![]() TheoTrade Analysis Team

TheoTrade Analysis Team

TheoTrade, LLC

Market Reaction To Fed Hikes

This was probably the biggest week of the year for the market in terms of news events as we had the Trump-Kim summit, the Fed meeting, and the ECB meeting which will be on Thursday. With 2 of the 3 major events having occurred, plus the CPI report on Tuesday, the stock market is almost flat for the week. The biggest volatility came after the Fed’s hike decision because risk assets tend to do poorly when the Fed is hawkish. Investors don’t take the improved expectations for growth kindly because it means more rate hikes.

The S&P 500 was down 0.4% and the Russell 2000 was down 0.34%. On the one hand, one more hike in 2018 matters because we’re close to the end of the hike cycle. I don’t think it ends the bull market in the next few months, but the length of time the bull market has left just got shorter. On the other hand, just one member changed his mind which means it can be changed back. I think the decline in stocks is fair because the market was digesting the news. I’m still bullish on stocks this year, but the odds of a bear market in 2019 increased.

Surprisingly, the dollar index was down on the news of the hawkish guidance. The dollar was down headed into the decision. After the decision, it popped 43 cents and then quickly fell back to where it was trading at before the meeting. It closed down 28 cents to $93.55. When you look at the stock market’s somewhat muted response, the reaction becomes less surprising, but I would have expected a positive move.

The treasury market moved as you’d expect as the short end yields increased, which caused the curve to flatten. The Fed always gives lip service to the yield curve, but it clearly doesn’t care about an inversion. The Fed decided to press down on the gas pedal as the car approaches a brick wall. The 2 year yield increased 2.88 basis points to 2.57% and the 10 year was about flat. Both bond yields spiked and then rescinded some of the increase after the Fed statement was released.

At the top of the spike, the 2 year yield hit the highest point of the cycle. As I mentioned, when the 2 year yield peaks, it’s the peak of the business cycle. You want the 2 year to be increasing. The problem has been the speed of the increase and the slowness of the increase in the 10 year yield. The latest difference between the two bonds is 39.88 basis points. It has broken the 40 basis point mark for the first time which means the chances of an inversion by the end of this year have increased. It’s reasonable to figure out how you will hedge your investments or sell some of your risky bets to weather the potential bear market which will occur in 2019 or 2020.

Review Of The Fed Statement Changes

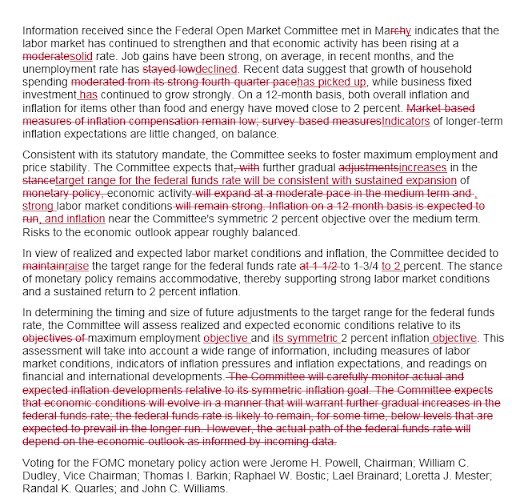

The biggest change to the Fed statement is the length. The Fed statement seen below is only 320 words which is less than half the words in a typical statement. Powell had an hour press conference with the media in which he tried to speak in layman’s terms. It’s debatable if that even matters because the Fed isn’t followed by the general public anyway. Powell isn’t a PhD. economist. Therefore, his language has less wonkish terms even when he’s not trying to be simplistic. He announced the Fed will be doing pressers after every meeting in 2019. This is in tune with the trend of the Fed becoming more transparent. 2019 is going to be a big year for monetary policy because it will be close to the end of the rate hikes if not the end. I can’t see the Fed ever taking these presses away even after this important year and the incoming recession because it would be like Yellen’s Fed not having a statement.

The first change seen above is economic activity is rising at a solid rate instead of a moderate rate. This reflects the expectation that Q2 GDP growth will be 3.7%. The scary part of this situation is if economic growth slows in the rest of the year like the ECRI forecast expects, the Fed will be caught being too hawkish. It’s unlikely Q3 and Q4 will grow at the same rapid rate.

The second change is it says the unemployment rate declined instead of stayed low. That’s just a literal depiction of the metric. The next point is household spending picked up instead of moderated. That’s hawkish, but there’s a big caveat in that Q1 consumer spending growth was very weak. It doesn’t take much for growth to accelerate from 1%.

More Succinct Statements Coming?

The next point which was eliminated is where it said the market based measures of inflation remained low. It was changed to saying indicators of long term inflation expectations are little changed. This is an odd change because the breakeven inflation rate is at about the same rate it was in March. Yes, that is little changed, but it also remains low, so it’s odd to take that part out. I see this change as no change to tone. I think the change was made so the statement is more succinct. This statement is very short, so there needed to be changes like this to get it there. Maybe the Fed feels longer pressers eliminate the importance of the statement.

The same can be said about the other changes in the statement. To me, it looks like the Fed worked as an editor to eliminate unnecessary phrases. It also looked like the Fed tried to make the whole statement more like a boiler plate memo. This may be the beginning of the end of my analysis of these statements as they become shorter and less opinionated. 320 words doesn’t allow much to change for the next statement. Unless there’s a big change in the data, I expect the next statement to be almost exactly the same as this one. The Fed has done about all it can do to clean up the language of statements used when Yellen was chair.

Don Kaufman: Trade small and Live to trade another day at Theotrade.

Neither TheoTrade or any of its officers, directors, employees, other personnel, representatives, agents or independent contractors is, in such capacities, a licensed financial adviser, registered investment adviser, registered broker-dealer or FINRA|SIPC|NFA-member firm. TheoTrade does not provide investment or financial advice or make investment recommendations. TheoTrade is not in the business of transacting trades, nor does TheoTrade agree to direct your brokerage accounts or give trading advice tailored to your particular situation. Nothing contained in our content constitutes a solicitation, recommendation, promotion, or endorsement of any particular security, other investment product, transaction or investment.

Trading Futures, Options on Futures, and retail off-exchange foreign currency transactions involves substantial risk of loss and is not suitable for all investors. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources. You may lose all or more of your initial investment. Opinions, market data, and recommendations are subject to change at any time. Past Performance is not necessarily indicative of future results

Recommended Content

Editors’ Picks

USD/JPY holds above 155.50 ahead of BoJ policy announcement

USD/JPY is trading tightly above 155.50, off multi-year highs ahead of the BoJ policy announcement. The Yen draws support from higher Japanese bond yields even as the Tokyo CPI inflation cooled more than expected.

AUD/USD extends gains toward 0.6550 after Australian PPI data

AUD/USD is extending gains toward 0.6550 in Asian trading on Friday. The pair capitalizes on an annual increase in Australian PPI data. Meanwhile, a softer US Dollar and improving market mood also underpin the Aussie ahead of the US PCE inflation data.

Gold price keeps its range around $2,330, awaits US PCE data

Gold price is consolidating Thursday's rebound early Friday. Gold price jumped after US GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the Fed could lower borrowing costs. Focus shifts to US PCE inflation on Friday.

Stripe looks to bring back crypto payments as stablecoin market cap hits all-time high

Stripe announced on Thursday that it would add support for USDC stablecoin, as the stablecoin market exploded in March, according to reports by Cryptocompare.

Bank of Japan expected to keep interest rates on hold after landmark hike

The Bank of Japan is set to leave its short-term rate target unchanged in the range between 0% and 0.1% on Friday, following the conclusion of its two-day monetary policy review meeting for April. The BoJ will announce its decision on Friday at around 3:00 GMT.