Beware the Student Loan Grinch

If I had to attend mandatory addiction classes, it would be CA, or Christmas Anonymous, for those who look forward to the holiday season just a bit too much and then suffer when it’s over.

December 26 is always a bummer for me because I know Christmas is 364 days away. Of course, at that point, I also know I’m getting closer to taking down decorations, which is no fun for anyone.

In fact, a recent survey by Christmas Lights, Etc. – an online store – found that when it comes to all things Christmas, taking down decorations is the least favorite activity of every age group, except Millennials. For the young set, sticking to a budget is the worst part, with denuding in second place.

It’s fitting that those under 35 would focus on money, since they don’t have much. And at this time of year, the most recent college graduates among them get another reminder of their broke status.

The student loan Grinch is on his way.

When you graduate college – or leave without graduating – student loan providers give you six months to get on your feet. After that, you’re expected to start making the monthly strokes. For those who graduated in May 2017, December brings their first Christmas as working stiffs, and their first installment payment on student loans.

Since two out of three graduates from public universities and three out of four graduates from private institutions carry student loan debt, the vast majority of first-year graduates fall into this category. They join a bulging population of borrowers who have piled on massive amounts of debt in the past 15 years.

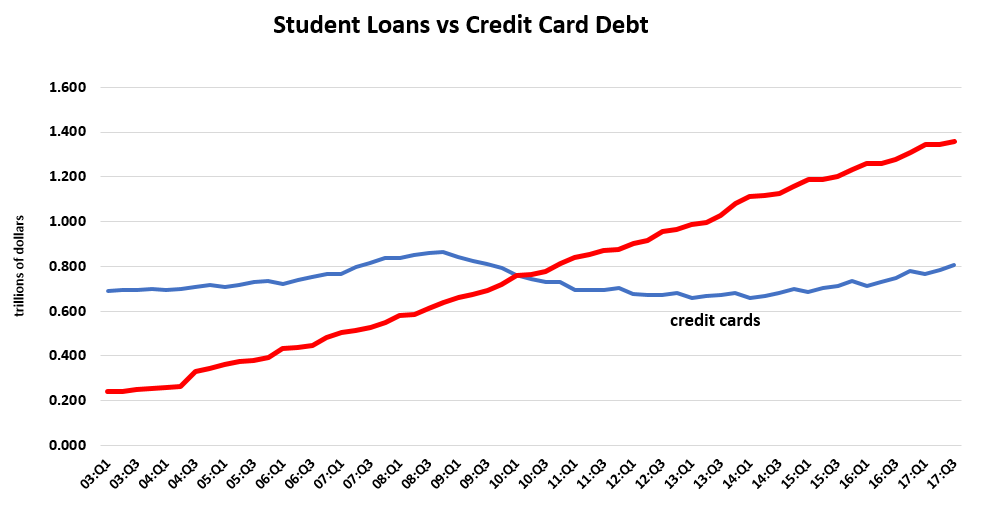

This chart compares student loan debt to credit card debt since 2003.

In the last decade and a half, student loan debt has exploded from $241 billion to $1.357 trillion, while credit card debt expanded from $688 billion to $808 billion. Student loan debt grew 463% compared with 17% for credit card borrowing.

But before you start to feel bad for the hapless graduates, consider that many of them find a way to ease their repayment pain.

Only 54.4% of borrowers are making payments on their debt. The rest are either still in school (10.2%) or fall into one of several non-payment flavors. The typical graduate gets to breathe easy for six months in a normal grace period, which accounts for 3.4% of current borrowers. Another 9.9% have been granted a deferment and 10.9% a forbearance.

Deferments don’t accrue interest during the payment holiday, and are typically granted when the borrower goes back to school, joins the Peace Corp, loses a job, or has some other employment interruption.

Forbearances are closely related and granted for medical expenses or financial difficulties, but borrowers are responsible for accrued interest.

The always-present “other” category accounts for 1% of loans, leaving the tough-luck crowd in default with 10.2% of all loans outstanding. Just like bad things in your rearview mirror, the last category is larger than it appears.

Defaults might be one-tenth of the total, but one-third of student loans (current students, forbearances, and deferments) aren’t in repayment. If we just count those in repayment and those in default (54.4% and 10.2%), then non-payers account for 15.8% of the total.

When more than 15% of your borrowers aren’t paying back their debt, you know there’s a problem in the system.

And many of those making payments will never pay all that they owe.

In the late 2000s we developed income-based repayment plans and Pay As You Earn (PAYE) programs.

The idea was to better match loan payments with earnings, allowing those who earn less early in their careers to pay less at the same time. Such plans have a termination date, or a get-out-of-jail-sort-of-free date, after which the borrower owes nothing, even if he has not paid off his loan.

Just under half, or 42.5% of those currently paying off their debt, participate in one of these programs. This leaves just a mere 31.3% of student loan borrowers making full payments on their debt.

It’s starting to feel like the Grinch is coming for someone else – student loan providers, which means me and you, the U.S. taxpayers.

We probably won’t feel immediate pain from this twisted saga. The U.S. debt will increase, which will most likely cost us in the form of higher interest payments down the road but won’t limit the number of presents we have under the tree this year.

Graduates with debt, however, will shoulder a burden, even if it’s one they chose. Those paying their loans, paying less than the full amount on their loans, in some sort of forbearance or deferment, or even in default, take this baggage everywhere they go.

Whether walking down the aisle with their future spouse or into the signing room at a title company, the debt comes along. They simply won’t spend as much in their early adult years as previous generations because they used up some of their precious capital while sitting in the classroom.

In this light, the student loan Grinch weighs on the entire economy, curbing the economic benefits of adding the next generation to the working class. Judging by the trendline on the chart, this won’t end anytime soon.

But it seems out of touch with the season to end on sour note.

Since there’s no growing the student loan Grinch’s heart with a sudden rendition of alma mater fight songs, I’ll just refer back to the Christmas Lights, Etc. survey.

According to their data, our favorite Christmas movies are determined by our age, with the older generation preferring Miracle on 34th Street, and the young group leaning, appropriately, toward Jim Carrey’s version of How the Grinch Stole Christmas.

Author

Dent Research Team of Analysts

Dent Research