AUD strengthens after CPI report, market waits on US data

Forex News and Events

Australian CPI surprises to the upside (by Arnaud Masset)

The last CPI report from Australia surprised substantially to the upside with the headline measure printing at 1.3% in the third quarter versus 1.1% median forecast. The sharp increase was mostly due to an important rise in fruit (+19.5%), vegetables (+5.9%), electricity (+5.4%) and tobacco (+2.3%) prices. On the other hand, automotive fuel (-2.9%) and telecommunication equipment & services prices (-2.5%) dragged the gauge down. In spite of this good news, the core figures were left unchanged with the trimmed mean stable at 1.7%y/y, while the weighted median mean eased came in slightly below median forecast as it printed at 1.3%y/y very 1.4% expected.

All in all, this inflation report does not change the big picture, especially for the Reserve Bank of Australia, as core inflation remains subdued meaning that the door is still open for another rate cut. However we expect the central bank will remain on hold next week, waiting for further clarity - especially from the US where the Fed and presidential election could impact markets significantly - before cutting the cash rate target another 25bps. The Australian dollar surged 0.64% after the release and consolidated those gains afterwards. The Aussie stands amongst the few currencies that did not lose ground against the dollar as market participants started to price in a December rate hike in the US. Therefore, there is still upside potential, especially should the Fed delay further any tightening move.

New homes sales data set to reflect underlying US difficulties (by Yann Quelenn)

US new home sales rarely decline twice in a row. Over the last two and a half years this has only happened once - at the beginning of this year. In addition, the downside move was somewhat limited with new home sales declining from 538k to 525k from December 2015 to February 2016. Last August, homes sales declined by -7.6% from 650k to 609k, which represented the biggest monthly decline in 11 months. Today’s data is expected to head lower by -1.5% to 600k new home sales.

The trend in home sales is nevertheless positive. The bottom was touched in February 2011 three years after the subprime crises exploded. The era of free cash has pushed real estate massively higher and while markets are now pricing a decent likelihood of a December rate hike, we should see the start of a slight correction in the housing market. In our view, this will remain temporary as no more rate hike should happen in 2017. We believe that the Fed will keep interest low while inflation starts running higher. This move will mostly be aimed at killing the massive US debt and taking back control of the economy as monetary policy becomes increasingly inefficient the more debt continues to rise.

As a result, the US middle class is certainly going to suffer in the coming few months/years. The demand for dollar is set to continue and we maintain our bearish view on the currency. Yet, there is no big upside on the green note at the moment as a Fed rate hike in December is well priced in.

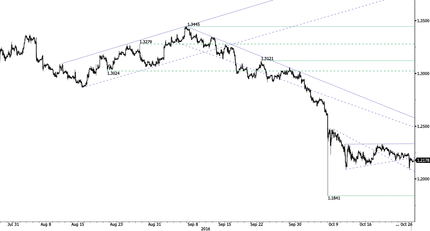

GBP/USD - Bearish Breakout.

| Today's Key Issues | Country/GMT |

|---|---|

| oct..23 FIPE CPI - Weekly, exp 0,10%, last 0,02% | BRL/07:00 |

| Sep Trade Balance, last -10.3b | SEK/07:30 |

| Aug Retail Sales MoM, exp 0,40%, last -0,30% | EUR/08:00 |

| Aug Retail Sales YoY, exp 0,50%, last -0,20% | EUR/08:00 |

| Sep BBA Loans for House Purchase, exp 37350, last 36997 | GBP/08:30 |

| Oct FGV Consumer Confidence, last 80,6 | BRL/10:00 |

| Oct FGV Construction Costs MoM, exp 0,21%, last 0,37% | BRL/10:00 |

| oct..21 MBA Mortgage Applications, last 0,60% | USD/11:00 |

| Sep PPI Manufacturing MoM, last -0,38% | BRL/11:00 |

| Sep PPI Manufacturing YoY, last 3,11% | BRL/11:00 |

| Sep Advance Goods Trade Balance, exp -$60.5b, last -$58.4b, rev -$59.2b | USD/12:30 |

| Sep P Wholesale Inventories MoM, exp 0,10%, last -0,20% | USD/12:30 |

| Sep Retail Inventories MoM, last 0,60% | USD/12:30 |

| Sep Outstanding Loans MoM, last 0,00% | BRL/12:30 |

| Sep Total Outstanding Loans, last 3115b | BRL/12:30 |

| Sep Personal Loan Default Rate, last 6,20% | BRL/12:30 |

| oct..24 CPI Weekly YTD, last 4,40% | RUB/13:00 |

| oct..24 CPI WoW, last 0,10% | RUB/13:00 |

| Oct P Markit US Services PMI, exp 52,5, last 52,3 | USD/13:45 |

| Oct P Markit US Composite PMI, last 52,3 | USD/13:45 |

| Bank of England Bond-Buying Operation Results | GBP/13:50 |

| Sep New Home Sales, exp 600k, last 609k | USD/14:00 |

| Sep New Home Sales MoM, exp -1,50%, last -7,60% | USD/14:00 |

| oct..21 DOE U.S. Crude Oil Inventories, exp 2000k, last -5247k | USD/14:30 |

| oct..21 DOE Cushing OK Crude Inventory, exp -300k, last -1635k | USD/14:30 |

| Currency Flows Weekly | BRL/14:30 |

| ECB's Praet Speaks in Brussels | EUR/17:00 |

| Sep Trade Balance NZD, exp -1145m, last -1265m | NZD/21:45 |

| Sep Exports NZD, exp 3.53b, last 3.39b | NZD/21:45 |

| Sep Imports NZD, exp 4.68b, last 4.65b | NZD/21:45 |

| Sep Trade Balance 12 Mth YTD NZD, exp -3113m, last -3131m | NZD/21:45 |

| Sep Tax Collections, exp 95014m, last 91808m | BRL/22:00 |

| Sep Formal Job Creation Total, exp -7000, last -33953 | BRL/22:00 |

The Risk Today

Yann Quelenn

EUR/USD's bearish momentum is definitely up and running despite ongoing short-term bullish consolidation. Strong resistance lies at 1.1058 (13/10/2016 high). Key resistance is located far away at 1.1352 (18/08/2016 high). Expected to further weaken towards support area below 1.0860. In the longer term, the technical structure favours a very long-term bearish bias as long as resistance at 1.1714 (24/08/2015 high) holds. The pair is trading in range since the start of 2015. Strong support is given at 1.0458 (16/03/2015 low). However, the current technical structure since last December implies a gradual increase.

GBP/USD has exited symmetrical triangle. Hourly support is now given around 1.2135 (25/10/2016 low) while hourly resistance lies at 1.2332 (19/10/2016 high). Key resistance stands far away at 1.2620 then 1.2873 (03/10/2016). Expected to show continued weakness. The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY is trading mixed but the pair remains within an uptrend channel. A break of hourly support at 102.81 (10/10/2016 low) is unlikely at the moment. Key support can be found at 100.09 (27/09/2016). Hourly resistance is implied by the upper bound of the uptrend channel around 105. Expected to see continued selling pressures. We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF's buying pressures tend to increase but the pair still lies within former resistance area between 0.9919 (07/08/2016 low) and 0.9950 (27/07/2016). In addition, the pair remains on a bullish momentum since September 15. Hourly support is located at 0.9733 (05/10/2016 base) then 0.9632 (26/08/2016 base low). Expected to see continued increase. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

|---|---|---|---|

| 1.1428 | 1.3121 | 1.0328 | 111.45 |

| 1.1352 | 1.2857 | 1.0257 | 107.49 |

| 1.1058 | 1.2477 | 1.0093 | 104.64 |

| 1.0922 | 1.2206 | 0.9914 | 104.06 |

| 1.0822 | 1.209 | 0.9632 | 102.8 |

| 1.0711 | 1.1841 | 0.9522 | 100.09 |

| 1.0458 | 1.052 | 0.9444 | 99.02 |

Author

Arnaud Masset

Swissquote Bank Ltd

Arnaud Masset is a Market Analyst at Swissquote Bank. He has a strong technical background and also works in the development of quantitative trading strategies.