Bond yields everywhere rose a little on relief from geopolitical tension

Outlook:

Bond yields everywhere rose a little on relief from geopolitical tension, even French yields with the election looming on Sunday. Markets have been focused on recent displays of White House machismo, but an equally big disrupter could be the French election.

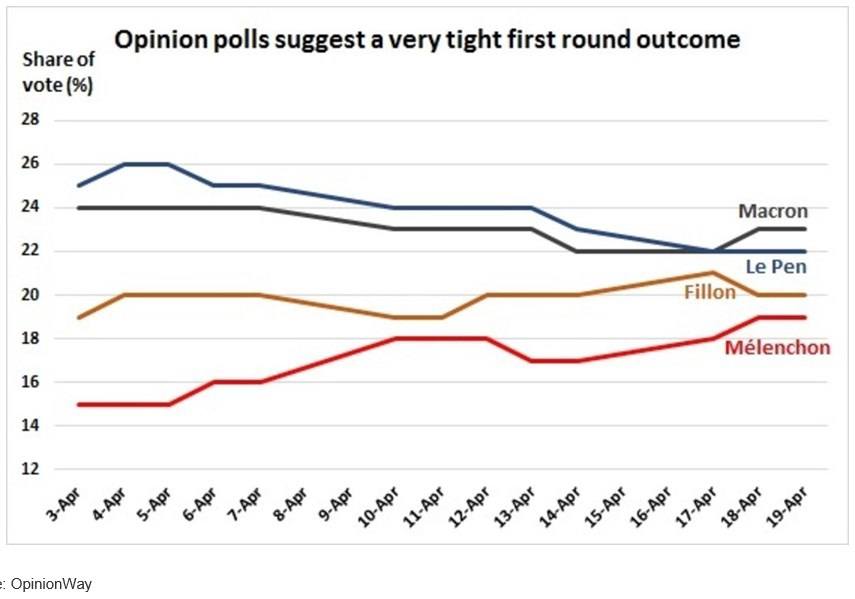

We are puzzled by the euro not losing it moxie ahead of the electoral run-off in France on Sunday. Econoday published the latest poll below. The expected outcome is Macron and LePen coming out on top for the second run-off in May, but if it's Melenchon, head for the bunkers. The FT's Chisholm, who knows a hawk from a handsaw, has a tidbit today saying the negative scenario (LePen and Menenchon) raise Frexit danger that could push euro as low as $0.90.

Nobody trusts polls after Brexit and Trump, but CNBC reports the Cevipof opinion poll published yes-terday "showed frontrunners Macron and Le Pen both losing some momentum ahead of Sunday's first round, and conservative Francois Fillon and Melenchon still in contention for the second round run-off in May."

Oddly, Bloomberg reports France auctioned €5.5 billion in 3-year and 5-year notes today and got a bid-to-cover of 1.99, better than the 1.86 seen in the Jan auction. That was for a 5-year note. The FT reports "The premium for 10-year French bonds over Bunds has generally been around 40 basis points in recent years, so the current spread above 70 bps is certainly enticing for traders willing to bank on a middle-ground candidate eventually winning. We have already seen money flow into Europe, ignoring the sight of various volatility measures straining at the leash like a half-starved whippet." The FT has 0.67 bp for the French-German spread at around 8 am today. Here's the question—why is it not much, much wider?

We like to think the worst-case outcome in France will affect only European yields, but is that really so? Why would the US yield not also dip on a safe haven inflow if the outcome is LePen-Melanchon? We could get the strange outcome of falling US yields and a falling dollar/rising euro on an event that "should" clearly be euro-negative. We have seen stranger things. And let's note that three of the four top candidates are pro-Putin. We have no idea what this may mean down the road.

We intend to get out of any positions by 1 pm on Friday. We seem to be the lone coward. The bond boys are having a ball betting on the French election.

Here's another possible disruption this coming weekend: the World Bank/IMF meetings start today in Washington. Normally we get only a random nugget or two on the sidelines, but this time the central issue will be Trump's America First stance, which runs directly counter to the very heart and soul of the IMF. Insiders say IMF chief Lagarde intends to "socialize" the Trumpies, especially about protec-tionism.

Commerce Secy Ross already pushed back with remarks last week that the US is the least protectionist of the majors. Trump pushed back on Monday with "Buy America" and "Hire America." Former IMF official and generally smart guy Prasad told Reuters "The IMF has little leverage since its limited toolkit of analysis-based advice, persuasion, and peer pressure is unlikely to have much of an impact on this administration's policies." That's the polite way of saying the Trumpies will be pig-headed.

Reuters reports Lagarde will interview TreasSec Mnuchin on stage during the meetings. Yikes! He did not acquit himself well in the FT interview on Monday. Mnuchin is no dummy but not accustomed to the public stage and visibly torn between the conventional sane and reasonable approach to internation-al economics vs. the Trump version.

Having said that, the Trump version is not entirely wrong. In fact, it's largely right. It's perfectly true that other countries have manipulated currencies and do subsidize exports in various ways, some of them buried so deep in their infrastructure they are really very hard to find. A policy approach that fa-vors US self-interests more openly is not a bad thing.

We just wish the Trumpies would do it in a brainier and classier way. The Treasury must have dozens of economists in the backroom with piles of data at hand. But it's a hallmark of the Trump administra-tion not to use hard facts and sound analysis, but rhetorical blasts instead. For example, VP Pence is in Indonesia today offending the government by complaining about its trade surplus with the US. Pence is not the brightest bulb in the chandelier and almost certainly not qualified to talk trade.

We are especially worried about Japan in this context. PM Abe was out front in starting trade talks with the US and has been leaning over backwards to get friendly treatment. It seems to have been working so far—we haven't had any outbursts from the White House against Japan. China is in the same posi-tion, with Trump seemingly willing to swap help with N. Korea for less strident trade demands. But just wait.

If you are going to shoot first and ask questions afterwards, okay—but then you really do need to ask the questions. The US vs. the rest of the world is not going away when the Washington meetings end, either. We are in for a long slog. We may get a new version of presidential interference in the FX mar-ket next week when Trump meets Italian PM Gentiloni in Washington. Then he's on to a NATO sum-mit in Germany and thence to G7 in Sicily (May 26-27).

From Left Field: We are watching failed state Venezuela out of the corner of the eye. Things keep getting worse. Here's a doozy for the trigger-happy Trump: the government seized a GM plant in Va-lencia and halted operation. It seized assets, which we guess means the factory itself and its bank ac-counts.

Politics: Bill O'Reilly bore the brunt of a renewed awareness of misogyny triggered by Trump. O'Reil-ly said he was railroaded by unfounded charges, which would come as a surprise to the fancy white-shoe law firm that did the research and judged he had to be fired. Not just smoke, real fire. Even some sports heroes declined to attend a White House shindig lest their children see them hob-nobbing with the groper-in-chief. Civil liberties groups joined forces, too.

Now it remains for the libs to do it right this time and not become so insufferably holier-than-thou that even dyed-in-the-wool feminists and libertarians are repelled.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 109.06 | SHORT USD | 03/21/17 | STRONG | 112.51 | 3.07% |

| GBP/USD | 1.2827 | LONG GBP | 04/12/17 | STRONG | 1.2495 | 2.66% |

| EUR/USD | 1.0760 | LONG EURO | 04/13/17 | STRONG | 1.0643 | 1.10% |

| EUR/JPY | 117.35 | SHORT EURO | 03/28/17 | STRONG | 120.19 | 2.36% |

| EUR/GBP | 0.8389 | SHORT EURO | 04/12/17 | STRONG | 0.8487 | 1.15% |

| USD/CHF | 0.9957 | SHORT USD | 04/13/17 | STRONG | 1.0043 | 0.86% |

| USD/CAD | 1.3488 | SHORT USD | 04/13/17 | WEAK | 1.3244 | -1.84% |

| NZD/USD | 0.7015 | SHORT NZD | 04/12/17 | WEAK | 0.7022 | 0.10% |

| AUD/USD | 0.7514 | SHORT AUD | 03/28/17 | WEAK | 0.7607 | 1.22% |

| AUD/JPY | 81.95 | SHORT AUD | 03/22/17 | STRONG | 85.20 | 3.81% |

| USD/MXN | 18.8324 | SHORT USD | 01/31/17 | STRONG | 20.8108 | 9.51% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat