Japanese Yen recovers further from multi-month low against USD amid intervention fears

- The Japanese Yen drops to a fresh multi-month low amid wavering BoJ rate hike expectations.

- Intervention fears, geopolitical risks and the cautious mood drives haven flows towards the JPY.

- The widening US-Japan yield differential should cap any meaningful JPY appreciating move.

The Japanese Yen (JPY) rebounds against its American counterpart after touching its lowest level in nearly six months earlier this Tuesday amid fears that Japanese authorities might intervene in the market to prop up the domestic currency. Adding to this concerns about US President-elect Donald Trump's tariff plans, geopolitical risks and the cautious market mood lend some support to the safe-haven JPY.

Meanwhile, the US Dollar (USD) remains depressed below a two-year high touched last week and contributes to capping the USD/JPY pair. That said, doubts over the timing of when the Bank of Japan (BoJ) will hike rates again could act as a headwind for the JPY. Moreover, the recent widening of the US-Japan yield differential, bolstered by the Federal Reserve's (Fed) hawkish shift, warrants caution for the JPY bulls.

Japanese Yen gains some respite following interevention warning from Japan's Finance Minister

- Japan’s Finance Minister Katsunobu Kato was out with some verbal intervention this Tuesday and said that the government will take appropriate action against excessive FX moves, including those driven by speculators.

- The Bank of Japan last month opened up the possibility of waiting longer before the next rate hike, citing uncertainty over US President-elect Donald Trump's economic policies, which continues to undermine the Japanese Yen.

- Trump denied a Washington Post story that his administration will pursue a less aggressive tariff regime and will only target certain sectors in imposing trade tariffs, instead of the broad tariffs promised during campaigning.

- BoJ Governor Kazuo Ueda said on Monday the central bank will raise interest rates further if the economy continues to improve, though he stressed the need to consider various risks when deciding how soon to pull the trigger.

- Furthermore, the broadening inflationary pressures in Japan keep the door open for a potential BoJ rate hike in January or March, pushing the yield on benchmark 10-year Japanese government bonds to its highest level since July 2011.

- Meanwhile, the 10-year US Treasury yield shot to a multi-month peak in the wake of the Federal Reserve's hawkish shift, projecting only two quarter-point rate cuts in 2025 amid still elevated inflation in the world's largest economy.

- The resultant widening of the US-Japan interest rate differential and the prevalent risk-on mood do little to provide any respite to the safe-haven JPY or hinder the USD/JPY pair's positive move back above the 158.00 round figure.

- Traders now look to Tuesday's US economic docket – featuring the ISM Services PMI and JOLTS Job Openings – for some impetus ahead of the FOMC minutes and the US Nonfarm Payrolls on Wednesday and Friday, respectively.

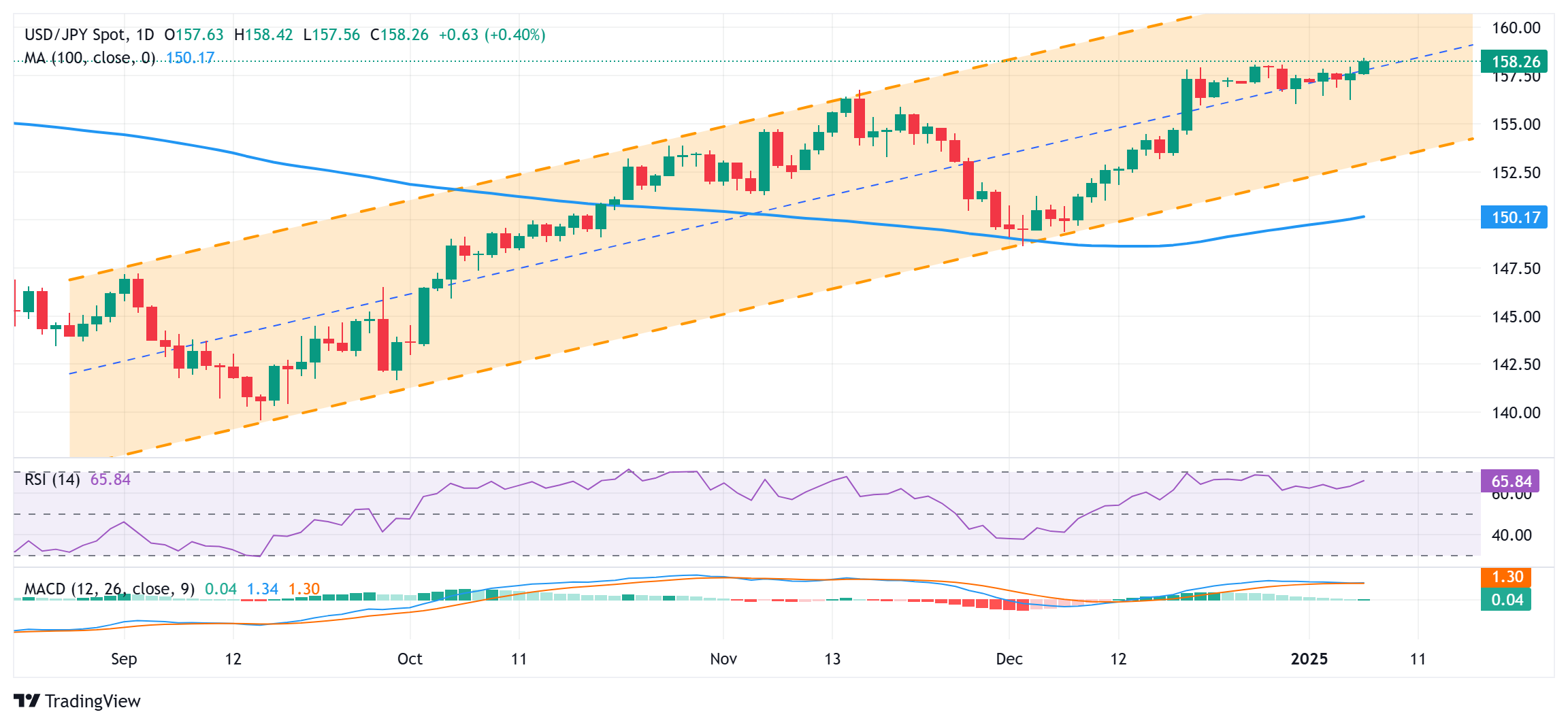

USD/JPY could accelerate intraday corrective pullback below daily swing low, around mid-157.00s

From a technical perspective, a sustained move beyond the 158.00 mark could be seen as a fresh trigger for bullish traders and support prospects for additional gains. The constructive outlook is reinforced by the fact that oscillators on the daily chart are holding comfortably in positive territory and are still away from being in the overbought zone. Hence, a subsequent strength towards the 159.00 round figure, en route to the 159.45 intermediate hurdle and the 160.00 psychological mark, looks like a distinct possibility.

On the flip side, the 158.00 round figure now seems to protect the immediate downside ahead of the 157.55-157.50 region. Any further pullback might now be seen as a buying opportunity and remain limited near the 157.00 mark. Some follow-through selling, however, could drag the USD/JPY pair to the 156.25 intermediate support en route to the 156.00 mark. The latter should act as a pivotal point, which if broken decisively, might negate the positive bias and pave the way for a deeper corrective decline.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.