Bank of England steps up talks on negative interest rates amid uncertain outlook

The BoE kept rates unchanged but said it was mulling how to implement negative rates effectively. This has brought markets' expectations of negative rates forward. It is very likely the BoE would expand asset purchases and cut rates into negative territory if a deal with EU is not reached. Unprecedented monetary policy support would be needed to support the economy from twin stresses of COVID and no deal Brexit. The BoE also said it would refrain from hiking rates until inflation sustainably reached its 2% target. The Pound weakened post the BoE policy. Yield on UK 6 month bills hit a new record low of -0.04%. However, the Pound recovered later on broad USD weakness.

US jobless claims in line with expectations at 860k. Continuing claims also came in better than expected at 12.6mn (exp 13mn) but nevertheless continue to remain elevated.

The RBI bought bonds aggressively in the OMO twist with cut off coming in way below market yields (RBI bought bonds at higher prices compared to market). The RBI also announced an outright OMO for 10000crs. The RBI is sending a signal across but market participants are still wary of taking duration ahead of the announcement of H2 borrowing calendar on 30th Sep and RBI monetary policy on 1st Oct.

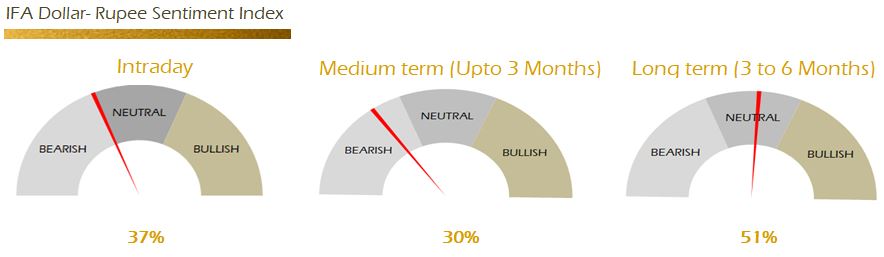

USD/INR continues to trade an extremely tight range. There are inflows but the RBI has been absorbing them. Until we see the next leg of USD weakness, the RBI may not step aside to let the Rupee readjust. We may continue to see the Rupee in 73-74 range until then. Over the next couple of sessions, we are likely to see inflows to the tune of USD 1bn on account of FTSE index rebalancing. USDINR is likely to trade 73.35-73.65 range.

Strategy: Exporters are advised to cover confirmed order on upticks or go for risk reversal strategy. Importers are advised to hold. The 3M range for USDINR is 72.50 – 74.50 and the 6M range is 72.50 – 75.40.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.