Eurozone industry: is the end of the slump in sight?

Industrial production is likely to have increased in May, but don’t let the numbers fool you. Without an improved trade outlook, manufacturing could be in for a weak second half of the year. As long as employment remains stable, however, an outright eurozone recession remains unlikely.

Industrial production peaked in December 2017 and has been on a declining trend ever since. While the indicator is volatile and plenty of one-off factors have been impacting the industrial sector over the past year and a half, the trend is worrying. Although the reasons behind the downturn remain somewhat of a mystery, as some indicators are still pointing to decent performance, it does seem that weakening global demand and trade uncertainty have had a more significant impact than initially expected. This means more sluggishness could be on the cards. Remarkably though, this contraction in activity has not caused employment to decline. As long as that is the case, an outright eurozone recession remains unlikely.

Export growth is still positive but industries with export exposure are the weakest

Production seems sensitive to weakened global demand and trade uncertainty, not least because the decline in production coincided with falling confidence and the start of significant trade rhetoric from the United States. Still, German exports to the US and China have held up pretty well and national accounts data suggests that eurozone exports of goods are still rising. That said, the growth rate has been slowing markedly - except for a brief pick up in 1Q, which was mainly related to stockpiling in the UK. This adds to mixed views on the downturn in production as it begs the question as to whether external demand can really be the problem when exports are still going up.

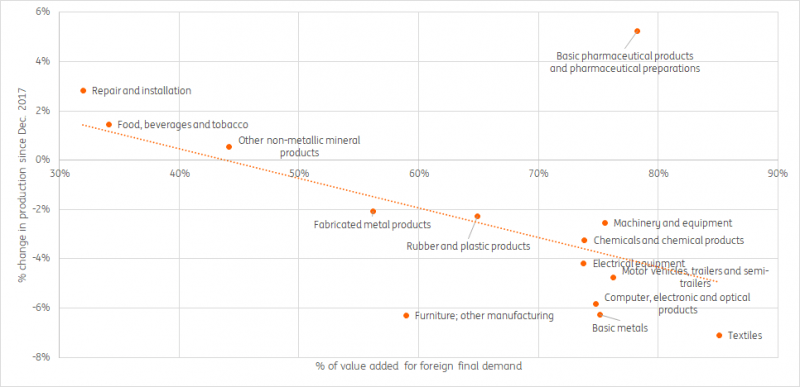

Production has declined most among export dependent industries

It is hard to come to a conclusive answer on this, but it does seem that the external environment plays an important role. Even though export growth is still positive, business surveys have been pointing to a contraction in orders from abroad. Moreover, there is a strong correlation between the percentage that industries produce for foreign final demand and the performance in production since December 2017, with the industries that produce more for foreign final demand doing much worse than the ones producing more for domestic final demand. This indicator includes intermediates that are used in products that are exported, therefore giving a more complete indication of industry sensitivity to weaker external demand.

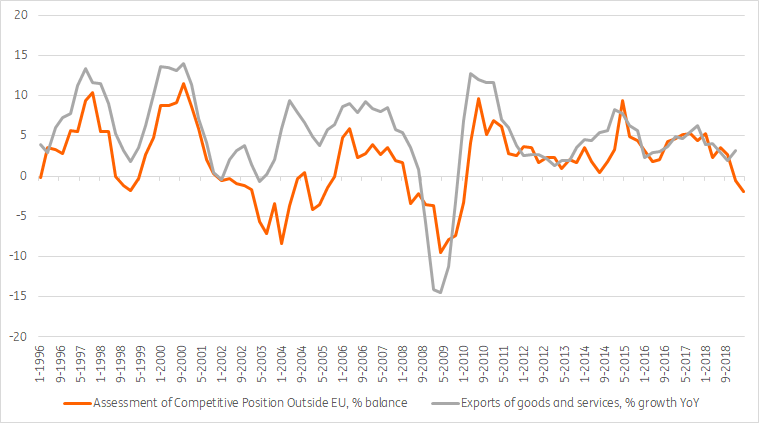

Weaker gross exports could be on the cards over the summer

Source: European Commission, Eurostat, ING Research

While export growth has remained positive up to now, weaker production of intermediates used for exports indicates that weaker gross exports could well be on the cards over the summer months. This view is also supported by the reported deterioration of eurozone companies’ international competitiveness.

While the outlook for industry is clouded by quite a few mixed signals, sluggish global demand and trade concerns are expected to drag on in the months ahead. That means a swift bounce back in manufacturing production is unlikely in the second half of the year and concerns about eurozone GDP growth remain significant at least for the remainder of 2019.

Does this put the eurozone at risk of recession?

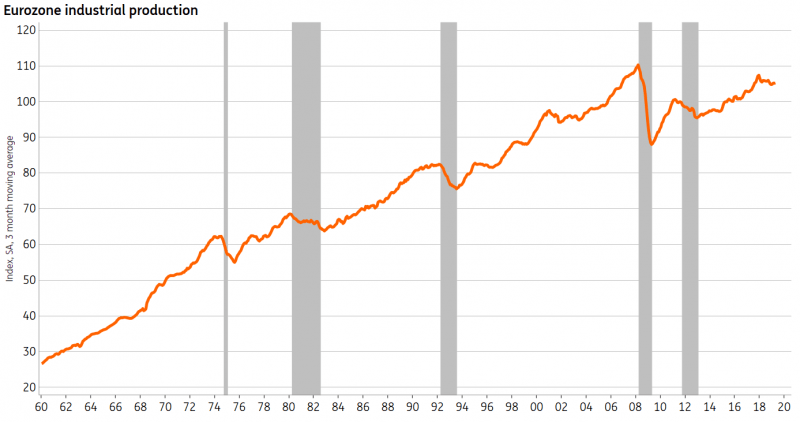

When looking at episodes of declining production, this one stands out. We have not seen a decline this long and this deep without a contraction in GDP since the 1960s, which is the furthest back that the data go. This is except for the early 2000s around the dotcom crisis, which was officially not a eurozone recession although many eurozone countries did experience a recession at the time. Now, while the second half of 2018 saw a marked slowdown in growth, the eurozone has avoided a (technical) recession for now, but the question is, how long can this industrial slump continue without broader repercussions?

Industrial production usually does not decline that long without recession

Source: ECB, CEPR, ING Research Note: shared areas represent recessions

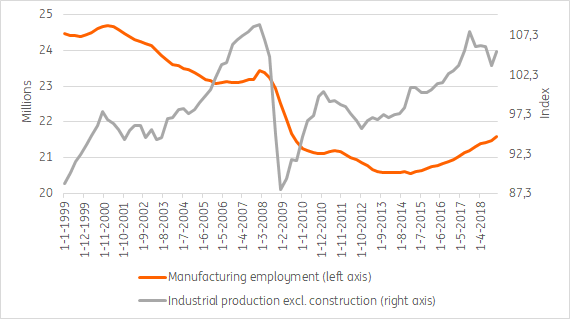

The strong performance of the service sector has kept the eurozone economy from contracting. Remarkably enough, the poor performance of the manufacturing sector has not yet led to a decline in employment growth in the sector. The expansion of the 2000s was marked by a strong decline in manufacturing employment, but the current picture is the reverse of that. Employment in the manufacturing sector continues to grow, thereby supporting household consumption, which in turn mainly benefits the service sector.

Manufacturing employment is still growing despite declining production

Source: Eurostat

There are signs that manufacturing employment could turn down though. For example, businesses indicate that hiring intentions in the manufacturing sector are weakening and in Germany, layoffs have increased while short-term work is returning. Still, as long as overall manufacturing employment continues to grow, the sluggishness in industrial production may well remain relatively contained. The manufacturing job market could, therefore, be key in the coming months to see whether the expansion can hold out amidst industrial sluggishness.

Read the original analysis: Eurozone industry: is the end of the slump in sight?

Author

Bert Colijn

ING Economic and Financial Analysis

Bert Colijn is a Senior Eurozone Economist at ING. He joined the firm in July 2015 and covers the global economy with a specific focus on the Eurozone.