AUD/USD Price Forecast 2022: The China threat could temper Aussie’s turnaround

-

AUD/USD faded the post-pandemic recovery in 2021, despite the pro-risk market environment.

-

The Aussie risks a turnaround amid a potential RBA hawkish surprise, higher commodities prices.

-

Looming Chinese risks on trade and economic front could temper AUD/USD’s upswing.

- AUD/USD’s weekly technical setup suggests the rebound could remain limited.

The AUD/USD pair emerged as the most underperforming currency within the G10 basket in 2021, losing roughly 9% on the year. Does that provide a strong reason to witness a major turnaround for the aussie in 2022?

The 2020 post-pandemic recovery seen in the currency pair lost legs in 2021, undermined by the dovish stance from the Reserve Bank of Australia (RBA) and a pause in the commodity ‘Supercycle’. Although a likely shift in the gear by the RBA and improved economic performance pose upside risks for the aussie in 2022. Will the recovery be a smooth sail amid looming Chinese concerns?

AUD/USD: 2021 in the rearview

The AUD/USD recovery from the March 2020 lows of 0.5507 failed to sustain above the 0.8000 threshold in the first quarter of 2021. Since then, the downtrend kicked in, with the currency pair settling the year around 0.7100.

The optimism over global economic recovery from the coronavirus pandemic-induced blow incited a record rally in the US stocks, as risk-on market profile remained the dominant theme in 2021. The S&P 500 futures, better known as a risk barometer, gained nearly 20% over the year, although the high-beta currencies such as the Australian dollar failed to capitalize from the risk appetite.

The Delta and Omicron story

The aussie resumed the bearish trend after the world was hit by the Delta covid variant, with Australia heavily affected by the extended lockdowns amid a relatively slower pace of vaccinations in the country. At that time, just under 5% of the adult population was fully vaccinated, with 29% having received a first dose.

In the past year, Australia was lauded for its relative success in combating the global pandemic. However, in June 2021, the country’s most populous states of New South Wales (NSW) and Victoria were back under lockdowns, which extended through October. Nationwide, 41% of Australia’s population was fully vaccinated and 63% had at least one dose.

Just as the economy reopened, the new Omicron covid variant held back the authorities to announce border openings, as uncertainty over the new strain prevailed.

RBA dovish but confident on the economy

The RBA, however, maintained throughout the year that the economy retains the ability to rebound quickly, as observed during the 2020 lockdowns. At its September monetary policy decision, Governor Phillip Lowe said, “the Delta outbreak is expected to delay, but not derail, the recovery.” The same, he reiterated during the December 7 policy announcement, in the face of the Omicron variant.

The RBA’s confidence in the economic recovery was justified by a smaller-than-feared economic downturn in the South Pacific island nation, with the GDP contracting only by 1.9% in the third quarter. The country’s solid retail sales, upbeat exports, public spending and current account position offered a more optimistic outlook on the economy.

The Australian central bank trimmed the weekly bond purchases to AUD4 billion per week from AUD5 billion, acknowledging the economic upturn. But it stuck to its dovish tone amid benign inflationary conditions, noting explicitly that the “board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range.” The bank did mention that “a further pick-up in wages growth is expected as the labour market tightens”.

Australia-China diplomatic row

The worsening Australian-Sino diplomatic ties added to the pain in the aussie dollar, as China is the South Pacific nation’s biggest trading partner.

Ties have been fraught since 2018 when Canberra barred Huawei Technologies Co. from building its 5G network on national security grounds. In response, China imposed tariffs on Australian barley and wine, and blocked shipments of timber, coal, lobster and other goods from May 2020. Beijing accused Australia of taking a hostile approach on issues ranging from a clampdown on foreign investment to questions on the origins of COVID-19. China also took aim at Australia's use of offshore detention for asylum seekers and alleged war crimes in Afghanistan.

Making matters worse, Australian Prime Minister Scott Morrison said that he will not send officials to the Winter Olympics in Beijing, citing the latter’s human rights atrocities in the far western region of Xinjiang and ongoing trade row.

2020 commodity supercycle fades

A downswing in the industrial metals, including copper, iron-ore and silver, weighed negatively on the resource-linked aussie. Concerns over rising global inflationary pressures and its impact on the economic growth capped the multi-year highs rally in the metals. China’s distressed property sector woes also emerged as one of the key catalysts, undermining the demand for metals.

However, the record surge in natural gas and coal prices did help to alleviate the bearish pressure on the commodity-currency. Soaring energy prices, courtesy of a cold and long winter in the Northern Hemisphere and a weaker-than-expected increase in supply, offered a brief reprieve to AUD bulls in October before the selling spiral resumed. Note that Australia was the world’s largest exporter of liquefied natural gas (LNG) in 2020.

AUD/USD: 2022 what to watch out for

Heading into the year 2022, the factors that shaped up the aussie price action are likely to play out, although a few of them could turn in favor of bulls. A ray of hope appears due to the economic optimism and a likely resumption of the commodity ‘Supercycle’.

Pick up in wage inflation

The RBA has been confident of the economic upturn and with vaccine rollout picking up pace, the Australian economy is expected to bounce back strongly from lockdowns.

Conducive economic environment could prompt RBA Governor Phillip Lowe to walk back on his words that the first post-pandemic hike in the cash rate will not be before 2024.

The central bank’s December 7 policy statement offered no new surprises but it offered a glimmer of hope for the hawks. The RBA talked up the prospects of an increase in wages this month, citing: “A further pick-up in wages growth is expected as the labour market tightens.” In November, Lowe linked the probability of wage growth to a potential rate hike in 2022.

Industry experts and analysts believe wages growth will accelerate by H2 2022. The uptick in wages is expected partly due to workers exercising their increased bargaining power by asking for higher wages and/or moving to better jobs amid growing number of industrial disputes in the country.

Dissipating RBA-Fed divergence

As the RBA suggested that its QE programme will be considered next year, it is highly likely that it may signal an end to its bond-buying in the February meeting. Markets could begin pricing in a rate hike as soon as the QE programme ends. With the economy rebounding firmly from the covid blow alongside solid employment, increasing domestic demand and higher commodities prices, the aussie central bank could very well gear up for a hawkish surprise and announce a rate lift-off in the second half of 2022.

The US-Australian money market curve could narrow if the RBA comes out hawkish, fading the monetary policy divergence with the US Federal Reserve. In the grand finale of 2021, the Fed opened the door to a March rate hike, especially after it doubled the pace of tapering to $30 billion and its dot plot chart showed three rate increases next year. The Fed’s hawkish shift suggests that it remains worried about inflation. The CME Group’s FedWatch Tool now shows a 47% chance of a 25bps rate hike in the May FOMC meeting.

Global energy transition and higher commodities prices

World leaders are ramping up efforts to address climate change, with energy transition at the core of their agenda. A shift towards renewable energy will drive up demand for raw materials — including rare earth metals, copper, platinum etc, — to build installations and storage solutions.

With China being the world’s biggest emitter of carbon and the largest commodity consumer, its economic growth prospects and policies will be key to shoring up commodities prices and, in turn, the aussie.

China’s energy crisis is likely to extend into the next year, keeping the prices of coal and gas on the higher side. It’s worth noting that Beijing is heavily dependent on Australian coal to meet its energy demand.

The People’s Bank of China (PBOC) cut the Reserve Requirement Ratio (RRR) for the second time in 2021 to stimulate the economic recovery while the factory gate prices eased, allowing some room for the central bank to ease policy further. Moving forward, China’s policy support measures could aid the aussie’s upturn.

Looming dual Chinese threats

The first half of 2022, however, could be a bumpy ride for the antipodean, as China’s distressed property sector problems will extend, limiting the upside in the commodities prices. The country’s real estate giants Evergrande Group and Kaisa Group are at risk of defaults and the authorities are leaving no stone unturned to avoid the fateful event.

Another impediment to the aussie’s recovery could be escalating Australian-Sino tensions, with trade relations between the closest partners on the brink. Australia is poised to show the world what decoupling from China looks like amid deteriorating diplomatic and trade ties.

Stretching beyond the Pacific, US-China trade relationship will also play a pivotal role in the AUD valuations. The Trump administration struck a Phase One trade deal with Beijing in January 2020. In November 2021, US President Joe Biden held the first meeting with his Chinese counterpart Xi Jinping. Both sides exchanged bold remarks, with America opposing unilateral efforts to change the status quo of Taiwan. Meanwhile, China’s President Xi urged the Biden administration not to politicise Sino-US trade issues.

If the US-China relations turn south, it could have a significant impact on the market sentiment, eventually affecting the risk-sensitive assets such as the Australian dollar.

AUD/USD: 2022 technical picture

So, to speak, a big sell-off looms for AUD/USD in the coming months, especially after the price confirmed a Head-and-Shoulders (H&S) breakout on the weekly chart during the final week of November 2021.

The H2 2020 recovery, followed by the descent this year, carved out an H&S formation on the said time frame. The fourth straight weekly decline in end-November, back then, prompted a breach of the pattern neckline at 0.7158, paving the way for a massive slump going forward. The pattern target is measured at 0.6190, a level not seen since April 2020.

However, 0.7063, the 38.2% Fibonacci Retracement (Fibo) level of the entire post-pandemic recovery, starting from March 2020 troughs of 0.5508 to February 2021 peak of 0.8008, has emerged as critical support for the currency pair.

The bulls have bounced off the latter on multiple occasions since October 2020. The bull cross, represented by the 100-Weekly Moving Average (WMA) having climbed above the 200-WMA, has also provided additional support to the aussie buyers.

The major has also found acceptance above the pattern neckline, now 0.7170, although recapturing the 0.7200 barrier is critical to unleashing the additional recovery. The 100 and 200-WMAs hang around near that psychological magnet.

If the turnaround in AUD/USD gains momentum, then the next resistance is envisioned at the bearish 21-WMA at 0.7298, above which the bulls will challenge the 23.6% Fibo level of the same ascent, pegged at 0.7432.

Further up, the downward-pointing 50-WMA resistance at 0.7513 will be put to test once again. The price has failed to find a strong foothold above the 50-WMA since early September 2021.

It’s worth mentioning that recapturing the mid-0.7500 levels could lead to the H&S pattern failure, which would then entice additional bullish interest. A sustained break above the latter could bring the 2021 peak of 0.8008 back in sight.

On the flip side, a weekly closing below the 38.2% Fibo support could reinforce the selling interest, opening floors towards the 50% Fibo level at 0.6768. The last line of defense for AUD bulls awaits at the 61.8% Fibo level at 0.6474.

The weekly Relative Strength Index (RSI) has stalled its recovery, turning south while below the midline. This suggests that the AUD/USD recovery in the next year could likely lose steam.

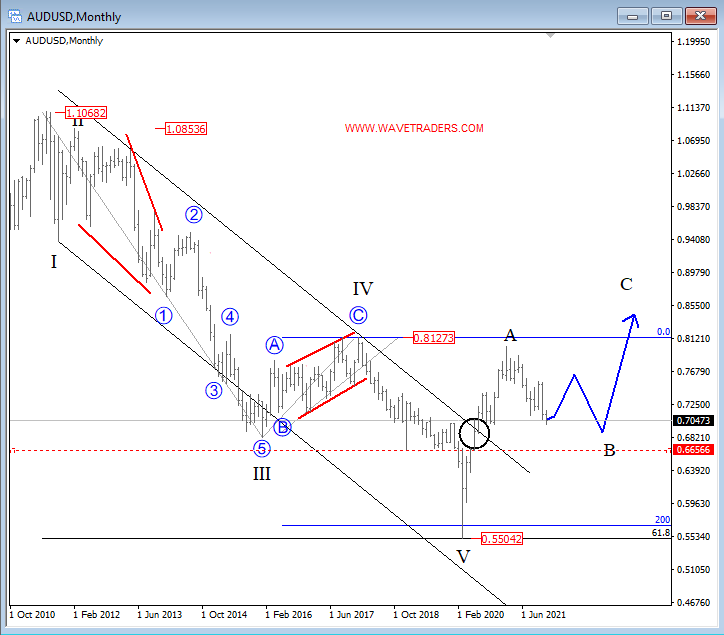

Gregor Horvat projects a bullish scenario for the Australian dollar/US dollar pair on his Elliott Wave analysis:

AUD/USD Elliott Wave Analysis

Aussie came out of a big downward channel which means that pair is most-likely trading in a higher degree correction. But corrections are in three waves, so more upside can be seen in 2022, but after wave B pullback which is underway now and it ma retrace close to 0.6600 area before bulls shows up for wave C.

Forecast Poll 2022

| Forecast | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Bullish | 29.62% | 17.24% | 23.33% |

| Bearish | 22% | 24.13% | 23.33% |

| Sideways | 44.44% | 55.17% | 50.00% |

| Average Forecast Price | 0.7204 | 0.7177 | 1.1264 |

| EXPERTS | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Alberto Muñoz | 0.6850 Bearish | 0.6650 Bearish | 0.6300 Bearish |

| Andrew Lockwood | 0.7000 Sideways | 0.6800 Bearish | 0.6700 Bearish |

| Brian Wang | 0.6830 Bearish | 0.6810 Bearish | 0.6590 Bearish |

| ANZ FX Strategy Team | 0.7500 Bullish | 0.7500 Bullish | 0.7500 Sideways |

| Barclays | 0.7500 Bullish | 0.7600 Bullish | 0.7800 Bullish |

| BoA FX Rates & Commodities Team | 0.7400 Bullish | 0.7400 Sideways | 0.7700 Bullish |

| Brad Alexander | 0.7000 Sideways | 0.6950 Sideways | 0.6800 Sideways |

| CIBC World Markets Team | 0.7400 |