Federal Reserve July Minutes: Tapering is a rate hike

- Minutes of July 27-28 FOMC advance taper discussion.

- Credit market response shows caution, yields stable.

- Equities fall hard on rate fears, dollar gains on safety.

- July Retail Sales and August Consumer Sentiment may delay implementation.

As the Marxists like to say, the taper discussion exhibits false consciousness.

Ok. Perhaps followers of the Leninist creed never considered central bank policy in any other context than as capitalist oppression.

Still, they have a point.

Tapering the Fed’s bond program will not lead to rate hikes in the US. The taper is a rate hike.

Once the Fed makes it plain that it is winding down the bond purchases that have kept US interest rates historically low, the credit market will do the rest. Treasury prices will fall and yields will jump, perhaps sharply, perhaps not. The speed and extent of the rate increases will depend on the success of Fed expectations management.

The economic impact of a taper does not wait for the Fed to adjust its base rate. It is immediate.

Commercial rates that key on the Treasury market, from mortgages to business credit facilities and your next month's Visa card, will follow government yields higher. This has already happened once this year when Treasury rates soared in the first quarter as the credit market assumed, prematurely, that the recovering economy would soon put an end to the Fed’s emergency intervention.

10-year Treasury yield

CNBC

FOMC minutes

The minutes of the July 27-28 Federal Open Market Committee (FOMC) meeting make it clear that the governors are aiming for a reduction in bond purchases before the end of the year. It is also evident that the decision has not been made and that opinions are not uniform.

“Some participants suggested that it would be prudent for the Committee to prepare for starting to reduce its pace of asset purchases relatively soon, in light of the risk that the recent high inflation readings could prove to be more persistent than they had anticipated and because an earlier start to reducing asset purchases would most likely enable additions to securities holdings to be concluded before the Committee judged it appropriate to raise the federal funds rate,” said the FOMC minutes.

In other words these members are concerned about inflation and want the bond program over before the FOMC moves to raise the fed funds rate.

“In contrast, a few other participants suggested that preparations for reducing the pace of asset purchases should encompass the possibility that the reductions might not occur for some time and highlighted the risks that rising COVID-19 cases associated with the spread of the Delta variant could cause delays in returning to work and school and so damp the economic recovery,” noted the minutes in the immediately following paragraph.

In terms or market perception the minutes have told us nothing new.

Federal Reserve Chair Jerome Powell said after the July meeting that the taper discussion had begun.

In fact, it started at the April 27-28 meeting, whose minutes released on May 19 included the following nugget that then excited a bit of market action.

“A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases,” the meeting summary stated.

The Fed is moving to end its bond program. When it does, rates will move substantially higher. The minutes confirm what markets have known for many months.

Market response

Credit markets were blase in response to the minutes. Treasury yields were mixed and little changed with the 10-year, 2-year and 30-year government securities adding or losing about 1 basis point.

2-year Treasury yield

CNBC

10-year Treasury yield

CNBC

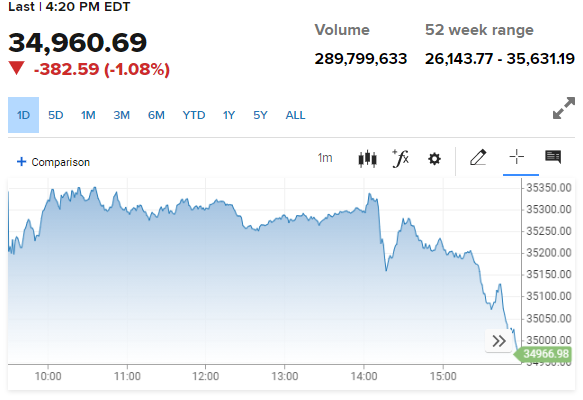

Equities were another story. The Dow closed down 382.59 points, 1.08% to 34,960.69. The S&P 500 lost 1.07%, 47.81 points to 4,400.27 and the NASDAQ stopped 130.27 points, 0.89% to 14,525.91.

Dow

CNBC

The careful preparation for the eventual bond program announcement has been underway since the April 27-28 Fed meeting and its minutes two week later.

That program and higher interest rates are on track and stocks simply acknowledged the inevitable.

The dollar was mixed on Wednesday, higher against the yen, Canadian dollar and Swiss franc but down versus the euro and sterling. The safety trade of the last few sessions faded but may be revived by the deteriorating situation in Afghanistan.

The release of the minutes brought on a flurry of dollar selling which soon petered out.

-637649162843323017.png)

-637649163290502869.png)

Conclusion

The FOMC minutes confirmed the policy outline at the July meeting. Federal Reserve intentions are, or were then, headed for a change, possibly as early as the September 21-22 meeting.

Since then Covid-19 cases have continued to rise in several states, Consumer Sentiment plunged in August below its prior pandemic low and Retail Sales contracted far more than expected in July.

Are these developments enough to delay the Fed’s taper plans?

On that topic the minutes tell us nothing. The Fed balance likely still lies with a taper later this year.

There are, however, five weeks before the September FOMC. If the economic data continues to worsen, if the August payrolls due on September 3, fail to deliver, then as sure as the arrival of fall a few weeks later, the Fed taper will be pushed off into the New Year.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.