Fed chief Powell’s speech. We also get the Beige Book (for the December 14-15 FOMC), another revision to Q3 GDP, Oct trade balance for goods, and pending home sales. Going into a day of data overload, remember that last week the Atlanta Fed had Q4 GDP at 4.3% and holiday retail sales are excellent.

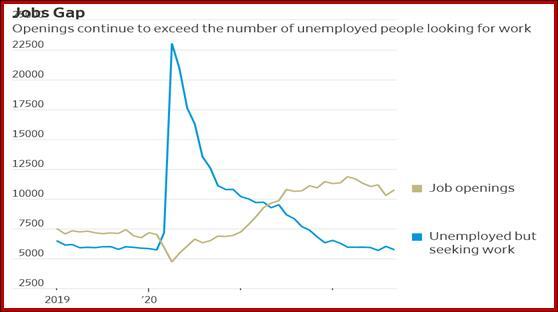

The Jolts report is expected to how ongoing divergence between jobs offered and the workers available to fill them. The space is so wide that even if offerings contract by 450,000 as forecast, the labor shortage will still be obvious and equally obvious, the expectation of rising wages to pull labor in.

The continuation of job growth will be tested with payrolls on Friday, but there is little doubt the Fed will not be getting the conventional response to rate hikes. Chart from the WSJ. As noted before, companies may be exaggerating their offering requirements but at the same time, unemployed may have given up because they don’t qualify due to illiteracy, innumeracy and drug addiction.

Jolts may prepare us for payrolls on Friday, likely 200,000 and unemployment the same 3.7%. Historically, 3.7% is very, very low. While the mainstream worry is about rising wages that feed inflation, we need more information (and not just snippets) about most of the inflation rise having been caused by the supply-side and not demand.

The WSJ reported yesterday that the 10-year Treasury is yielding less than the 2-year note by the largest amount since the 1980s. This means traders think the shorter-term rate is realistic but the longer one is too high because inflation has peaked and rates will be falling over the 10-year holding period. Considering the 10-year is under 4% now, we’d call that a memory from the days when deflation was the problem--and a leap of faith.

The Fed may enjoy the vote of confidence, although it incorporates the idea that when recession hits, the Fed will relent and start cutting–after just having front-loaded four 75 bp hikes. Yesterday St. Louis Fed Bullard repeated the need for hikes that will be “sufficiently restrictive” and we are not there yet. A rate of at least 4.9% will be needed next year.

When Powell speaks today at the Brookings Institute (1:30 pm), he’s likely to say “higher for longer” and it will be interesting to see if those betting on rate cuts in 2023 revise their thinking at all. Everyone always listens to Powell but this time he will have an even bigger audience. To be fair, the EU-harmonized inflation data from Germany and Spain yesterday and the EU today triggered the same bond market response. Nobody seems to share the view that inflation is more entrenched and we will be lucky to get 4% in five years.

So far it look like the FX market expects Powell to repeat that it’s time to dial back the aggressiveness, meaning the 50 bp at the Dec policy meeting that the Feds have been signaling for some time now. This is dollar-negative in some way we can’t grasp and neglecting “higher for longer.” Maybe it’s just short-term thinking. To be fair, high volatility reflects high uncertainty and we have some wild moves not justified by any data or news (why did the CAD collapse yesterday and the dollar crash against the yuan today?).

Tidbit: FX trend-following Commodity Trading Advisors are crushing it. In October,

“According to the SG Trend Index these funds finished the month +0.19%, in spite of suffering two drawdowns above 1% in the first two days of the month. In all, the Index lost ground on nine of the 21 trading days. Perhaps reflecting the more volatile nature of markets during October, the Index had four days of losses over 1% and three days of over 1% gains.

“Year-to-date the Trend Index remains in very healthy condition at +35.84%, the highest return since SG started producing the Index in January 2000. The previous high return for a year was 2003 at +15.75%, while in 2014 the Index was up 15.66%.

“The broader SG CTA Index was +0.45% in October, for +26.68% year-to-date, while short -term traders suffered, the SG Short-Term Traders Index falling 0.35% on the month. It remains, however, comfortably in positive territory at +12.61% year-to-date.”

Bottom line–trend following in FX tends to outperform short-term trading. In Oct, we made 27% in futures and are on track for 24% in November. Year-to-date we are up over 100%.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat