Does a credit crunch necessarily lead to recession and bankruptcies?

Outlook: Today we get inventories, house prices and consumer confidence. House price might be useful, assuming they continue to retreat. Housing is a big chunk of the inflation mix.

There’s a good possibility that the important development today might be Congressional testimony by Michael Barr, the Vice Chair for Supervision at the Fed. In his already leaked statement, Barr will say Silicon Valley was a textbook case of mismanagement. Several press reports over the past few days have it that the state and the Fed had identified the problems and notified Silicon Valley as long ago as last year to fix things and starting in 2019 (before the Fed started hiking).

Barr’s testimony says "The bank did not effectively manage the interest rate risk of those securities or develop effective interest rate risk measurement tools, models, and metrics. At the same time, the bank failed to manage the risks of its liabilities. These liabilities were largely composed of deposits from venture capital firms and the tech sector, which were highly concentrated and could be volatile."

Barr intends to say “SVB’s failure demands a thorough review of what happened, including the Federal Reserve's oversight of the bank. I am committed to ensuring that the Federal Reserve fully accounts for any supervisory or regulatory failings, and that we fully address what went wrong." A report will be due before May 1, which gives Barr the time to pass the buck to some other poor guy. In addition, Barr is going to hint at “new measures” to prevent "isolated banking problems" from developing into systemic risks. This is some kind of required long-term debt management.

Bah. The “isolated banking problems” are already systemic, hence the need for new regs. They consist of huge unhedged bond holdings. We can wonder if any Senators drive Barr down that road. If not, the press is sure to do the job.

As the press is all too willing to point out, the top supervisor himself should have known about Silicon Valley and the others, and should have taken action. Instead he was cogitating and collecting data on crypto, among other issues. To be fair, the FT reports today that Swiss regulators were voicing concerns about the ability to rescue the banking sector (arising from the Credit Suisse problem) as long ago as 2019. There are vast differences between the Swiss and US banking sectors, but not, apparently, between their regulators.

Nobody knows whether there is another banking crisis or failure in the works, but everyone now acknowledges that modern communications and social media make the transmission of a crisis mentality fast as lightning, even faster than 2008. Today’s potential crisis differs from previous ones also because it’s due to the other side of the balance sheet and the public has a hard time understanding that. It can understand bad loans, but it's hard to grasp how a ton of US government bonds can be a bad thing.

The public can also understand that the government let it down and in any other enterprise, Barr would already be out on his ass. A modicum of fear remains that the next one, if there is a next one, will not find a buyer. After all, the FDIC tried–twice–to auction Silicon Valley and nobody showed up. The sale of Silicon Valley didn’t get done until the middle of the night on Sunday night and at a huge cost to the government, and never mind that the FDIC can just hike its fees.

Off on the side, the debate is building about whether the Fed will tighten further or hold the line at current levels with a cut sometime this year. BlackRock says the Fed will stick to its knitting and those expecting a cut are wrong–the top priority is inflation and the Fed acknowledges it’s terribly sticky. The BlackRock statements says “We think the Fed could only deliver the rate cuts priced in by markets if a more serious credit crunch took hold and caused an even deeper recession than we expect.”

Well, yes. And while we tend to bet on the resilience of the US economy, our faith is low in the banking sector’s management and the government’s regulatory capabilities. The probability of another crisis is 50-50 now and the probability of a credit crunch is likely more than 50%. Then the issue becomes whether that famous resilience wins the day. Note that the WSJ is already putting a drop in bank lending in the eurozone on the front page.

Does a credit crunch necessarily lead to recession and bankruptcies? Historically, yes–although perhaps not this time. Reuters repeats the old saw “A credit crunch is when your bank won't lend to you. A credit crisis is when banks won't lend to each other.” This time is unusual in the sense that the Fed has made it clear that it will lend to banks until the cows come home, in both the standard discount window and the new weekly facility. While lending has already slowed in the US, the sharp end of the knife is subprime borrowers, especially consumers trying to buy cars. Fed chief Powell made it completely clear in the press conference that he grasps the recession risk.

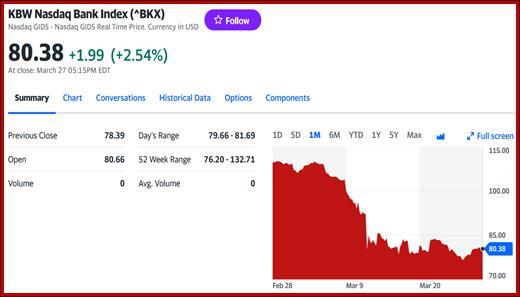

For the moment, a fresh banking crisis has not reared its head. The KBW bank index is fairly steady, if far down from Feb levels. The 2-year note yield rose back over 4% and the 2/10 yield curve inversion--the recession predictor–is holding steady around -41, better than -1.07 on March 8. And the CME FedWatch tool shows 52.3% expect the Fed to keep rates the same at the June 14 meeting with 41.2% expecting another 25 bp hike. This looks exactly like what Mr. Powell wants to see and validates the BlackRock outlook. But we can’t count on these metrics to last.

Forecast: This week marks a month-end and a quarter-end. Some traders in every market will be re-balancing and adjusting to end the quarter with the least perilous and most profitable positions. In FX, today is the day to get it done by Thursday and not be seen as waiting for the last minute. Sometimes these quarter-ends are marked by serious moves and other times they come and go almost without notice. We had thought this would be a serious-move occasion and short dollar positions would be pared back. So far, that is not happening. The reason seems to be that a global banking crisis would favor the dollar but relative calm everywhere takes it away.

Tidbit: In the UK, yesterday Bank of England Gov Bailey did a bit of a victory lap, saying "With the Financial Policy Committee on the case of securing financial stability, the Monetary Policy Committee can focus on its own important job of returning inflation to target." Today Bailey told Parliament there is no obvious stress in the UK system” and “more hikes might be needed.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat