Do manufacturing and service PMIs depict the same US economy?

- Sentiment in the manufacturing and service sectors diverge in December.

- Employment indexes in both sectors declined, manufacturing to decade low.

- Manufacturing new orders and employment indexes remain in contraction.

The title question of course is facetious. But the strikingly different business sentiment readings in the two sectors need an explanation, as does the recessionary outlook in manufacturing and its actual hiring record.

Purchasing managers’ indexes

Sentiment and activity indexes in the services sector rose in December as the pending trade deal with China set the stage for an improved US economy in the first half of the year.

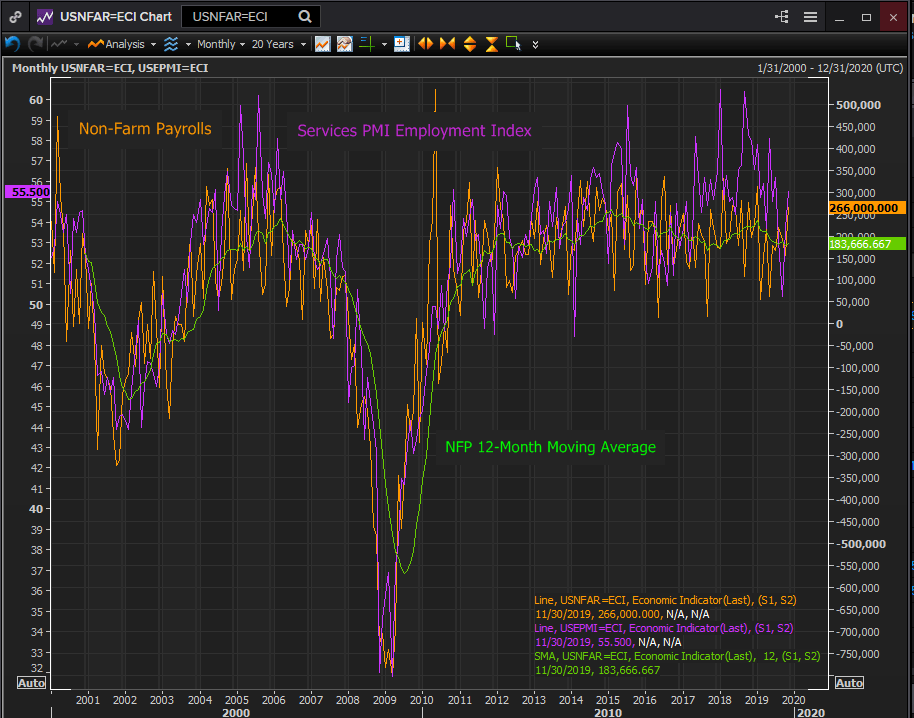

The non-manufacturing purchasing managers index (PMI) from the Institute for Supply Management (ISM) increased to 55 in December, slightly more than the 54.5 forecast and up from the 53.9 reading in November. Business activity jumped from 51.6 to 57.2. The employment index declined 0.2 points to 55.3. New orders fell from 57.1 to 54.9.

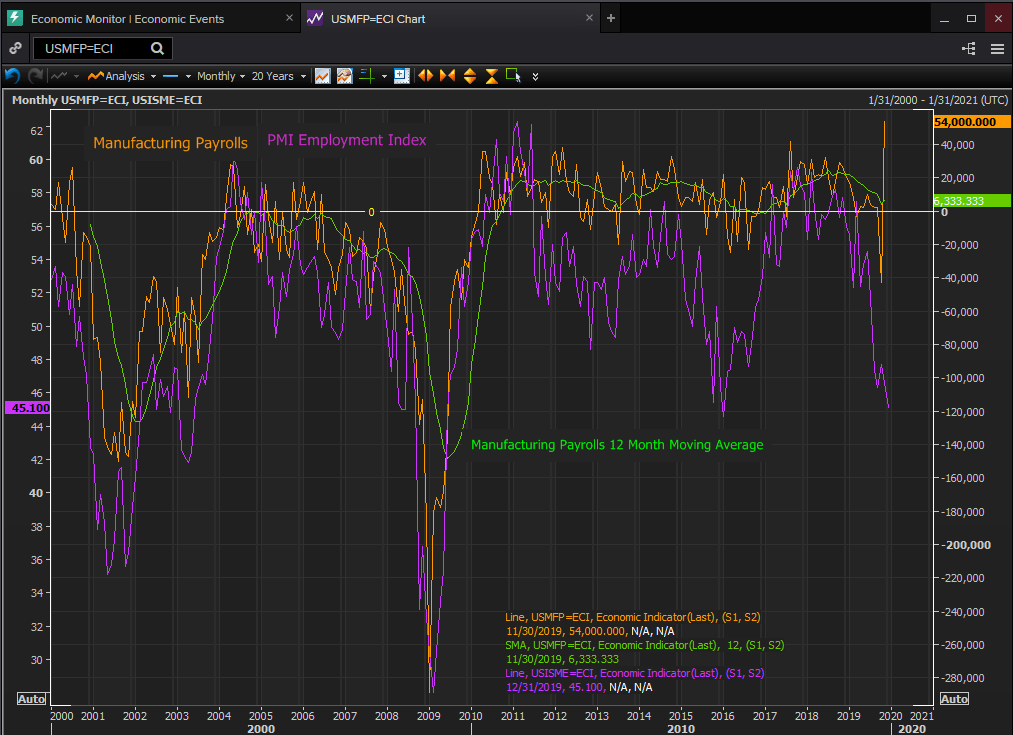

In contrast the manufacturing PMI lengthened its term in contraction to five months dropping to 47.2 in December, its weakest score since June 2009. It was down from 48.1 in November and well below the anticipated rise to 49. The employment index slipped to 45.1 in December, its lowest since June 2016, from 46.6. New orders dropped to 46.8 from 47.2, its poorest showing since April 2009.

China and the US are expected to sign the so-called phase one deal on trade in Washington on January 15th. President Trump has said that he would be traveling to Beijing soon after to begin negotiations on a second agreement.

While the most difficult intellectual property and ownership issues for US companies in China are but partially resolved and most of the American tariffs will remain, Washington has eliminated duties on $160 billion in Chinese consumer products that had been scheduled for December 15th and China has agreed to large purchases of US agricultural products.

As important as the terms of the agreement is the change in direction for the relationship between the world’s largest economies. It was the fear that an escalating Pacific trade war would drive the global economy into recession that prompted rate cuts by the central banks of New Zealand, Australia and the United States and let the European Central Bank to restart its bond purchases

Sentiment and employment in the US economy

The 2.4% annualized growth of the US economy in the first three quarters is expected to be little changed at 2.3% in the final three months of the year by the Atlanta Fed.

This expansion is the answer to the questions posed above. While executives have grown increasingly worried over the two years since the trade dispute began, and for a time stopped spending on capital projects, they continued to hire the new workers required by their current sales.

Non-farm payrolls declined from an excellent 12-month average of 235,000 in January of this year to a merely healthy 185,000 in November. This took place while the services employment PMI dropped from 57.8 in January to 50.4 in September—it has since returned to 55.2 in December.

Reuters

The manufacturing employment index plunged from 55.5 at the beginning of the year to 45.1 in December. Despite five straight months below the contraction demarcation at 50 factory hiring has continued throughout albeit at a slower pace. The 12-month moving average for manufacturing jobs has dropped from 22,000 in January to 11,000 in September, 4,100 in October and 6,000 in November. The 3-month average has dropped from 21,000 in January to 4,000 in November. Factories are forecast to add 5,000 job in December.

Reuters

Manufacturing is more dependent on overseas orders than service industries. All three purchasing related indexes, new orders, export orders and backlog of orders were contracting in December for 5, 2, and 8 months respectively.

Conclusion

Two reasons in combination for the continued hiring in manufacturing are suggested. First the plunge in sentiment was primarily tied to the China trade situation. It did not describe and likely overstated the actual decline in business as the US economy continued a moderate expansion and formerly exported purchases were redirected to domestic suppliers.

Second the drop in sentiment was as much a product of the potential business collapse if the worst trade fears came true, as it was due to the actual change in business.

If things were as bad as described in the manufacturing surveys of the past five months, we might expect to see large job losses in factory work rather than continued placement of new workers.

The divergence in sentiment between the manufacturing and service sectors in that second half of the year was the result of the trade dispute and negotiations between the US and China. As that argument subsides expect business attitudes to reflect realities rather than fears.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.