Fed might make an announcement, but don't expect the whole hand

Outlook:

The market is sleepy because it nearly the end of July. It's sleepy because the charts are clearly dollar-bearish but the dollar is deeply oversold, so maybe we get one of those tire-some corrections. Or maybe not. Why put on a position under these conditions? Today we get the Conference Board consumer confidence index and the Richmond Fed, yawn.

That pretty much leaves the Fed tomorrow and whatever disgraceful thing the Senate is going to do with the healthcare bill, for which McCain is returning from a hospital bed. The Senate is being asked to vote on a bill nobody has seen. No wonder public approval of Congress is in single digits. On the wider stage, the lack of clarity on economic stimulus has corporate chieftains stymied and indecisive.

There's still a chance the Fed may inspire move movement. This could come from an announcement about the starting date for reducing the balance sheet. So far we know it should begin this year and the Fed intends it to be so quiet and gradual as to be barely noticed, but traders are hungry for fresh meat. After all, there's $2 trillion to get dumped into the private sector.

The latest whisper is that the Fed could begin buying less and declining to roll over as early as next month or September—before the next rate hike, assuming we get one. This is logical—the Fed must want to see the market response to what is, after all, an entirely unprecedented phenomenon. Those who are expecting a specific amount per month will likely be disappointed, though. The Fed doesn't want to show its whole hand. As supply rises, prices should fall, meaning higher yields. We have to assume the Fed and Treasury are working hand-in-hand to substitute one tenor for another to keep the whole curve sane and prevent bulges and disruption. NY Fed chief Dudley will not be getting any sleep until Christmas.

The Fed funds market, in the meanwhile, sees no hike at all this year, leaving the reduction in purchas-es the only policy tool on the table. The CME FedWatch tool shows traders see the probability of a rate hike by year-end at less than 50%. You have to ask yourself how much damage Yellen thinks this is doing to the Fed's credibility rating. To be fair, Yellen cares more about doing the right thing than about the Fed's reputation, but it must be galling to see her comments about inflation undershooting interpreted as just plain dovish and not the nuanced (and obvious) observation she intends.

Despite this bearish environment, oversold is oversold. But to get more than a blip, data will have to extraordinarily good, such as Friday's GDP and embedded PCE inflation. As we wrote yesterday, this is not the forecast. Then there might be something on the fiscal side, but that's not the forecast, either. We might get something on tax reform in early September. Conventional wisdom has it that August can be flat. In practice, this tends not to be true, but never mind. We are all starting to form FX views on what might happen 6-8 weeks out. This is always highly dangerous.

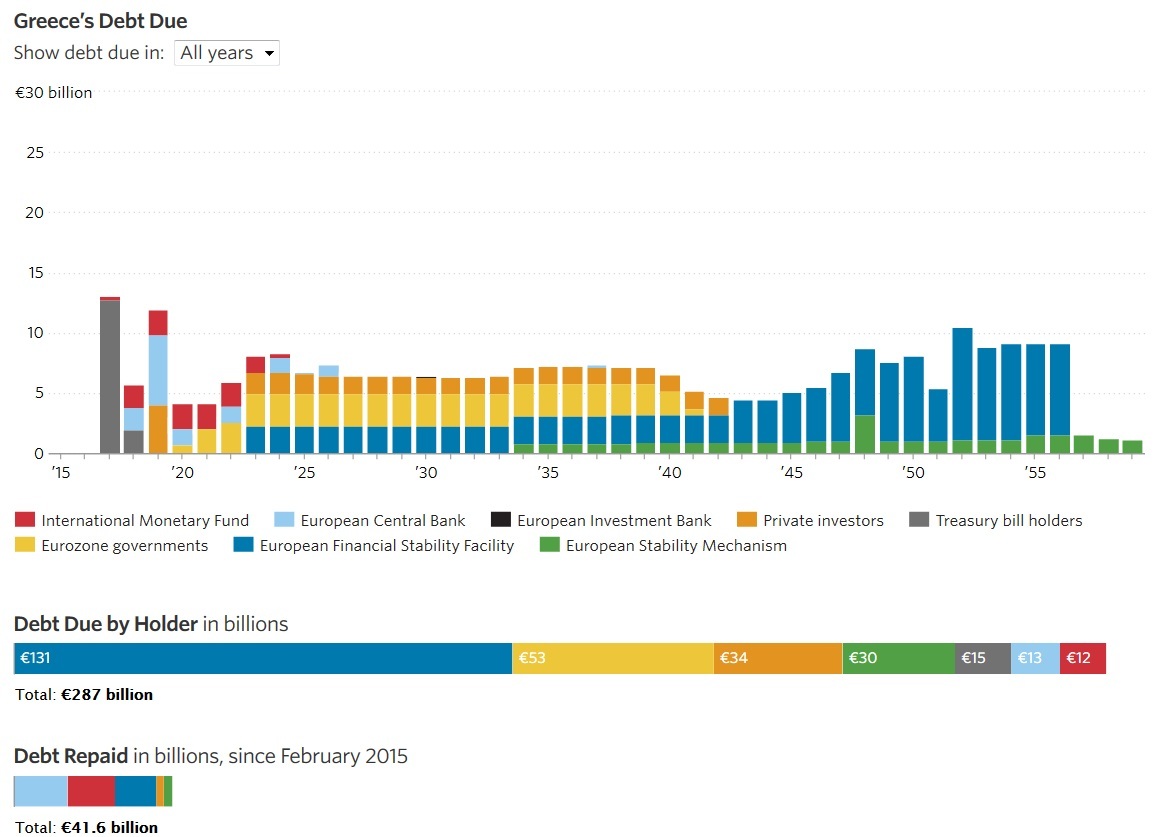

Tidbit: The Greek new bond issue this morning is the first since 2015. It will issue 5-years at a starting yield of about 4.75%. A redemption is included. The WSJ reports redemptions will be about 4% pa for the next 5 years except for 2019, when they are 7%. Greece's return to the market illustrates recovery, but the debt map shows the IMF is right—the burden is unsustainable. See the chart. Greece will be under the crushing weight of debt for another generation. So far, Europe will not relent on debt relief. There are two choices—Greece hunkers down into destitution for decades or a popular revolt triggers another crisis.

On the US political front, Kushner said "I did not collude with Russia and I don't know anyone on the campaign that did." He no doubt believes his statements, just as Trump presumably believes his own lies at the moment he is uttering them. Besides, what does Kushner mean by "collusion?" The Kushner statement was a lawyer-advised public relations statement designed to mislead. To be fair, it was pretty good, although journalists picked it apart word by word and found much to criticize (e.g,, Kushner businesses do not "rely" on Russian funding, not the same thing as not having any).

Attending that one meeting was stupid and breaks election campaign law. So if he's not crooked, that must mean he's stupid. The press names it "playing the ignorance/rookie card." But the guy is a Har-vard grad, even if admittance to Harvard was probably a function of his dad's $2.5 million donation. What's not credible is such haplessness in someone with such a fancy pedigree and so many portfolios. If he's naive, an organizational dunce and an intellectual lightweight, why is he is charge of Middle East peace? And hapless people get played.

Political Tidbit: from essayist Nick Hanauer, who says the mob with pitchforks are already here. "... I find myself in deep disagreement with almost everyone I talk to about Trump and Trumpism. I firmly believe that Trump, by himself, is not the problem. Indeed, the left's maniacal focus on Trump confus-es cause with effect. Yes, Trump is a manifestation of a serious civic sickness. But treating the symp-tom by removing Trump won't cure the disease, even if it temporarily makes us feel better. No, to heal the body politic we must confront the disease itself.

"The real threat to our republic is an alarming breakdown in social cohesion, and the cause of this breakdown is obvious: radical, rising economic inequality, and the anger and anxiety it engenders. The truth is that over the span of decades, American lawmakers have enacted policies that have depressed wages, stoked economic insecurity and exacerbated cultural angst and social dislocation. At the same time, a tiny minority of mostly urban elite have benefitted obscenely from our growing economic, polit-ical and legal power."

Hanauer defends the $15 minimum wage and asserts there are good economic arguments why a higher minimum wage does not kill enterprises. It's a new-fangled model but has some decent data displayed in an original way and we can't say it's crazy.

We may not agree with everything Hanauer says, but consider he wrote the essay two years ago!

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.43 | SHORT USD | 07/19/17 | WEAK | 111.96 | 0.47% |

| GBP/USD | 1.3018 | LONG GBP | 06/28/17 | WEAK | 1.2701 | 2.50% |

| EUR/USD | 1.1655 | LONG EURO | 06/28/17 | STRONG | 1.1218 | 3.90% |

| EUR/JPY | 129.86 | LONG EURO | 06/27/17 | WEAK | 125.73 | 3.28% |

| EUR/GBP | 0.8952 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 5.44% |

| USD/CHF | 0.9474 | SHORT USD | 06/28/17 | WEAK | 0.9675 | 2.08% |

| USD/CAD | 1.2514 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 8.13% |

| NZD/USD | 0.7424 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 5.13% |

| AUD/USD | 0.7924 | LONG AUD | 06/08/17 | WEAK | 0.7548 | 4.98% |

| AUD/JPY | 88.30 | LONG AUD | 06/16/17 | WEAK | 84.65 | 4.31% |

| USD/MXN | 17.7794 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 4.97% |

| USD/BRL | 3.1458 | SHORT USD | 07/17/17 | WEAK | 3.1794 | 1.06% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat